Dubai’s real estate conversation is drifting toward the wrong battlefield. Scroll any property portal and the narrative feels obvious: prices are falling, listings are being cut, sentiment is turning. The conclusion seems intuitive — the market is weakening.

But this is not where the real story is. Listing prices are noise. Transaction prices are lagging confirmation. The signal sits elsewhere — in capital access.

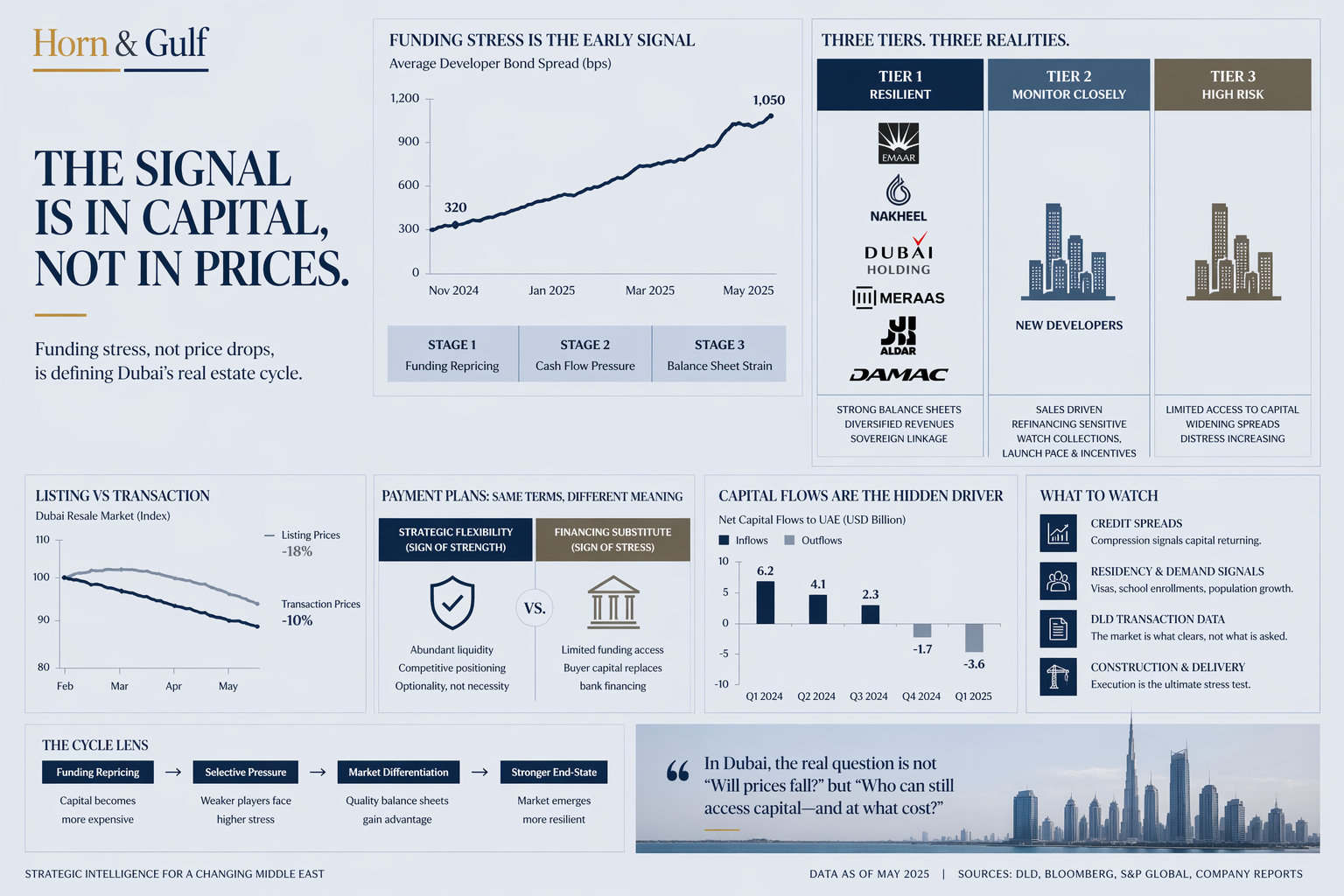

The First Misread: Asking Prices Are Not the Market

A seller dropping a unit from 8M to 5M does not define market value. It defines urgency. What clears — what actually transacts — is the only reliable datapoint. And even that is backward-looking. By the time a transaction prints, the decision that created it was made weeks or months earlier.

This is the first analytical mistake: confusing visible price movement with underlying system stress. The market is not repricing because sellers are emotional. It reprices when capital conditions change.

Where the System Is Actually Tightening

The pressure point is not on the surface. It is in the funding layer. Developer credit spreads have widened sharply. Refinancing costs have reset upward. Access to cheap capital — the invisible engine behind off-plan velocity — is no longer guaranteed.

This is not a collapse signal. It is something more precise: Stage One: funding repricing. In any real estate cycle, this is where stress begins — not with defaults, not with halted construction, but with the cost of money itself. When capital becomes selective, the market stops being uniform.

It starts differentiating.

One Market, Three Realities

Dubai is often discussed as a single market. It is not. It is a stack of balance sheets operating under different constraints.

Tier One — Balance Sheet Driven

Developers with sovereign linkage, diversified income, and large cash buffers.

Their behavior changes first — but not because they are under pressure. Because they have optionality. They can delay launches. They can preserve pricing. They can wait for capital conditions to normalize.

This is not weakness. It is control.

Tier Two — Flow Dependent

Developers with real sales momentum but reliant on continuous off-plan cycles. Their exposure is not immediate — it is conditional. If funding remains tight for an extended period, pressure migrates from pricing to collections, from collections to launch cadence. Nothing breaks instantly.

But the system becomes more sensitive.

Tier Three — Capital Constrained

Smaller developers already being repriced by the market. Here, the signal is explicit:

- widening spreads

- reduced lending access

- increasing reliance on buyer-funded payment structures

At this layer, the distinction between opportunity and risk becomes extremely thin.

The Most Misunderstood Signal: Payment Plans

Flexible payment structures are being read as incentives. In reality, they are information. A long post-handover plan can mean two opposite things:

- A well-capitalized developer choosing to compete aggressively

- A constrained developer replacing bank financing with buyer cash

The structure looks identical. The balance sheet behind it is not. This is where most investors misprice risk — by reading terms, not funding conditions.

What Is Missing From the Conversation

Three critical layers remain largely absent from public discussion.

1. Capital Does Not Stay Still

Dubai is not a closed system. It is an execution hub within global capital flows. Liquidity moving through the Gulf, Asia, Europe — it reallocates continuously based on risk, yield, and stability. When funding costs rise locally, the question is not only “who can borrow?”

It is: Where else can capital go — and at what return? Without this layer, any market analysis remains incomplete.

2. Corridors Matter More Than Prices

The next phase of real estate cycles is not defined by local supply-demand alone. It is defined by capital corridors:

- which jurisdictions are attracting inflows

- which channels remain frictionless

- which structures preserve liquidity movement

As global systems shift from chokepoints to corridors, real estate becomes a downstream expression of those flows. Price adjustments are the surface. Corridor control is the structure.

3. Crisis Is a Filter, Not an Event

What is unfolding is not a singular “market correction.” It is a filtering process. Funding repricing forces selection:

- which developers retain access

- which projects continue without disruption

- which balance sheets absorb stress

This is how markets mature — not through collapse, but through differentiation.

What to Actually Watch

Not listings. Not sentiment. The real indicators are structural:

- Credit spreads: are they compressing or widening further?

- Capital access: who can still refinance, and at what cost?

- Delivery continuity: are projects progressing without delay?

- Residency signals: are people staying, relocating, or pausing decisions?

And most importantly: Is capital returning — or repositioning elsewhere?

Conclusion: The Market Is Not Falling. It Is Sorting.

The mistake is to frame this moment as bullish or bearish. It is neither. It is selective. Dubai is not experiencing a demand collapse. It is undergoing a capital recalibration.

And in that process, the market is doing what it has done in every previous cycle: Not breaking. Not freezing. Refining itself through pressure. The investors who will read this phase correctly are not the ones watching price charts.

They are the ones asking a different question: Who still has access to capital — and who no longer does? Because right now, that distinction is the market.