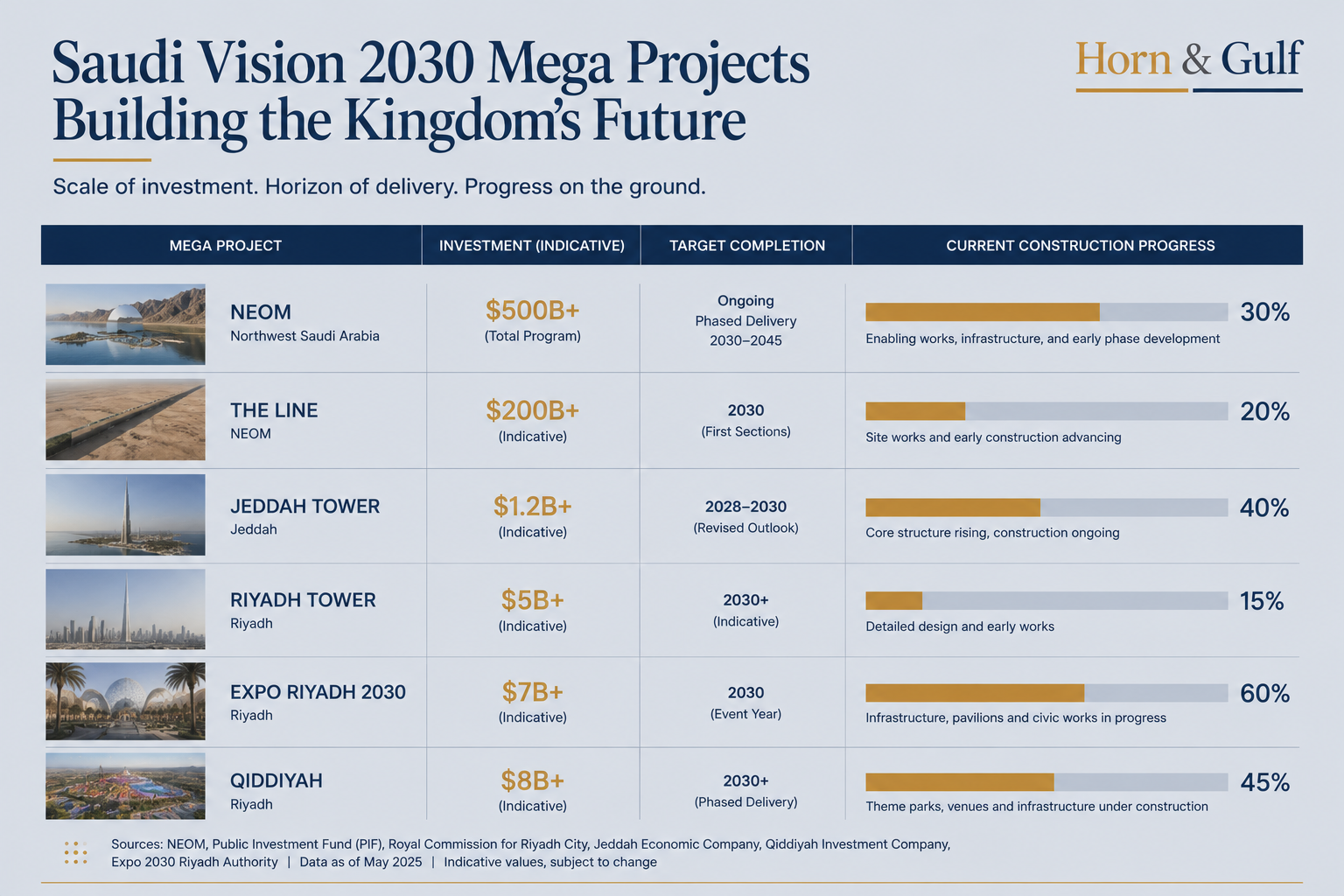

Saudi Vision 2030 is increasingly tied to maritime continuity rather than oil prices alone. As tensions around Hormuz intensify, Saudi Arabia is facing a broader strategic challenge involving logistics resilience, insurance confidence and investor perceptions of Gulf stability.

Hormuz Is Testing the Economic Logic Behind Vision 2030

Saudi Arabia’s challenge in the Iran war is not fundamentally about battlefield exposure. It is about continuity.

The immediate signal is visible across multiple layers at once: maritime risk, insurance pricing, investor psychology, logistics redundancy and the long-term operating assumptions behind Vision 2030. Riyadh is not simply managing regional instability. It is trying to preserve the economic logic that made large-scale transformation possible in the first place.

For years, Saudi Arabia’s regional de-escalation strategy was interpreted primarily through the language of diplomacy. But the deeper function was economic. The Yemen pause, the Iran détente, regional normalization efforts and the broader emphasis on stability all helped construct a more predictable operating environment for capital, tourism, infrastructure investment and strategic partnerships.

In this sense, Saudi de-escalation was never only diplomacy. It functioned as economic infrastructure.

That infrastructure has not broken down. But it is now operating under significantly greater pressure.

The central issue is not whether Saudi Arabia can withstand a temporary regional shock. The Kingdom retains substantial fiscal capacity, sovereign assets, institutional control and long-term strategic depth. The more important question is whether the regional environment can continue supporting the assumptions that underpin Gulf transformation models: stable maritime passage, manageable insurance costs, predictable logistics and sustained investor confidence.

This is where Hormuz becomes more than a military chokepoint.

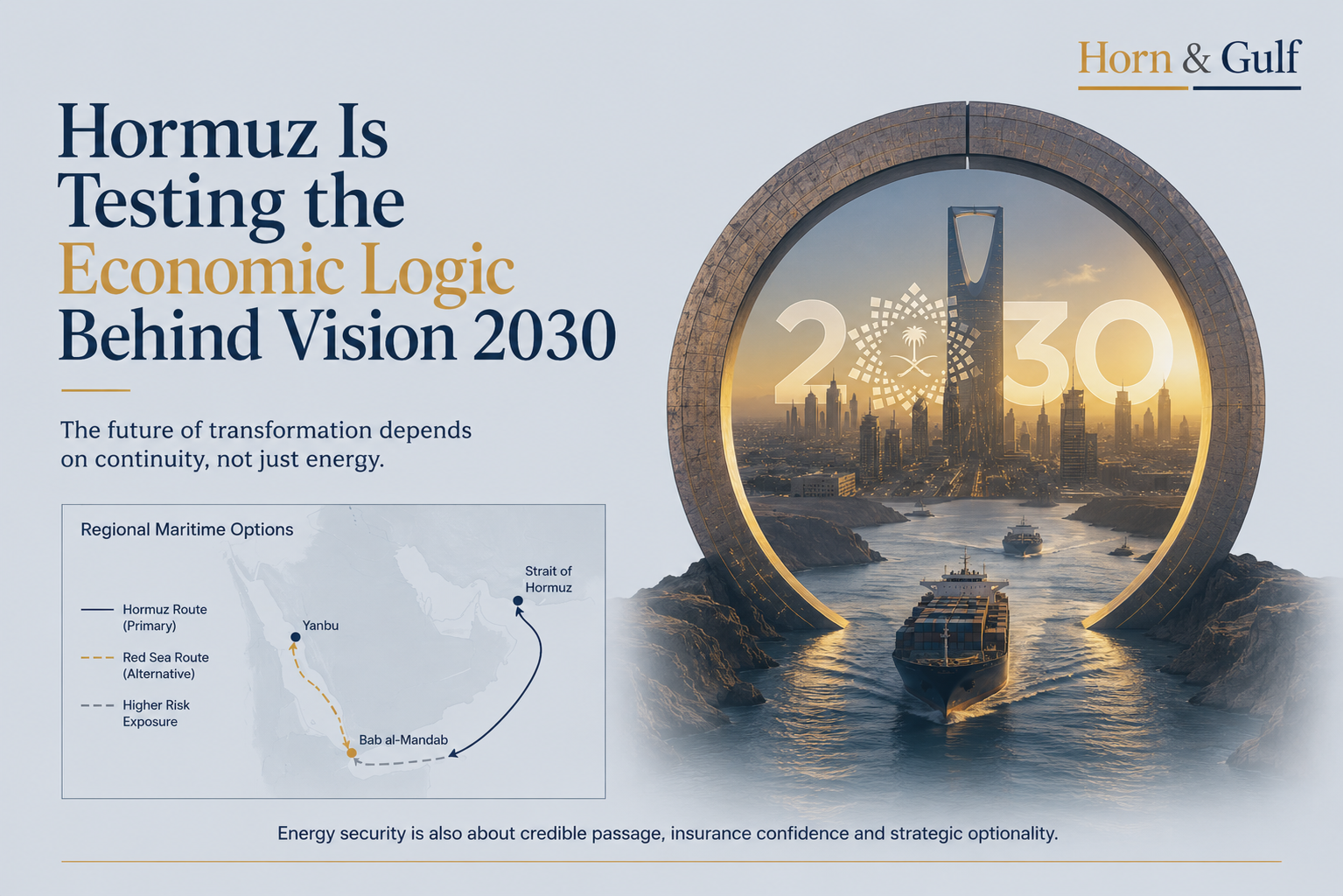

Disruption around the Strait does not only affect oil exports. It also affects the credibility of passage itself. Insurance calculations change. Shipping confidence changes. Contingency planning changes. Even when alternative export routes remain operational, the perception of friction inside the system can gradually alter capital behavior.

That is why Red Sea alternatives matter — but also why they remain incomplete substitutes. Saudi export routes toward Yanbu provide strategic flexibility, yet they introduce their own operational exposure through Bab al-Mandab, longer routing patterns, maritime-security uncertainty and additional logistical costs.

In H&G terms, Saudi Arabia is not only managing an oil-export challenge; it is testing the practical limits of regional route redundancy.

A second structural layer concerns Gulf coordination. Any visible divergence in Saudi–UAE energy positioning should not automatically be interpreted as strategic fragmentation. Gulf states continue to share deep security, economic and financial interdependence. However, the current environment may be encouraging a more interest-specific and policy-driven form of coordination rather than the highly synchronized signaling that previously characterized parts of Gulf energy strategy.

That distinction matters because the Gulf’s long-term attractiveness has depended not only on capital accumulation, but also on continuity, predictability and the perception of strategic coherence.

At the same time, there are strong reasons to avoid exaggerating the current moment. Markets often absorb geopolitical volatility more effectively than early narratives suggest. Insurance pricing can normalize. Shipping patterns can adapt. Hormuz stability may partially return. Saudi project execution may continue with manageable delays rather than systemic disruption.

In that scenario, the Iran war would represent a serious but temporary regional stress event rather than a structural turning point.

This is why the more disciplined conclusion is not collapse, but recalibration.

The Iran war has not undermined the foundations of Saudi transformation. But it has exposed how dependent modern Gulf economic strategy remains on controlled escalation, credible maritime continuity and sustained confidence in regional stability.

If the disruption proves temporary, the broader system may absorb the shock with limited long-term consequences. If instability persists, however, Gulf states may need to invest more actively — financially, diplomatically and logistically — in reinforcing the region’s continuity premium within global capital and supply-chain systems.

What remains uncertain is the duration of the conflict, the resilience of maritime insurance markets, the adaptability of regional logistics networks and the degree to which investors ultimately distinguish between temporary geopolitical turbulence and lasting structural risk.

For now, the signal is visible. But the long-term structure is still forming.