Dubai real estate coordination is becoming increasingly important as the Gulf adapts to geopolitical fragmentation and shifting capital flows. The recent Emaar shareholder restructuring reflects a broader trend in which flagship assets, infrastructure and institutional capital are being aligned within a more integrated regional economic framework.

The Signal Beneath the Transaction

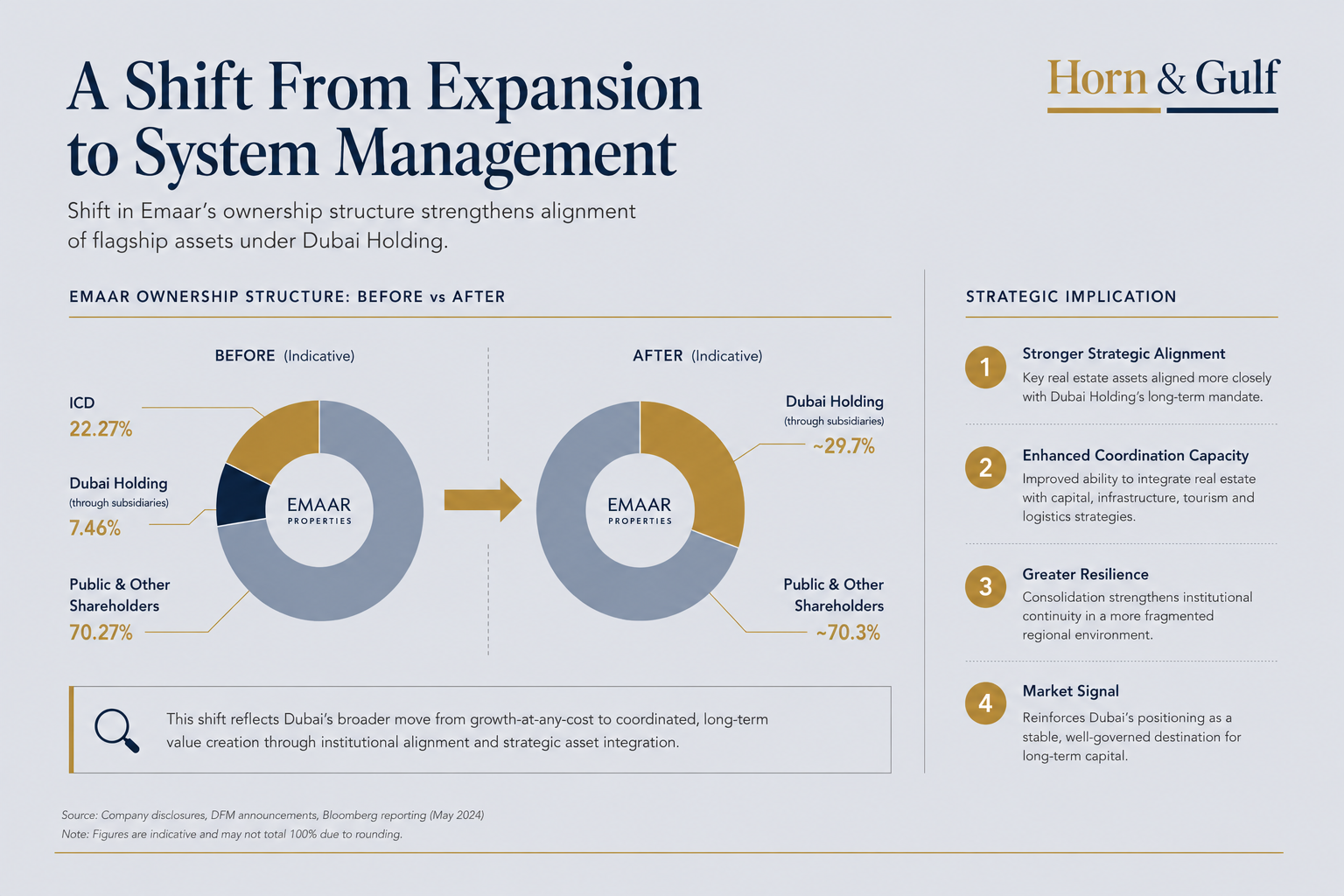

The visible headline is straightforward enough: a Dubai government-linked firm has become the largest shareholder in Emaar after acquiring a major stake from the emirate’s sovereign investment vehicle.

On paper, this appears to be an internal restructuring within Dubai’s state-linked corporate ecosystem. In practice, however, the move also reflects how Gulf cities are adapting to a more fragmented geopolitical and economic environment.

The transaction matters because Emaar is not simply another real estate developer. It is one of the institutional pillars of Dubai’s global city model. Downtown Dubai, Dubai Mall, hospitality assets, recurring retail income, waterfront expansion, tourism branding and international investor psychology all intersect through Emaar’s balance sheet.

This is not only about property. It is also about strategic coordination.

Bloomberg’s reporting on the stake transfer has been broadly supported by regional financial reporting and Dubai Financial Market disclosures, although the precise valuation attached to the transaction still appears partially estimate-based rather than fully detailed in public filings. What is clearly visible, however, is the broader structural shift itself: Dubai Holding has emerged as the dominant shareholder in Emaar, while ICD’s direct position has receded.

That distinction matters. Because the story is less about ownership change than about governance architecture.

From Growth Story to Strategic Coordination

For much of the past two decades, Dubai’s real estate model was externally interpreted through the language of growth cycles: boom, correction, recovery and expansion. That framework is becoming increasingly incomplete.

The emirate’s major state-linked developers — including Emaar, Nakheel, Meraas and Dubai Properties — increasingly resemble components of a coordinated urban-capital ecosystem rather than entirely separate commercial entities operating independently from one another.

Under normal conditions, this type of restructuring could be interpreted primarily as administrative simplification or portfolio optimization.

But the regional environment is no longer defined by conventional market conditions alone. The Gulf now operates inside an environment shaped by persistent geopolitical repricing:

- Red Sea disruption,

- maritime insurance volatility,

- Hormuz uncertainty,

- supply-chain fragmentation,

- sanctions adaptation,

- logistics securitization,

- and intensifying competition between financial hubs.

Against this backdrop, Dubai’s real estate ecosystem now carries significance beyond domestic property demand alone. It increasingly forms part of the emirate’s broader economic resilience architecture.

Real Estate as a Capital Preservation Layer

One of the most underappreciated dynamics in Gulf economics is that premium real estate increasingly appears to function as one channel for regional capital preservation and allocation.

Periods of regional uncertainty no longer automatically trigger capital flight away from the Gulf. In some cases, they contribute to capital redistribution within the region toward jurisdictions perceived as institutionally stable, globally connected and operationally predictable.

Dubai appears to have benefited from this broader repricing cycle.

The city’s aviation connectivity, arbitration environment, financial services ecosystem, luxury residential market, residency flexibility and dollar-linked monetary stability together form an integrated continuity proposition for global investors and businesses.

In this environment, flagship developers are no longer viewed solely as construction companies.

They also operate as strategic components within a larger urban-economic platform linked to tourism, logistics, financial services and long-term capital positioning.

That helps explain why governance alignment around these platforms may carry greater importance today than during previous real estate cycles.

The restructuring of Emaar’s shareholder framework therefore appears less like a speculative market move and more like a long-term institutional alignment designed to support strategic urban coordination.

The Red Sea Effect That Does Not Appear in Property Headlines

Most real estate reporting still treats Dubai property demand as a local supply-and-demand story. That increasingly misses the wider regional system.

The disruption of Red Sea shipping lanes over the past two years accelerated a broader repricing of logistical reliability across the Gulf. Maritime uncertainty raised the strategic value of jurisdictions capable of combining:

- physical infrastructure,

- financial flexibility,

- legal continuity,

- and political predictability.

Dubai sits near the center of that adaptation layer.

Jebel Ali, DIFC, Emirates airline connectivity, free zones, logistics corridors and premium urban districts increasingly reinforce one another within a single economic ecosystem. Real estate appreciation cannot be entirely isolated from these wider systems.

A waterfront apartment in Dubai is no longer priced solely against local housing fundamentals. It is increasingly influenced by the continuity premium investors assign during periods of regional uncertainty.

That helps explain why Gulf real estate — particularly in globally connected hubs — has shown resilience even during periods of broader geopolitical tension. The market is not only trading yield.

It is also trading continuity, connectivity and institutional predictability.

A Shift From Expansion to System Management

The deeper signal inside the Emaar transaction may therefore be institutional rather than purely financial.

Dubai appears to be entering a phase where managing the coherence of the broader economic ecosystem matters more than maximizing the autonomy of individual components.

That does not imply centralization in a traditional statist sense. Rather, it suggests the emergence of a more coordinated strategic-capital model where:

- urban planning,

- sovereign capital,

- logistics,

- tourism,

- infrastructure,

- and financial governance

increasingly operate through an integrated long-term framework.

This distinction is important. For years, international commentary often interpreted Gulf megaprojects primarily through the lens of branding or speculative expansion.

What is becoming increasingly visible instead is a stronger emphasis on institutional capacity, coordination and long-term economic positioning.

The Gulf’s leading systems increasingly appear focused on resilience and operational continuity rather than expansion alone.

The Underpriced Risk

At the same time, risks remain embedded within this model.

As strategic coordination deepens, the distinction between institutional alignment and market concentration can become thinner. Greater alignment between flagship developers and state-linked holding structures may strengthen execution capacity, but over time it may also reduce competitive diversity within parts of the market.

Another underpriced variable is external dependency.

Dubai’s real estate ecosystem remains closely connected to global liquidity conditions, high-net-worth mobility, tourism flows and international investor confidence. If global financial conditions tighten sharply or regional escalation materially disrupts Gulf aviation or maritime systems, property valuations could face pressure despite strong local coordination mechanisms.

For now, however, markets appear to be pricing continuity rather than disruption. And that may be the most important signal of all.

Dubai’s Next Phase Is About Strategic Operating Architecture

The old Dubai story was primarily about growth. The emerging Dubai story is increasingly about strategic operating architecture.

Not architecture in a coercive sense — but in the systemic sense:

- organizing capital flows,

- strengthening logistics reliability,

- reinforcing investor confidence,

- supporting urban continuity,

- and aligning strategic assets during an age of geopolitical fragmentation.

That is what makes the Emaar transaction significant beyond finance pages.

Dubai is not only expanding its skyline.

It is strengthening the institutional architecture beneath it.