The emerging Hormuz bypass strategy is reshaping how the Gulf approaches maritime resilience and energy continuity. Following the Trump–Xi discussions on regional stability and shipping security, markets increasingly appear to be pricing not only conflict risk, but also infrastructure redundancy, logistics continuity and strategic resilience across the Gulf and Red Sea system.

Trump, Xi and the Repricing of Strategic Passage

The visible signal from the Trump–Xi meeting was diplomatic restraint. Both sides publicly emphasized the importance of stability in the Strait of Hormuz and uninterrupted energy flows. Yet beneath the language of de-escalation, the meeting also highlighted a broader structural reality: the Gulf is increasingly operating through multiple overlapping security and economic frameworks rather than a single strategic logic.

The discussion surrounding Hormuz is gradually evolving from the binary question of whether the strait will remain open into a more complex question of how the risk conditions surrounding passage are managed and perceived.

That distinction matters.

For decades, the strategic logic of the Gulf revolved around clear disruption scenarios — war or stability, closure or continuity, escalation or calm. Markets, insurers and shipping systems were largely structured around that framework. But the recent cycle of tanker rerouting, reported disruptions, insurance repricing and bypass infrastructure investment suggests the region may be entering a different phase.

Hormuz is becoming less a classical maritime chokepoint and more a risk-sensitive corridor operating within a more layered geopolitical environment.

From Maritime Route to Risk-Based Passage

The broader significance of the Trump–Xi dynamic extends beyond conventional US–China competition. It reflects the emergence of overlapping security and economic priorities inside the Gulf itself.

Washington continues to position itself as the principal guarantor of maritime order in the region. The United States remains the dominant naval actor in Gulf waters, and recent strategic signaling continues to reinforce that role. At the same time, recent events have highlighted the growing complexity of maintaining maritime predictability in an increasingly fragmented regional environment.

China, meanwhile, approaches the Gulf primarily through the lens of energy continuity. Beijing’s position appears less ideological than operational. Its core concern is the reliability of maritime and energy corridors that support long-term industrial and economic stability.

Iran remains central to this evolving equation. Recent regional patterns suggest Tehran may see strategic value in calibrated ambiguity and selective pressure rather than outright disruption. From a market-risk perspective, the effect is increased uncertainty surrounding maritime movement and regional escalation dynamics.

That distinction is increasingly shaping market behavior.

Oil traders, insurers and shipping operators are no longer focused solely on catastrophic interruption scenarios. They are also pricing selective friction: delays, rerouting costs, insurance volatility and broader political-risk exposure associated with maritime transit.

The result is a gradual transformation of Hormuz from a traditional transit route into a more permission-sensitive corridor where predictability itself carries growing strategic value.

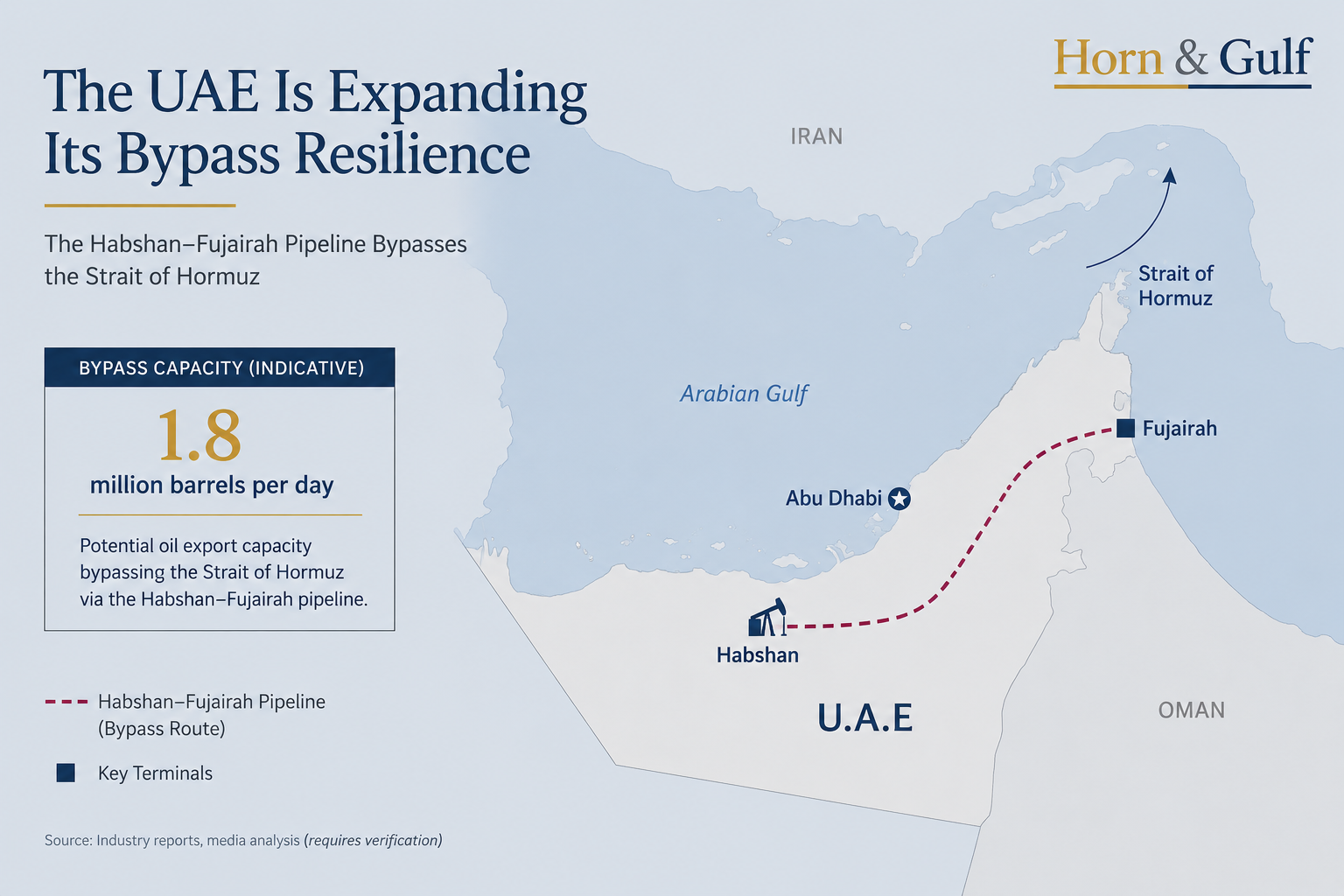

The UAE Is Expanding Its Bypass Resilience

Perhaps the clearest structural response has emerged from the UAE.

While much of the international discussion remains focused on naval security, Abu Dhabi has steadily accelerated a parallel approach centered on strategic bypass capacity. The continued expansion of Fujairah-linked energy and logistics infrastructure reflects a broader Emirati strategic pattern aimed at reducing exposure to chokepoint-related vulnerabilities through diversified transport and export systems.

This extends beyond pipelines alone.

It reflects a wider emphasis on continuity planning and infrastructure resilience under conditions of prolonged regional uncertainty.

Fujairah’s role now extends well beyond storage and export capacity. Increasingly, it functions as a logistics continuity hub designed to preserve trade flows even during periods of elevated geopolitical tension.

In this sense, the UAE is not simply reacting to instability. It is continuing to institutionalize resilience and redundancy as part of its long-term economic and logistical planning.

This also highlights differing strategic emphases inside the Gulf itself.

Saudi Arabia appears more focused on diplomatic stabilization and broader regional security understandings, including efforts aimed at reducing escalation risks with neighboring powers such as Iran. The Emirati approach, by contrast, places greater emphasis on infrastructure autonomy, logistical redundancy and economic continuity under prolonged uncertainty.

These approaches are not contradictory. Rather, they reflect different strategic priorities regarding how the Gulf may adapt to a more complex regional environment.

One places greater emphasis on political stabilization. The other prioritizes infrastructure continuity and operational resilience.

The Red Sea and Horn of Africa Are Becoming More Central

One of the more underappreciated dimensions of the current Gulf transition is the extent to which it is reshaping the strategic importance of the Red Sea and the Horn of Africa.

As Hormuz becomes more sensitive to geopolitical risk, alternative maritime and logistics corridors naturally gain additional value. This increases the strategic relevance of ports, coastal infrastructure and regional alignments stretching from Fujairah to Berbera, Djibouti and the wider western Indian Ocean system.

What once appeared to be isolated infrastructure investments increasingly resembles a more interconnected regional logistics map.

Berbera’s growing importance, Gulf-backed port investments, Sudan’s instability, Ethiopia’s maritime ambitions and Red Sea militarization are no longer entirely separate developments. Together, they increasingly form part of a broader geopolitical repricing process centered on corridor security, logistics continuity and trade resilience.

In that sense, the Gulf’s competitive geography is gradually expanding outward.

This is one reason why the Horn of Africa is likely to attract greater strategic attention in the coming decade — not only because of regional politics, but because logistics resilience itself is becoming an increasingly important dimension of geopolitical influence.

Markets Are Beginning to Price Persistent Friction

Financial markets often respond to structural shifts earlier than political narratives do.

Recent movements in oil prices, shipping premiums and insurance behavior suggest that investors are no longer evaluating the Gulf purely through the lens of imminent large-scale conflict. Increasingly, markets appear to be pricing prolonged geopolitical friction without assuming systemic regional collapse.

That distinction is important.

The older assumption was that the Gulf either functioned normally or entered outright crisis. The emerging reality appears more nuanced: a region capable of remaining operational even under sustained geopolitical pressure.

This creates a different type of market behavior.

Capital does not necessarily exit immediately. Instead, it becomes more selective. Infrastructure with redundancy gains strategic value. Secure logistics nodes attract additional interest. Financial centers positioned around governance, continuity and resilience strengthen their relative importance.

This helps explain why major Gulf financial and logistics hubs continue to expand even during periods of regional volatility. The system is not collapsing. It is being repriced.

A More Layered Gulf System

The Trump–Xi meeting may ultimately matter less for immediate diplomatic outcomes than for what it revealed about the evolving structure of the Gulf itself.

The region today appears less defined by a single external security framework than it once was. At the same time, it is not moving toward outright fragmentation or systemic breakdown.

Instead, the Gulf is evolving into a more layered strategic environment in which maritime continuity, logistics resilience, energy security and infrastructure autonomy increasingly matter alongside traditional military power.

The Gulf is no longer pricing war alone. It is increasingly pricing predictability, bypass capacity and strategic resilience.