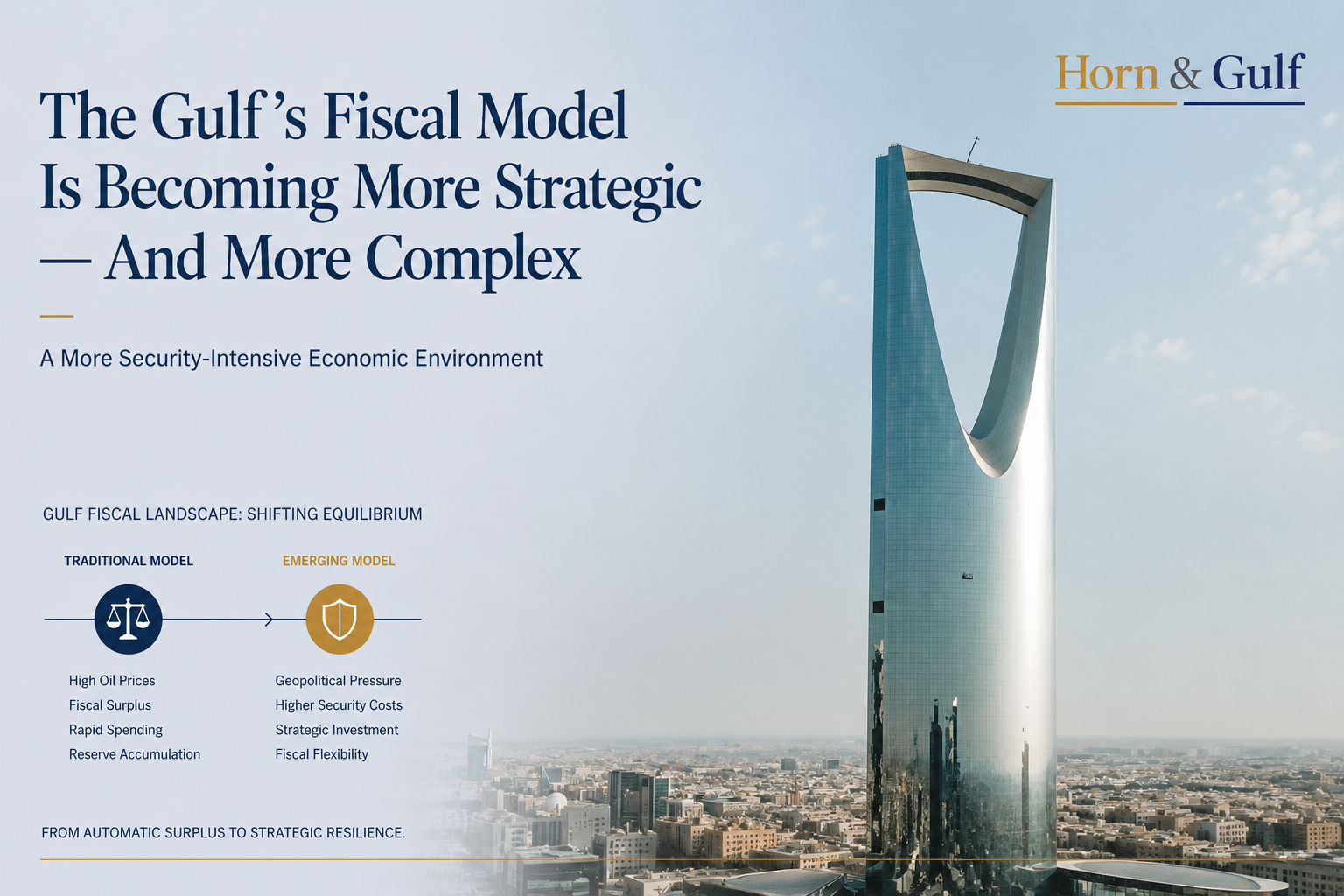

Saudi Arabia’s budget deficit is becoming more than a fiscal story. The widening deficit reflects a broader Gulf transition toward strategic capital deployment, infrastructure resilience and security-intensive economic planning. As regional maritime and geopolitical risks evolve, Gulf states are increasingly prioritising continuity and long-term capacity over purely surplus-driven fiscal management.

For decades, Gulf fiscal logic followed a relatively familiar pattern.

When oil prices strengthened, fiscal surpluses expanded, reserves accumulated and governments accelerated development spending. When oil prices weakened, states adjusted expenditure, recalibrated investment priorities and moved toward tighter fiscal management.

That framework is becoming less sufficient to explain the Gulf’s evolving economic direction.

Saudi Arabia’s widening 2026 budget deficit is not simply a short-term imbalance between expenditure and revenue. It is also a signal that the Gulf region is entering a more security-intensive, capital-intensive and infrastructure-focused strategic phase.

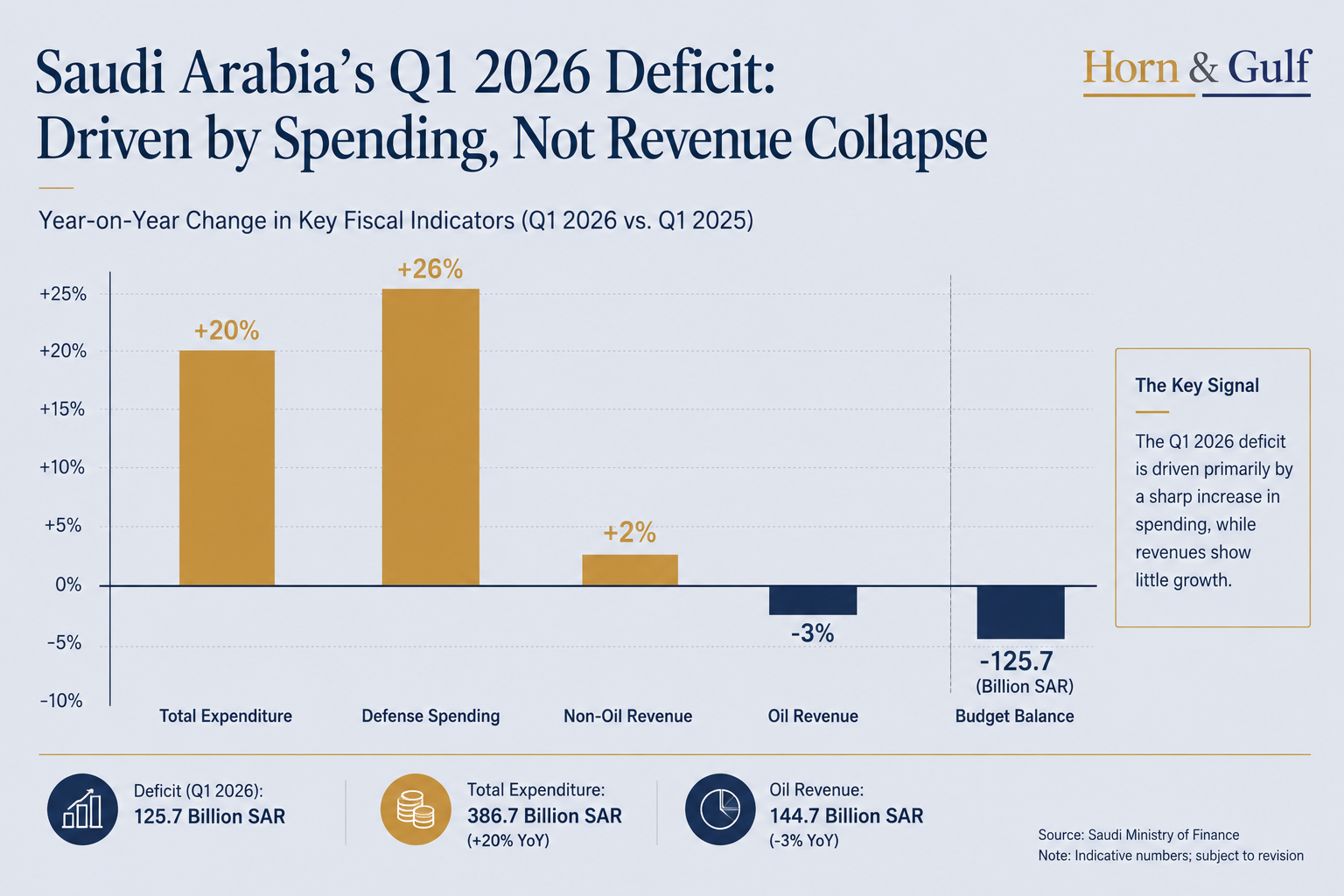

According to official figures reported by Reuters, Saudi Arabia recorded a first-quarter deficit of more than SR125 billion while expenditure rose sharply year-on-year. The more important signal, however, is not only the size of the deficit itself. It is that Riyadh chose to maintain strategic spending momentum despite a more complex external environment.

That distinction matters.

The Gulf Is Operating in a More Security-Intensive Economic Environment

The traditional Gulf economic model developed during a period of relatively stable maritime assumptions.

Energy exports moved through Hormuz with limited disruption risk. Shipping routes were widely viewed as commercially reliable. Insurance markets operated under comparatively predictable conditions, while fiscal surpluses supported large-scale development strategies across the region.

Today, the operating environment is becoming more complex.

The Gulf now faces:

- higher maritime risk sensitivity,

- periodic disruption concerns in the Red Sea,

- evolving drone and missile warfare environments,

- logistics fragmentation pressures,

- rising insurance costs,

- and increasing strategic competition across regional corridors.

This does not imply instability or systemic breakdown.

Rather, it suggests that maintaining continuity across trade, logistics, infrastructure and energy systems is becoming more expensive and strategically important.

Saudi fiscal policy increasingly reflects this broader regional reality.

Vision 2030 Is Expanding Beyond Economic Diversification

Many external analyses still frame Vision 2030 primarily as an economic diversification programme. That interpretation captures part of the picture, but not all of it.

Vision 2030 is also increasingly functioning as a broader state-capacity and economic resilience framework. Its objectives include:

- sustaining long-term economic momentum,

- supporting labour-market expansion,

- attracting international capital,

- strengthening industrial capacity,

- improving logistics redundancy,

- and reinforcing institutional resilience during periods of geopolitical volatility.

In this context, Saudi Arabia’s continued investment strategy reflects a longer-term view of transformation rather than a short-term fiscal calculation alone.

Saudi policymakers appear to view the continuation of strategic investment momentum as essential to maintaining long-term economic competitiveness and regional positioning.

That helps explain why Riyadh continues large-scale expenditure despite softer oil revenue conditions and wider deficits.

The Red Sea Is Becoming More Central to Gulf Strategic Planning

One of the most underappreciated dimensions of the Saudi fiscal story is maritime strategy.

Hormuz-related risk does not need to result in full disruption to influence regional planning assumptions. Even limited uncertainty can affect:

- shipping behaviour,

- insurance pricing,

- storage strategies,

- pipeline utilisation,

- port investment,

- and export diversification planning.

This is where the Red Sea becomes increasingly important.

Saudi Arabia’s western energy and logistics infrastructure is no longer viewed solely through a developmental lens. It is also becoming part of a broader continuity and resilience architecture.

Yanbu, Red Sea ports, inland logistics corridors and western industrial infrastructure provide additional flexibility should Gulf maritime pressure intensify during periods of regional tension.

The earlier Gulf development model prioritised efficiency and speed. The emerging model places greater emphasis on redundancy, continuity and strategic flexibility.

That shift is gradual, but significant.

Gulf Fiscal Strategy May Become More Capital-Intensive

Another important implication is financial.

Historically, Gulf economic stability was strongly associated with large hydrocarbon surpluses and relatively conservative debt exposure.

Today, several regional economies appear to be moving toward a more investment-driven model characterised by:

- higher strategic borrowing,

- larger sovereign balance sheets,

- long-term infrastructure financing,

- and more active state-led capital deployment.

This does not necessarily imply structural weakness.

The Gulf continues to retain major advantages:

- sovereign wealth capacity,

- energy leverage,

- relatively strong balance sheets,

- currency stability,

- and deepening access to global capital markets.

However, it does suggest that the region’s economic philosophy is evolving.

The central question for investors is increasingly not whether deficits exist, but whether those deficits contribute to productive long-term capacity:

- industrial depth,

- logistics resilience,

- technological capability,

- and stronger economic diversification.

That distinction will become increasingly important in how Gulf sovereign risk and regional growth are evaluated over the coming decade.

The Gulf Is Increasingly Being Viewed as a Strategic Economic System

Perhaps the most important shift is conceptual.

The Gulf is no longer viewed only as an energy-export region. It is increasingly being evaluated as:

- a strategic logistics corridor,

- a sovereign capital platform,

- a maritime continuity system,

- and a geopolitical infrastructure network.

That changes how infrastructure is valued.

It changes how ports are assessed.

It changes how defence spending is interpreted.

And it changes how investors evaluate long-term regional resilience.

This is why Saudi Arabia’s fiscal trajectory matters beyond economics alone.

The broader signal is that the Gulf region is adapting to a more complex strategic environment where resilience, continuity and long-term infrastructure capacity are becoming increasingly central to economic planning.

The Gulf’s era of automatic surplus is becoming more conditional.

A more strategic — and more operationally demanding — regional framework is gradually taking shape.