Hormuz risk is no longer a temporary disruption. It is reshaping Gulf energy flows, increasing systemic costs and redefining how risk is priced across the region. What is unfolding is not a breakdown of energy movement, but a structural repricing of the Gulf system itself.

The Shock Is Not the War — It Is the System

The Iran war is not simply a security crisis for the Gulf. It is a structural test of how the region functions under pressure. The disruption around the Strait of Hormuz, combined with Houthi attacks on maritime routes and the UAE’s strategic repositioning, is not fragmenting the system — it is forcing it to reveal its underlying mechanics.

What is unfolding is not a breakdown of flows, but their repricing.

For decades, the Gulf operated on a basic assumption: that energy would move, capital would follow, and risk would remain contained. That assumption is no longer holding. The system is still operating, but it is doing so under a different logic — one where cost, access, and control are no longer stable variables.

Hormuz Is No Longer a Chokepoint — It Is a Risk Multiplier

The traditional reading of the Strait of Hormuz treats it as a binary: open or closed. In practice, it has become something far more complex.

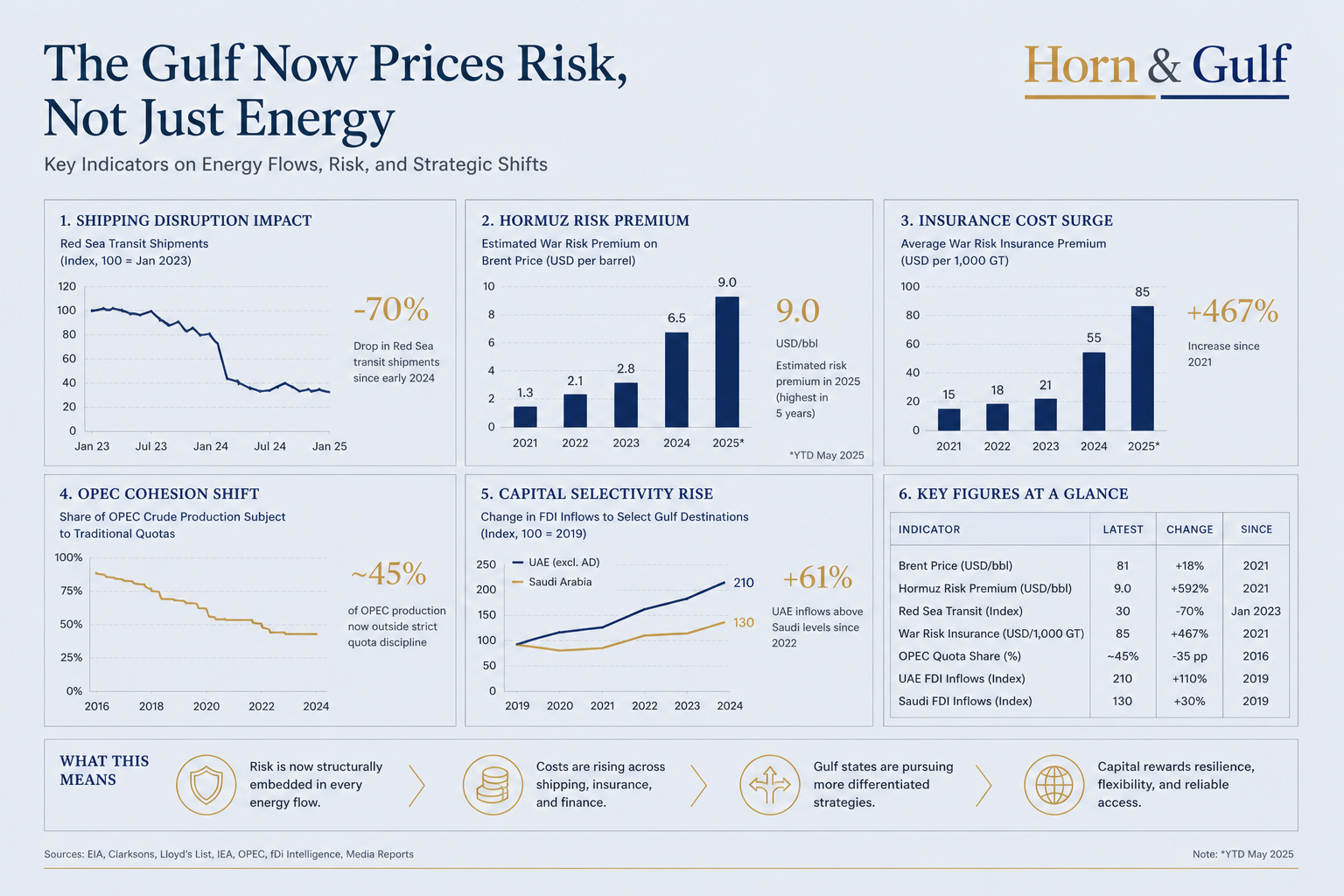

Even without a full closure, the perception of disruption is enough to alter flows. Shipping routes extend, insurance premiums rise, and delivery timelines shift. The result is not halted trade, but more expensive trade.

This is the key shift. The Strait is no longer just a physical bottleneck. It functions as a financial layer — one that injects cost and uncertainty into every barrel that passes through it.

Iran does not need to close Hormuz to exert pressure. It only needs to make it unpredictable.

Saudi Arabia’s Strategy Faces a Flow Dependency Problem

Saudi Arabia’s economic transformation is built on continuity — stable flows of capital, goods, and perception. Vision 2030 is not only an economic plan; it is a bet on reliability.

The current environment challenges that assumption.

Large-scale investments require more than long-term ambition. They require predictable access — to logistics, to markets, and to global confidence. When the main energy corridor becomes volatile, the entire model begins to absorb that volatility.

This is not a collapse of strategy. It is a stress test of its dependencies.

The Kingdom’s position is now defined by a tension it cannot fully control: it is attempting to move beyond oil while still relying on oil’s infrastructure to fund and enable that transition.

Houthis and the Expansion of System-Level Risk

The Red Sea has already demonstrated how limited, targeted disruptions can reshape global trade behavior. The Houthis, operating with relatively modest capabilities, have managed to alter shipping patterns and introduce persistent uncertainty into maritime routes.

This is not about scale. It is about leverage.

A small number of attacks can produce outsized effects when they intersect with critical infrastructure. The result is not continuous disruption, but recurring uncertainty — enough to force recalibration across the system.

Non-state actors are no longer operating at the margins. They are embedded within the system, capable of influencing its cost structure without needing to control it outright.

The UAE’s Exit Reflects a Shift Toward Strategic Flexibility

The UAE’s departure from OPEC appears, at first glance, to be an energy policy decision. In reality, it reflects a broader recalibration.

In a more volatile environment, coordination carries constraints. Collective frameworks limit the ability to respond quickly to changing conditions. What once provided stability now introduces rigidity.

The UAE’s move signals a preference for flexibility over alignment. It suggests a shift from shared control mechanisms toward individualized flow strategies — where each state positions itself according to its own risk tolerance and economic priorities.

This is not fragmentation. It is adaptation.

From Energy Market to Risk Market

The Gulf is no longer priced purely through supply and demand. It is increasingly priced through risk. Oil flows continue, but they carry additional layers: insurance costs, route diversification, timing uncertainty, and political exposure. These factors are no longer secondary — they are embedded in the price itself.

The market is not asking whether energy will move. It is asking under what conditions, and at what cost. This distinction matters. It marks the transition from a volume-driven system to a risk-adjusted one.

Capital Does Not Exit — It Repositions

Under these conditions, capital does not simply withdraw from the region. It becomes more selective.

Investment gravitates toward environments that can absorb shocks — where infrastructure, governance, and financial systems provide a buffer against volatility. This is where the Gulf begins to differentiate internally.

Some parts of the system carry more exposure. Others begin to price resilience. The result is not uniform movement, but redistribution.

A Region Moving From Stability to Managed Instability

The Gulf is not entering a phase of disorder. It is entering a phase of managed instability.

Flows continue. Energy moves. Capital remains engaged. But all of it operates under revised expectations — higher costs, tighter margins, and greater sensitivity to disruption.

This is not a temporary adjustment. It is a structural shift. The region is no longer defined by the absence of risk, but by its ability to operate within it.

Conclusion: The Gulf Now Prices Risk, Not Just Energy

The central question is no longer how the war reshapes individual strategies. It is how the system absorbs and redistributes its effects.

The answer is already visible. The Gulf is not ceasing to function. It is learning to function differently — with risk as a core variable rather than an external threat.

Energy still flows. But what is being traded, increasingly, is not just oil. It is certainty — and its cost.