DIFC Q1 2026 growth is not just a performance story. It reflects how global capital is relocating to Dubai, reshaping financial flows, regulatory structures and regional influence across the Gulf system.

The first quarter of 2026 did not simply mark another period of growth for Dubai International Financial Centre (DIFC). It revealed something deeper: a structural shift in how global capital is repositioning itself under pressure.

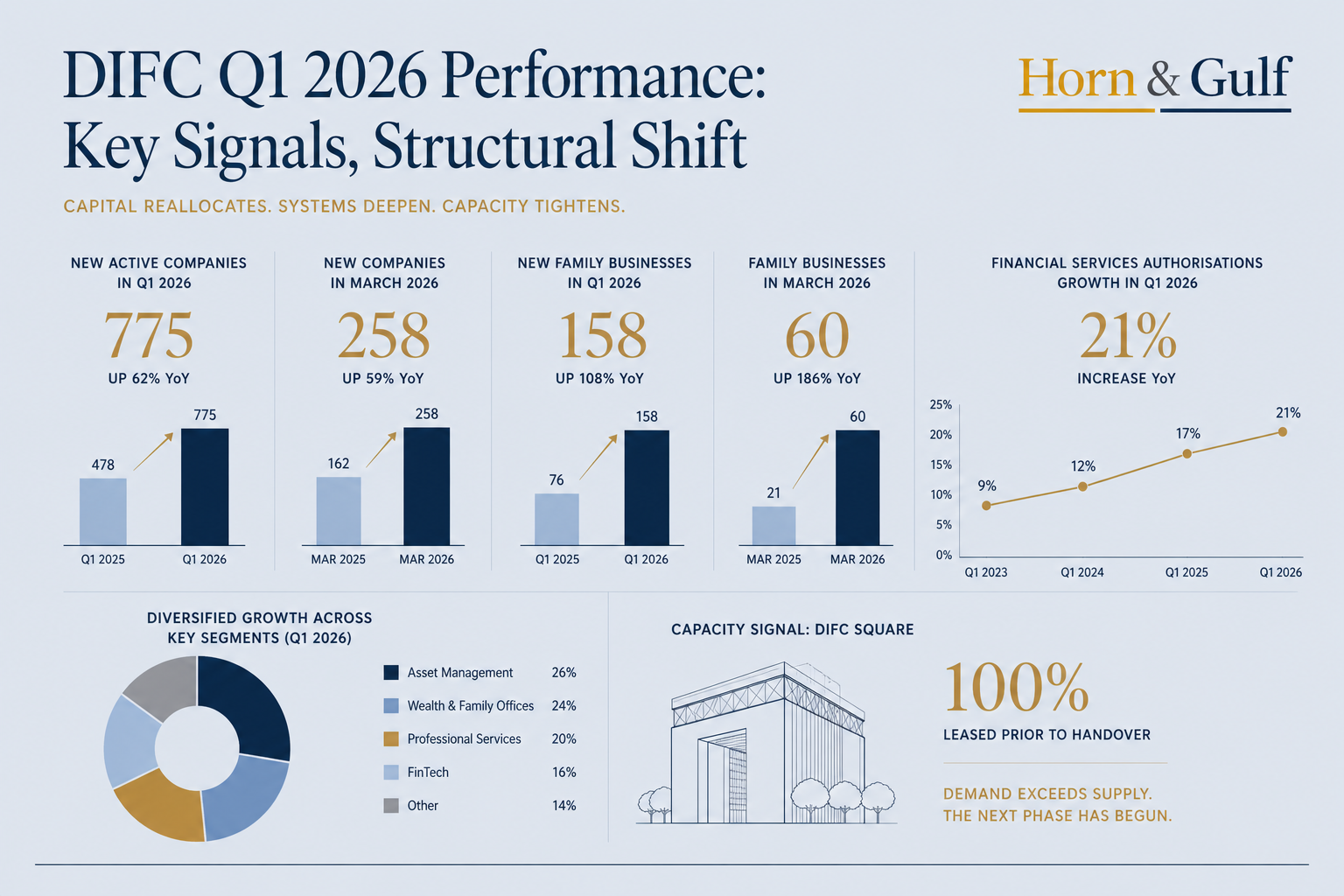

At face value, the numbers are strong. Around 775 new companies established presence in the Centre during Q1, a sharp year-on-year increase. Family business registrations more than doubled, while financial services authorisations rose by over 20 percent. Physical capacity tightened as DIFC Square reached full occupancy even before handover.

Taken in isolation, these figures describe expansion. Taken together, they point to something else entirely.

Company Growth Is Not Expansion — It Is Capital Repositioning

The rise in new company registrations is often read as a signal of economic dynamism. But the composition of that growth matters more than the headline figure.

A significant share of new entrants into DIFC are not large operating firms building industrial capacity. They are advisory entities, holding structures, family offices, and special purpose vehicles. These are not instruments of production. They are instruments of positioning.

This distinction changes the reading of the data. What appears as corporate growth is, in reality, capital reorganising itself—seeking jurisdictional clarity, legal protection, and operational flexibility.

DIFC is not absorbing companies. It is absorbing balance sheets.

Family Offices Are Not Expanding — They Are Relocating Risk

The sharp increase in family business registrations is one of the most telling signals in the dataset. On paper, it suggests entrepreneurial growth. In practice, it reflects wealth migration.

Family offices move for three reasons: protection, efficiency, and access. The surge in registrations indicates that private capital is not simply chasing returns—it is seeking stability in an increasingly fragmented global environment.

This is not about new wealth creation. It is about existing wealth reassigning its geographic and legal anchor. Dubai is becoming that anchor.

Licensing Growth Signals Depth — Not Just Volume

Among all the metrics, the increase in financial services authorisations carries the most structural weight.

Unlike general company registrations, financial licences require regulatory approval, operational substance, and compliance infrastructure. Growth in this segment suggests not just more entities, but deeper financial activity.

It indicates that DIFC is not only attracting capital—it is building the mechanisms to intermediate, deploy, and manage it. This is the difference between a financial hub and a financial system.

Full Occupancy Signals Constraint — Not Completion

The early full leasing of DIFC Square is presented as a milestone. It is, but not in the way it is often framed. Full occupancy before completion does not signal equilibrium. It signals pressure.

Demand for space within DIFC now exceeds available supply. This is not a marketing success—it is a capacity signal. It implies that growth is beginning to push against physical limits, forcing the next phase of expansion outward into surrounding districts. In practical terms, the financial centre is no longer contained within its original geography. It is spilling into the city.

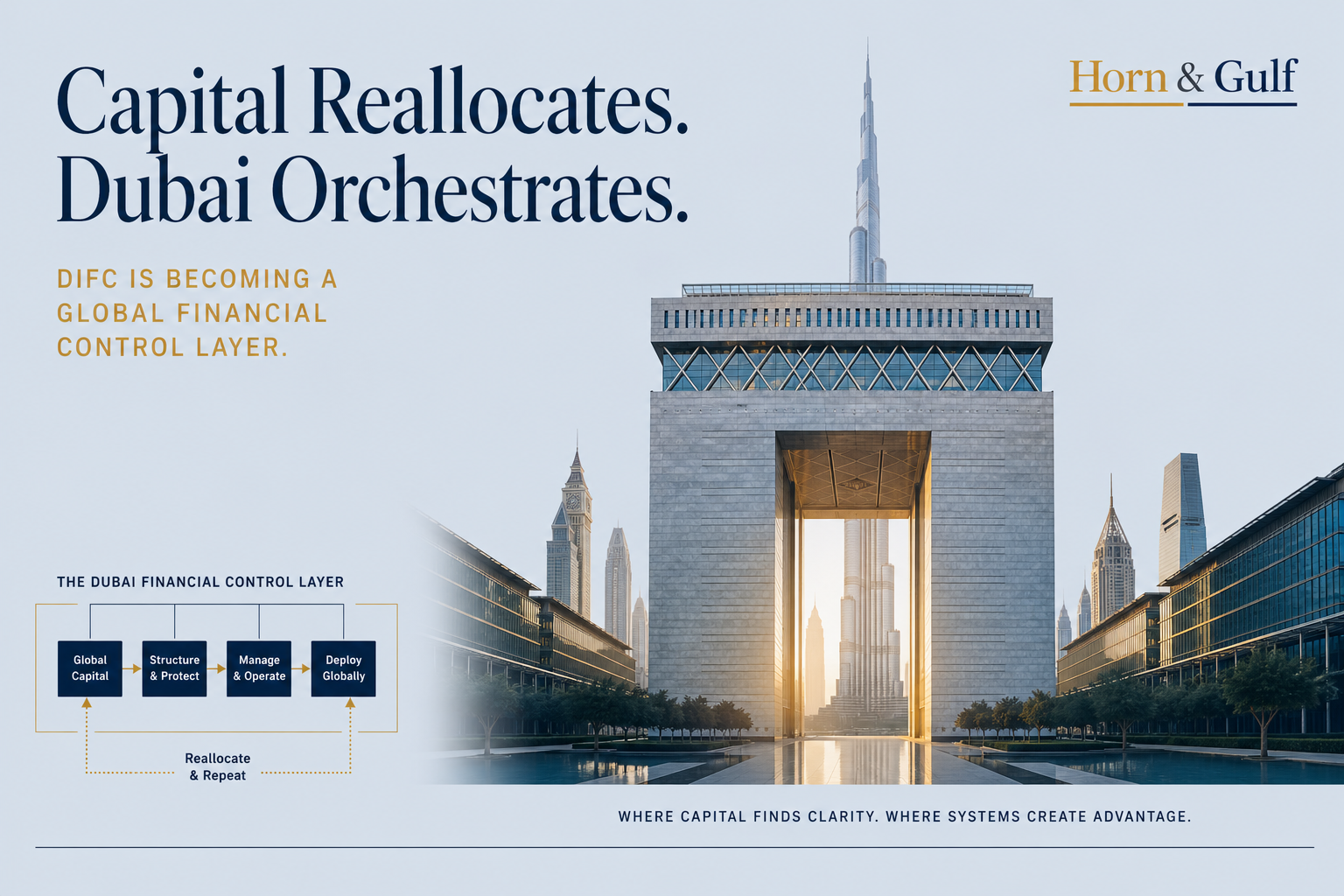

DIFC Is No Longer a Location — It Is a Financial Control Layer

When these signals are placed together, a clearer structure emerges. DIFC is evolving beyond the role of a free zone or business district. It is becoming a control layer within the global financial system—a place where capital is routed, structured, and stabilised before being deployed elsewhere.

This transformation is being driven by three overlapping pressures: Global fragmentation, as major economies diverge in policy and regulation.

Regional instability, particularly across the Red Sea and Gulf corridors.

Capital mobility, as wealth becomes more agile and less tied to origin markets.

In this environment, location matters less than system design. DIFC offers a predictable legal framework, regulatory clarity, and operational connectivity. These are not features of a city. They are features of infrastructure.

Capital Is Not Fleeing Instability — It Is Repricing Through Dubai

The underlying logic of this shift is often misunderstood. Capital does not simply exit regions under stress. It recalibrates. It seeks environments where risk can be priced, managed, and, where possible, neutralised.

Dubai is increasingly that environment. The inflow into DIFC is not driven by optimism alone. It is driven by the need to reorganise exposure—to hold assets in one jurisdiction, operate in another, and deploy in a third.

In this sense, DIFC functions less as a destination and more as an interface between systems.

The Real Impact Extends Beyond Finance — Into the City Itself

Financial flows do not remain confined to financial districts. They translate into physical demand. As firms establish presence, they bring teams, services, and support structures. This expands demand for office space, housing, and urban infrastructure—particularly in adjacent areas such as Downtown Dubai and Business Bay.

This is where financial architecture meets real estate reality. The pressure seen in DIFC Square is already being absorbed by the surrounding city. Over time, this diffusion will reshape how central Dubai functions—not as a collection of districts, but as an integrated financial ecosystem.

Growth Is Not the Story — System Reconfiguration Is

It is tempting to read DIFC’s Q1 performance as another success story in Dubai’s growth narrative. That reading is incomplete.

What the data shows is not simple expansion. It is system reconfiguration.

Global capital is not just arriving. It is reorganising itself within a new framework—one designed for a world of fragmented markets, shifting risks, and mobile wealth. DIFC sits at the centre of that framework.

And if the current trajectory holds, its role will not be defined by how many companies it hosts, but by how much of the world’s capital chooses to pass through it.