Gulf sovereign capital shift is no longer a cyclical reaction to geopolitical risk. It is actively reshaping how capital flows, ownership structures and private financial channels evolve across global markets.

The War Did Not Freeze Capital — It Changed Its Direction

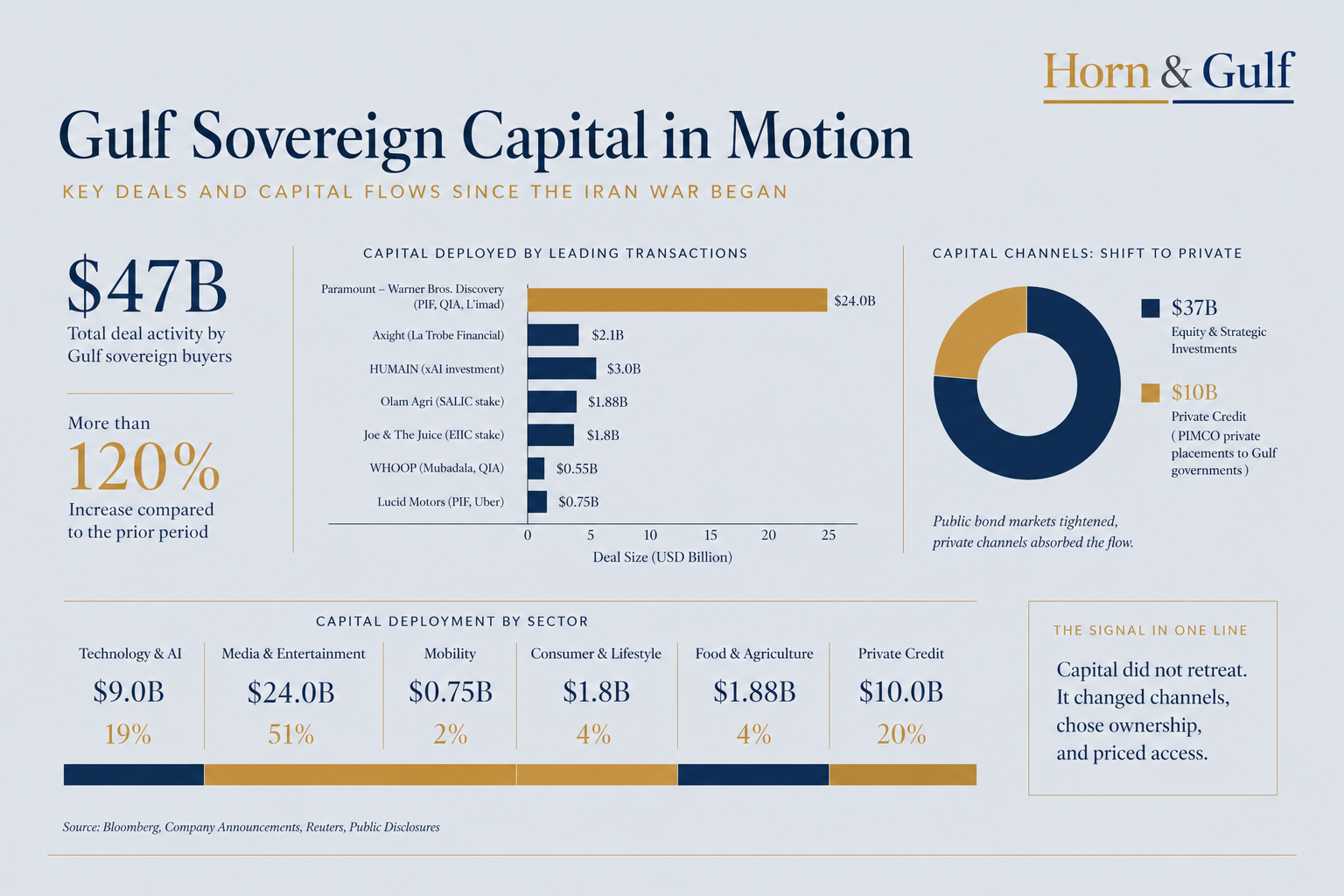

The assumption was simple: conflict would slow the region down. Capital would pause, wait, retreat to safety. That did not happen. Since the escalation tied to the Iran war, Gulf-linked sovereign and strategic investors have been involved in roughly $47 billion worth of global transactions.

The number itself is striking, but it is not the most important part of the story. What matters is how that capital is being deployed — and what it reveals about the structure beneath it. This is not a surge of opportunistic buying. It is a shift in how risk is interpreted, priced, and ultimately owned.

Volume Tells One Story — Composition Tells Another

At first glance, the headline number suggests aggression. But the composition tells something more deliberate.

Some of the transactions sit in traditional sovereign patterns — food security through Olam Agri, or mobility exposure via Lucid Motors backed by Public Investment Fund. Others move into consumer brands and global distribution networks, like Joe & The Juice.

But the deeper signal lies elsewhere. Capital is entering artificial intelligence platforms, private credit structures, and global media ecosystems. Investments tied to SpaceX and xAI, alongside commitments around a potential merger involving Paramount Global and Warner Bros. Discovery, show something beyond diversification.

This is not sector rotation. It is system positioning.

From Oil Surplus to System Ownership

For decades, Gulf capital followed a recognizable pattern: recycle surplus into stable Western assets, prioritize yield, preserve liquidity. That pattern is breaking.

Today’s allocation behavior looks closer to a multi-asset institutional investor than a region under geopolitical pressure. Technology platforms, media infrastructure, food systems, and logistics-linked assets are being accumulated not for short-term returns, but for structural leverage. Even the financing side reflects this shift.

When public bond markets tightened, capital did not disappear. It rerouted. PIMCO extended close to $10 billion in private placements to Gulf governments, effectively replacing public liquidity with private channels. The system did not lose access to capital. It internalized it.

Private Channels Are Replacing Public Signals

This is where the real shift becomes visible. Public markets tend to react quickly — spreads widen, issuance slows, headlines turn cautious. But beneath that surface, a parallel system continues to function.

Private credit, sovereign partnerships, and direct equity placements are taking on a larger role. These are quieter channels, less visible, but far more controlled. They allow capital to move without signaling panic. More importantly, they allow it to move with intent.

In this structure, volatility is not avoided. It is absorbed and redirected.

The Gulf Is Not Pricing Fear — It Is Pricing Access

There is a tendency to read geopolitical tension as a discount factor. Risk rises, valuations fall, capital waits. That logic no longer fully applies. What we are seeing instead is a repricing of access. Access to technology platforms. Access to global consumer networks. Access to distribution, data, and narrative infrastructure.

In that sense, the current wave of transactions is not defensive. It is selective. The region is not asking whether risk exists. It is asking where control can be established within that risk.

Conflict Is Not a Pause — It Is a Filter

The deeper takeaway is simple, but often missed. Conflict does not necessarily reduce activity. It filters it.

Weaker capital structures step back. Public market noise increases. But institutional capital — particularly sovereign-backed — becomes more targeted, more deliberate, and often more strategic. The Gulf is operating within that layer. Not as a reactive player, but as a system participant shaping where capital flows next.

A Region That Does Not Exit Cycles — It Converts Them

Across conversations in financial centers, there is a noticeable shift in perception. Less urgency, more patience. Less fear, more calibration. The region has seen cycles before. What distinguishes this moment is not resilience alone, but adaptation.

Capital is not leaving. It is reorganizing. And in doing so, it is quietly redefining how geopolitical risk translates into ownership.

The Gulf is not stepping back from volatility. It is turning it into position.