UAE leaving OPEC is not just a policy shift. It is reshaping oil market dynamics, supply coordination and global energy power balances across the Gulf system.

This move signals a transition from collective production control toward independent national energy strategies, with implications far beyond pricing.

From Coordination to Autonomy — What Just Happened

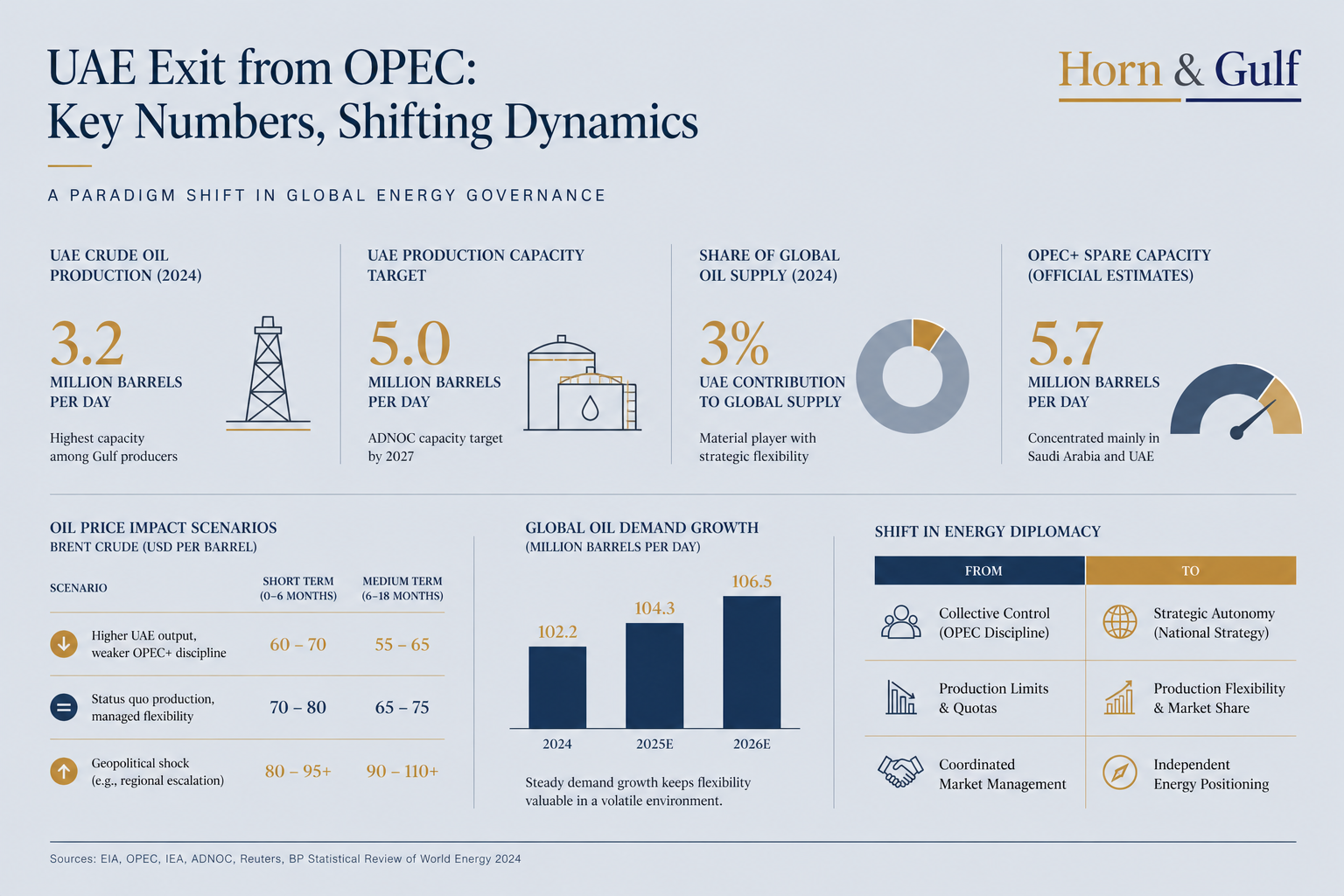

The decision by the Organization of the Petroleum Exporting Countries to lose one of its most strategic Gulf members is not a routine policy adjustment. When the United Arab Emirates announced it would exit OPEC, it effectively signaled the end of a long-standing assumption: that Gulf oil producers would continue to act as a coordinated bloc under Saudi Arabia’s leadership.

For decades, OPEC—and later OPEC+—functioned as both a price stabilization mechanism and a geopolitical alignment tool. The UAE’s departure disrupts both layers. It is not merely about production quotas. It is about who controls supply decisions in a world where energy has once again become strategic.

The Structural Tension — Why This Break Was Inevitable

This rupture has been building quietly for years. Abu Dhabi has invested heavily in expanding production capacity, with ambitions to reach and monetize output levels that OPEC quotas increasingly constrained. At the same time, it has repositioned itself as a broader energy hub—integrating upstream production with refining, storage, and global distribution networks.

That model does not sit comfortably within a cartel designed to restrict supply. What appears today as a political decision is, in reality, the resolution of a structural contradiction: a state pursuing volume, flexibility, and long-term market share cannot indefinitely operate within a system built on restraint.

Short-Term Market Reaction — Discipline vs. Uncertainty

In the immediate term, oil markets will focus on one question: does this weaken collective supply discipline? If the UAE chooses to increase production beyond former quotas, it introduces downward pressure on prices. Even the perception of fragmentation within OPEC+ can trigger volatility, as markets begin to price in a lower level of coordination.

But there is a second layer of uncertainty. In moments of crisis—whether tied to the Strait of Hormuz or broader regional instability—OPEC+ has functioned as a coordination mechanism. A weaker structure raises questions about response speed and cohesion during supply shocks. In short, the market may face a paradox: more potential supply, but less predictable governance.

Regional Balance — A Quiet Shift in Gulf Power Dynamics

The implications within the Gulf are more profound than the immediate market reaction. For Saudi Arabia, the departure is not simply about losing a member. It challenges Riyadh’s role as the central coordinator of oil policy and, by extension, its influence over global energy pricing mechanisms.

For the UAE, the move reinforces a different trajectory—one that has been visible across ports, logistics corridors, finance, and energy infrastructure. Abu Dhabi is positioning itself as an autonomous node in the global system, not merely a participant in a regional bloc.

This does not mean a rupture in UAE–Saudi relations. But it does mark a transition from alignment to managed competition.

Global Implications — A Fragmenting Energy Order

For major external actors, the shift carries mixed consequences. The United States may see an advantage in a less cohesive OPEC, as weaker coordination can ease upward pressure on oil prices and inflation. At the same time, Washington gains from a more direct and flexible energy relationship with Abu Dhabi.

The European Union benefits from diversification. A UAE operating outside strict quotas can provide an additional layer of supply flexibility at a time when energy security remains a priority.

For China, the picture is more complex. Greater supply optionality is positive, but reduced coordination introduces longer-term unpredictability in pricing and supply management—an issue for a system that depends on stable energy flows.

Beyond Oil — The Logic of UAE’s Strategic Exit

To understand the decision, it is necessary to look beyond oil prices. The UAE is not exiting OPEC to produce more oil in the narrow sense. It is exiting to control how oil fits into a broader economic architecture.

Energy, in this model, is integrated with logistics, finance, and geopolitical positioning. Ports, storage hubs, refining capacity, and trade routes form a system in which oil is one component of a larger strategy.

Within such a system, externally imposed production limits become a constraint—not just on revenue, but on strategic flexibility. This is the deeper logic: sovereignty over production is also sovereignty over positioning.

Long-Term Outlook — From Cartels to Competing Systems

The longer-term consequence is unlikely to be an immediate collapse of OPEC. The organization will continue to function, and Saudi Arabia will remain a dominant player. But the nature of the system is changing.

What was once a relatively cohesive producer bloc is gradually evolving into a set of competing national strategies. Coordination will still exist, but it will be more transactional, less structural.

Oil markets, in turn, will be shaped less by collective decisions and more by the interaction of independent actors pursuing their own models.

Conclusion — A System Repricing, Not a System Breakdown

The UAE’s exit does not signal the end of OPEC as much as it signals the end of a certain type of order. The global energy system is not collapsing. It is being repriced.

Power is shifting away from centralized coordination toward distributed control—where states with the capacity to produce, move, and finance energy flows operate with increasing independence. In that sense, this is not just an oil story. It is a story about how the architecture of global systems is quietly being rewritten.