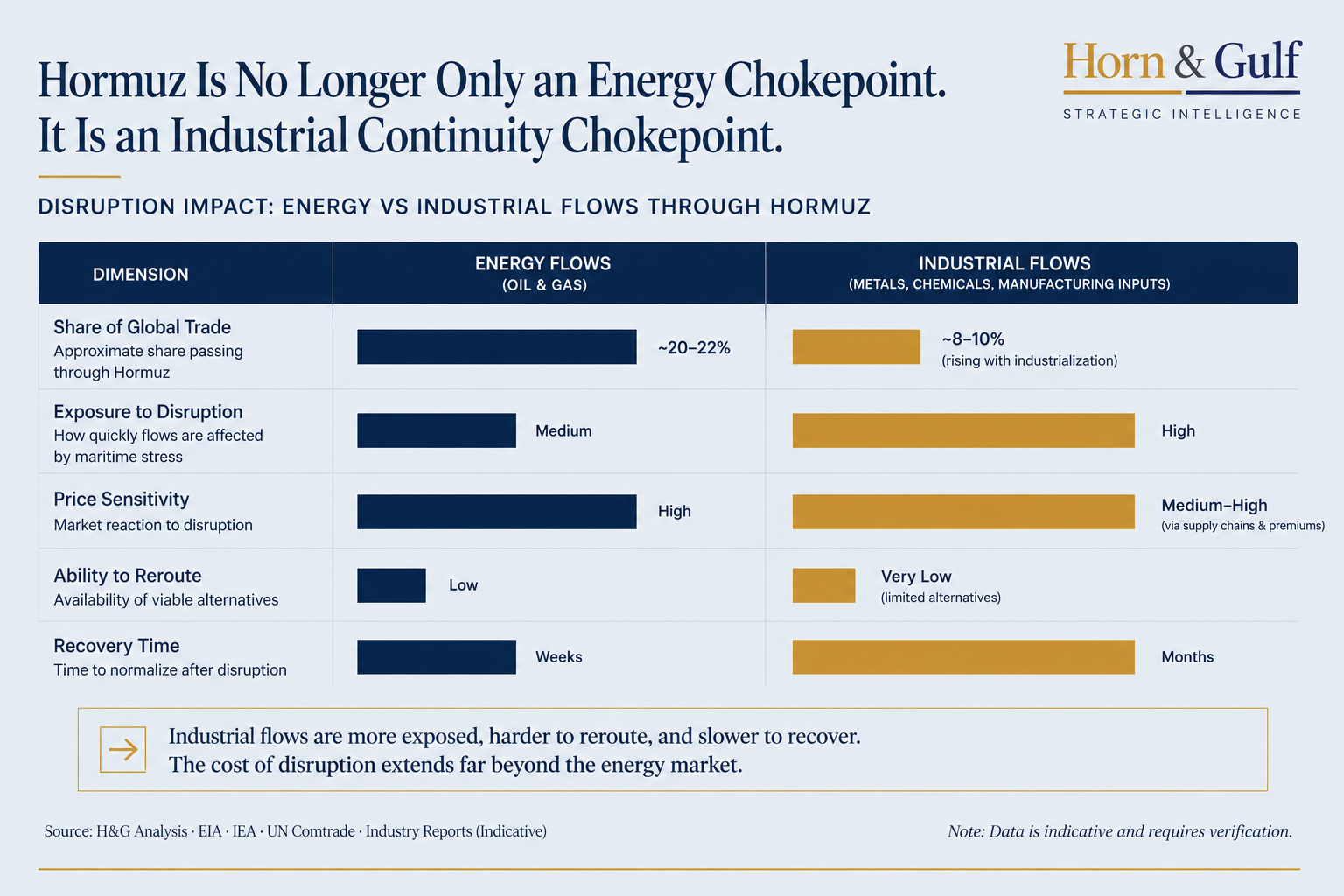

The Hormuz industrial chokepoint is no longer only an energy story. Gulf manufacturing systems now depend heavily on logistics continuity, shipping reliability and insurable maritime access during periods of geopolitical stress.

The latest disruption around Hormuz highlights how industrial economies react differently from energy-export systems. Production capacity alone is no longer enough to guarantee continuity.

Energy Built the Gulf’s Industrial Rise

For years, the Gulf’s industrial rise depended on one core advantage: energy.

Cheap gas, integrated ports and large-scale infrastructure allowed Gulf economies to expand beyond crude exports. The region invested heavily in metals, petrochemicals, logistics and manufacturing.

Aluminium became one of the clearest examples of that transformation.

Smelters across the Gulf helped position the region as an important supplier for construction, aviation, automotive and packaging industries.

But the latest disruption around Hormuz suggests the Gulf’s industrial story is entering a more logistics-sensitive phase. The pressure no longer comes mainly from energy availability. It increasingly comes from continuity.

Industrial Systems Depend on Timing

For years, analysts interpreted Gulf industrialization mainly through production capacity. The logic seemed straightforward. If the region could secure low-cost energy and build industrial infrastructure, industrial expansion would follow.

To a large extent, that strategy succeeded.

The Gulf developed advanced industrial corridors, integrated ports and large re-export systems. Aluminium stood near the centre of that evolution because it connected energy abundance with industrial scale.

Yet industrial systems behave differently from energy-export systems.

Oil markets can absorb disruption through price spikes. Industrial economies depend more heavily on timing, continuity and predictability.

A factory may continue operating while the surrounding logistics environment comes under pressure. That is the deeper signal emerging from Hormuz.

Continuity Matters as Much as Capacity

A smelter may retain stable power supply. Yet production economics can still weaken if shipping routes become less reliable, insurance costs rise or delivery schedules shift. Industrial continuity depends on more than electricity.

It depends on:

- inbound raw materials,

- freight reliability,

- shipping insurance,

- export scheduling,

- spare-parts access,

- customer delivery confidence,

- stable pricing mechanisms,

- predictable transit times.

Once those conditions weaken, the effects spread beyond production volumes. Contracts become harder to manage. Delivery timelines become less predictable. Inventory strategies change. Buyers diversify sourcing exposure. Freight behaviour adjusts. Insurance markets reassess risk conditions.

This is where the Gulf’s aluminium story becomes more than a commodities issue. It becomes a maritime systems issue.

Hormuz Is Becoming an Industrial Chokepoint

The Gulf’s industrial platform increasingly depends on what could be described as insurable continuity.

Industrial strength no longer depends only on energy access and factory scale. It also depends on whether maritime corridors remain commercially credible during periods of geopolitical stress.

That reality connects Hormuz directly to the wider Horn & Gulf framework.

The Gulf, the Red Sea and the Horn of Africa are often discussed as separate geopolitical theatres. In practice, they increasingly function as parts of one integrated logistics and risk architecture.

Recent Red Sea disruptions already demonstrated how rerouting decisions can reshape freight economics, delivery schedules and insurance exposure.

Hormuz introduces another layer. Industrial supply chains themselves can come under pressure even when energy exports continue moving. This creates a deeper strategic question for Gulf states.

Can the region evolve from an energy-export platform into a resilient industrial platform under conditions of sustained geopolitical pressure? That question now carries greater long-term significance than headline oil prices alone.

Industrial Economies React Differently

The Gulf’s industrial strategy assumed that infrastructure, capital and energy could gradually transform the region into a long-term manufacturing and processing hub.

In many ways, that transformation has already occurred. Metals, petrochemicals, refining, logistics and re-export systems now form part of the Gulf’s broader economic identity.

But industrial economies require continuity as much as capacity.

Delayed shipments, insurance restrictions and maritime uncertainty can affect manufacturing economics long before production facilities stop operating.

That is why the current aluminium disruption deserves closer attention. The issue is not simply whether Hormuz remains open.

The issue is whether industrial flows through Hormuz remain commercially dependable enough to support large-scale manufacturing ecosystems.

Historically, Hormuz was viewed mainly as an energy chokepoint. Today it increasingly functions as an industrial continuity chokepoint. The implications no longer stop at crude exports.

They now extend into:

- metals,

- manufacturing inputs,

- supply-chain timing,

- financing structures,

- insurance conditions,

- industrial confidence.

Capital and Insurance May Reprice Risk

The second-order effects may become more visible over time.

Global manufacturers may diversify sourcing exposure. Commodity traders may widen logistical risk assumptions. Insurers and reinsurers may reassess regional exposure models.

Industrial buyers may place greater emphasis on supply redundancy alongside cost efficiency. Capital behaviour could gradually shift as well.

Industrial investment does not flow only toward low-cost energy. It also flows toward environments where logistics, insurance and contractual continuity remain reliable during periods of stress.

If repeated disruptions reduce confidence in maritime continuity, some assumptions surrounding Gulf industrial logistics may gradually be reassessed despite the region’s strong infrastructure base.

That does not mean the Gulf’s industrialization model is weakening structurally. The region continues to possess major advantages:

- low-cost energy,

- sovereign capital,

- integrated ports,

- industrial scale,

- advanced logistics infrastructure,

- strategic geography.

But the aluminium disruption suggests that the next phase of Gulf industrialization may depend less on expanding capacity and more on preserving continuity under geopolitical pressure.

The Gulf Is Becoming Part of the World’s Industrial Architecture

That is the larger strategic signal emerging from Hormuz.

The Gulf no longer simply exports energy to the global economy. It increasingly operates as part of the world’s industrial supply architecture.

Industrial systems are judged not only by what they produce. They are also judged by whether they can continue delivering during periods of disruption.