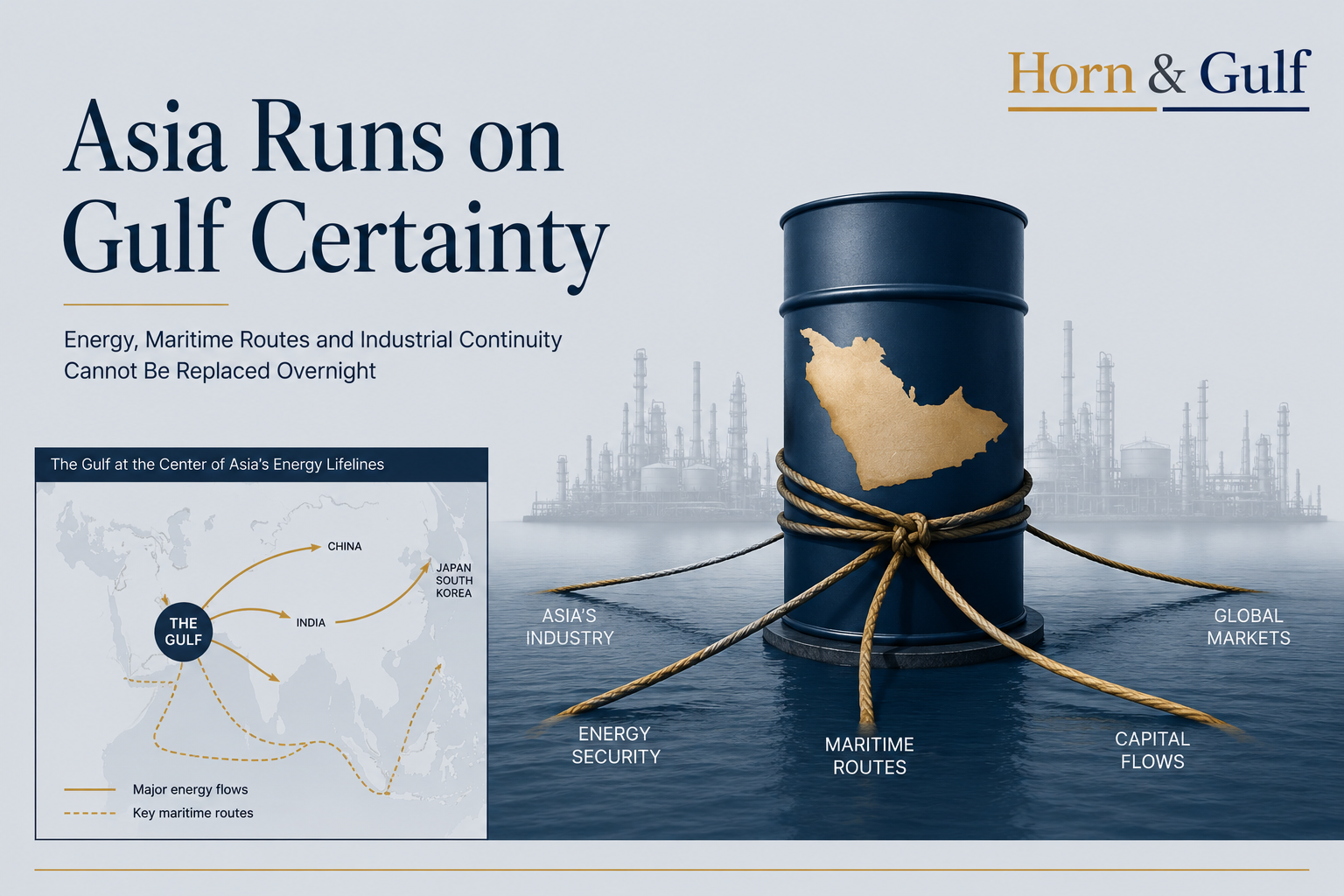

Asia Gulf crude dependency remains one of the defining structural realities of the global energy system. While Asian economies continue seeking supplier diversification, refinery compatibility, maritime logistics and Gulf-linked energy infrastructure make rapid replacement far more difficult than headline narratives often suggest.

The Signal Behind the Signal

The central argument in the recent analysis by Observer Research Foundation (ORF) is fundamentally correct: Asia cannot rapidly replace Gulf crude because large parts of its refining and industrial systems were built around long-term access to Middle Eastern energy flows.

At first glance, this appears to be a conventional energy-security discussion. Gulf producers supply scale, geographical proximity and the crude grades many Asian refineries were specifically designed to process. A major disruption around the Strait of Hormuz would therefore create significant substitution challenges.

But the deeper issue extends beyond oil dependency in the traditional sense.

Over time, the Gulf has evolved from a commodity supplier into an increasingly embedded component of Asia’s industrial and logistical architecture. That distinction matters.

The original article correctly highlights refinery chemistry, infrastructure compatibility and long-term supply relationships. However, the broader significance lies in how Gulf energy flows are now connected to maritime security, logistics resilience, insurance pricing, sovereign capital and industrial continuity across Asia.

The issue is no longer simply about oil volumes. It is increasingly about system stability.

Oil Markets Are More Structurally Rigid Than Headlines Suggest

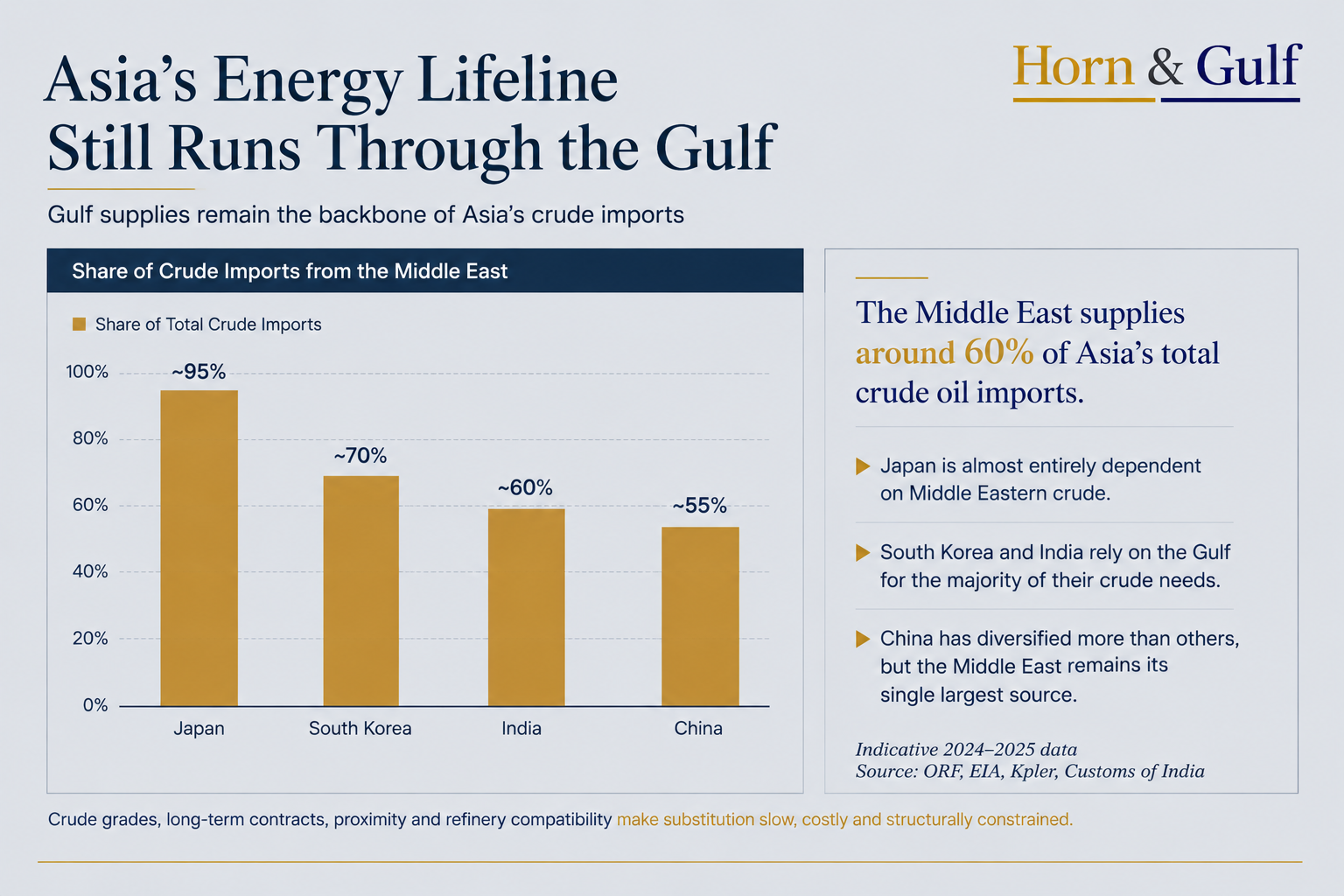

One of the strongest aspects of the ORF analysis is its rejection of a common assumption during geopolitical crises: that oil markets can always find rapid alternative supply.

In reality, crude oil is not universally interchangeable.

Large parts of Asia’s refining infrastructure were optimized over decades for medium and heavy sour crude grades supplied primarily by Saudi Arabia, Iraq, Kuwait and the UAE. Replacing those flows with lighter crude from other regions is not simply a purchasing decision. It can alter refinery efficiency, product yields and operational margins.

This becomes particularly important during periods of elevated geopolitical tension, when shipping times lengthen, inventories tighten and insurance costs rise simultaneously.

In other words, energy substitution is constrained not only by available supply, but also by industrial compatibility and infrastructure design.

That structural layer is often underappreciated in discussions surrounding Hormuz-related risk.

Gulf Energy Influence Extends Beyond Production

Where the original analysis remains incomplete is in its treatment of Gulf states primarily as exporters. The regional energy model has become significantly more integrated over the past two decades.

Saudi Aramco, ADNOC and other Gulf energy institutions are no longer simply shipping crude eastward. They are increasingly connected to Asian downstream systems through refinery partnerships, storage infrastructure, petrochemical integration, long-term supply agreements and strategic investment relationships.

This changes the nature of interdependence. Asia is not simply purchasing oil from the Gulf. Large parts of Asia’s industrial continuity are now connected to Gulf-linked energy infrastructure and maritime reliability. That shift also changes the strategic meaning of Hormuz.

Traditionally, maritime chokepoints were viewed primarily as physical bottlenecks. Increasingly, however, they function as strategic risk layers where security conditions, market expectations and transit confidence influence pricing behavior and industrial predictability even when physical flows continue uninterrupted.

This helps explain why Gulf energy relevance remains structurally important even during periods without major supply disruption.

In modern energy markets, the perceived possibility of disruption alone can affect freight pricing, insurance behavior and inventory decisions.

Hormuz Is Increasingly a Risk-Pricing Environment

Public discussion around Hormuz often remains framed around binary outcomes: open or closed, stable or disrupted. Markets increasingly behave differently.

The more important reality is that Hormuz now functions as a major risk-pricing environment within the global energy system.

Even limited instability — including military signaling, tanker incidents, insurance warnings or navigational disruption — can affect freight costs, hedging behavior and refinery planning long before any large-scale interruption occurs.

The result is a system where geopolitical uncertainty is increasingly reflected in shipping costs, insurance premiums and broader market pricing mechanisms.

This matters especially for Asia because many of its industrial economies remain deeply dependent on uninterrupted maritime energy flows.

China, India, Japan and South Korea may gradually diversify suppliers over time. However, diversification does not fully remove exposure to Gulf-centered maritime risk because the surrounding logistics, insurance and transit architecture remain heavily tied to the region.

This is where the Red Sea becomes increasingly relevant.

The Red Sea and Hormuz Are Now Interconnected Strategic Corridors

One important limitation in the original article is the relatively narrow treatment of Red Sea dynamics. The Gulf and the Red Sea increasingly operate as interconnected maritime systems rather than isolated theaters.

Since the escalation of disruptions in the Red Sea, shipping companies, insurers and energy traders have increasingly assessed maritime risk from the Bab el-Mandeb to Hormuz as part of a connected corridor environment.

That shift carries important implications. When risk levels rise simultaneously across both entry and exit points of Gulf-linked maritime routes, the cost of continuity increases even without a major supply collapse.

Longer shipping routes around Africa, elevated marine insurance premiums, naval protection measures and inventory adjustments gradually feed into industrial pricing systems across Asia.

This should not be viewed merely as a temporary crisis-related distortion. It increasingly reflects a broader structural repricing of maritime reliability and logistical certainty.

Capital Markets Are Also Responding

Another dimension often missing from traditional energy-security analysis is capital behavior. Energy systems are also financial systems.

Periods of sustained maritime uncertainty often strengthen capital concentration in states perceived as institutionally resilient and logistically significant. This helps explain why Gulf financial centers such as Dubai International Financial Centre and Abu Dhabi Global Market continue attracting financial activity despite wider regional volatility.

Markets increasingly distinguish between regional instability and institutional capacity. That distinction is becoming increasingly important.

For many investors, the Gulf is no longer viewed solely as an energy-exporting geography. It is increasingly understood as a combination of ports, logistics infrastructure, financial systems, aviation networks and sovereign investment capacity capable of maintaining continuity under periods of prolonged geopolitical stress.

Under certain conditions, this can increase the strategic value placed on resilient logistics and financial infrastructure.

Diversification Does Not Mean Replacement

Over the medium term, Asian economies will continue pursuing diversification strategies.

China will likely continue expanding strategic reserves and overland connectivity. India will continue seeking broader supplier flexibility. Japan and South Korea are also expected to deepen energy-security coordination with strategic partners. But diversification should not be confused with replacement.

Replacing Gulf crude at scale would require far more than sourcing additional barrels elsewhere. It would involve refinery redesigns, alternative logistics systems, adjusted petrochemical infrastructure and years of capital expenditure.

That transition is technically possible. But it is neither operationally simple nor strategically rapid.

The Gulf Is Becoming Part of Asia’s Industrial Continuity System

The central limitation of the original analysis is that it still frames the Gulf primarily within a traditional producer-consumer relationship.

The emerging reality is more structural. The Gulf is gradually becoming part of the operating architecture supporting Asian industrial continuity.

Its importance increasingly extends across:

- energy supply,

- refining compatibility,

- maritime geography,

- sovereign capital,

- logistics infrastructure,

- insurance pricing,

- and transit resilience.

This is why the question “Can Asia replace Gulf crude?” may ultimately be too narrow. A more important question may be:

How much of Asia’s industrial and logistical system can realistically adjust away from Gulf-linked energy and maritime infrastructure without significant repricing effects?

At present, the adjustment capacity appears limited.

And that is why Hormuz increasingly matters not only as an energy corridor, but as a strategic stabilizing layer within the wider Asian industrial system.