The Iran war Gulf risk environment is no longer limited to oil markets or military escalation alone. As tensions surrounding Hormuz intensify, the Gulf is increasingly functioning as a systemic control layer connecting maritime security, insurance pricing, logistics resilience and global capital flows.

Rather than operating as isolated crises, disruptions across the Gulf and Red Sea are increasingly influencing one another through interconnected trade and risk networks.

The immediate signal is military escalation surrounding Iran and renewed pressure on the Gulf security environment. The deeper structural reality, however, may prove more consequential: the Gulf is no longer functioning merely as a producer of energy or a passive absorber of geopolitical shocks. It is increasingly operating as a global pricing center for risk itself.

That distinction matters.

Much of the conventional analysis surrounding a potential Iran conflict still approaches the region through the vocabulary of the early 2000s — oil supply disruption, naval escalation, missile exchanges and temporary volatility in energy markets. But the architecture of the global system has evolved. Energy flows are now increasingly interconnected with maritime insurance, logistics reliability, digital infrastructure, capital mobility, sovereign governance and supply-chain continuity.

The emerging order is not simply multipolar. It is infrastructural.

A confrontation involving Iran could accelerate the gradual erosion of the post-Cold War framework and deepen the transition toward a more fragmented geopolitical environment. Yet the more important shift may lie elsewhere: influence is increasingly being shaped not only by ownership of resources, but by the ability to manage the corridors, permissions, financial protections and logistical systems through which those resources move.

That is where the Gulf is being repriced.

The Gulf Is No Longer Only an Energy Buffer

For decades, the region’s global role was largely framed through hydrocarbon supply, while external powers played a central role in the wider security framework.

That framework is evolving.

Today, the Gulf increasingly functions as a center where global crises are interpreted, priced, hedged and operationally managed. The region is no longer simply downstream from geopolitical shocks. It increasingly sits at the intersection of energy security, maritime connectivity, sovereign capital and logistical resilience.

This shift is visible through the concentration of logistics infrastructure, sovereign capital, maritime insurance exposure, aviation connectivity and financial governance systems emerging across the UAE and Saudi Arabia.

The implications are significant.

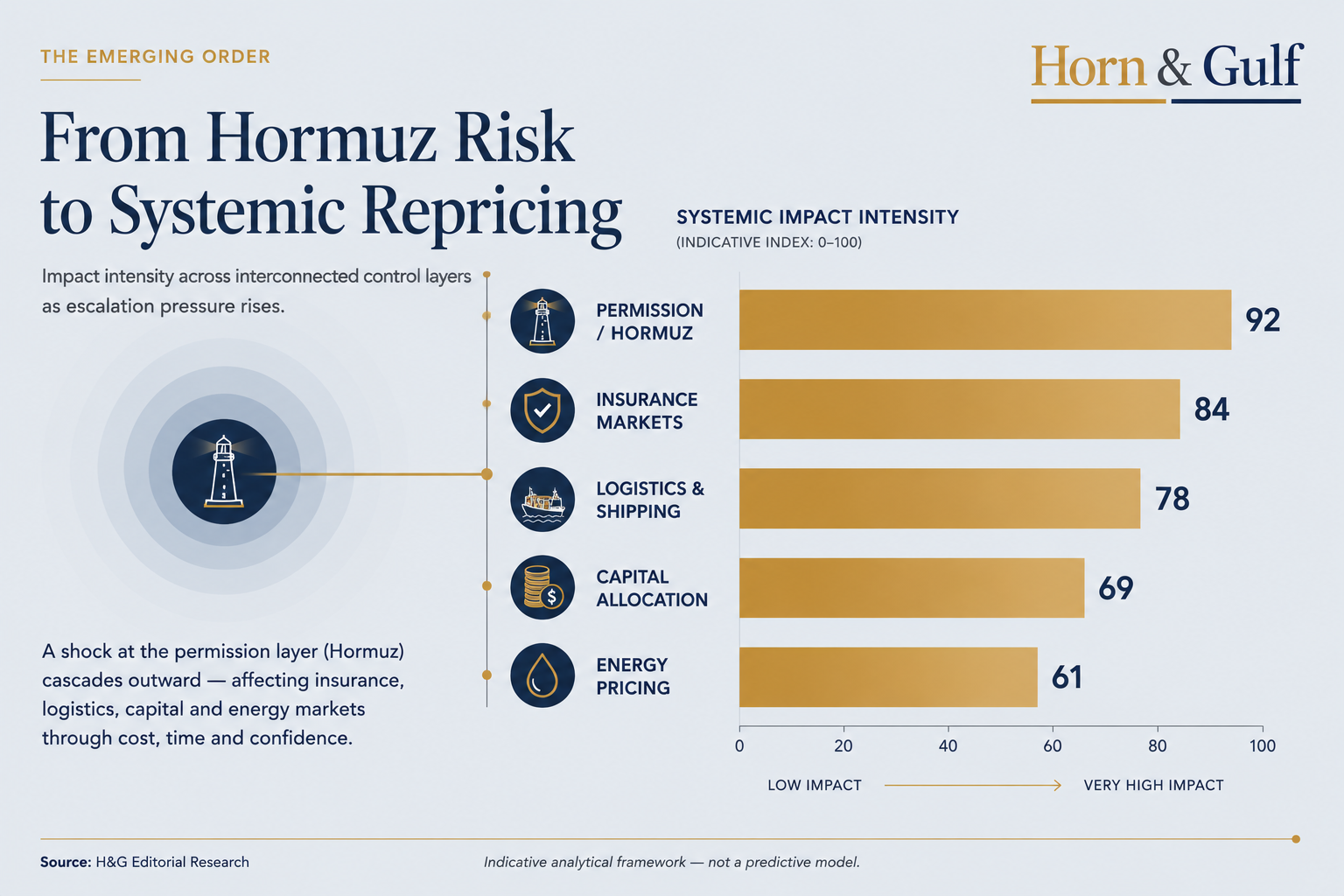

When tensions rise around Iran, the immediate market reaction is still often measured through oil prices. But increasingly, some of the more meaningful signals appear elsewhere first: insurance premiums, shipping confidence, rerouting behavior, freight costs, tanker visibility patterns and capital allocation decisions.

In other words, modern Gulf crises begin affecting pricing mechanisms before major physical disruption occurs. Markets increasingly react not only to damage itself, but also to the probability and perception of disruption.

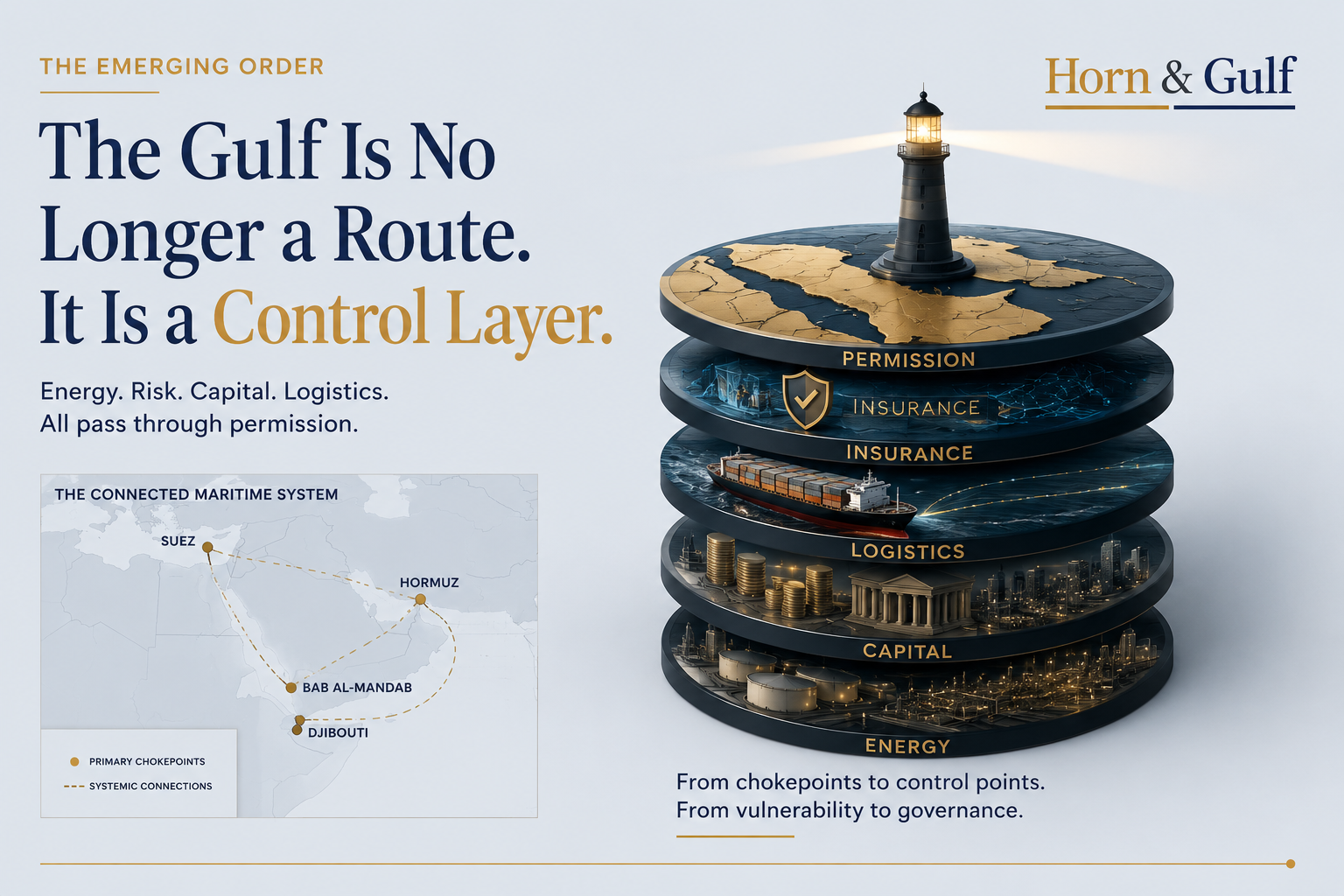

Hormuz Is Becoming a Permission Layer

The Strait of Hormuz remains one of the world’s most critical maritime chokepoints. But reducing Hormuz to a narrow shipping route increasingly misses the structural transformation underway.

Hormuz is no longer simply a corridor. It is increasingly functioning as a permission layer.

The distinction is subtle but important. A route implies movement. A permission layer implies conditional movement shaped by deterrence, surveillance, insurance tolerance, naval presence, political signaling and risk perception.

Even without a full closure scenario — which remains uncertain and operationally difficult — the strategic importance of Hormuz lies in the fact that even limited disruption or perceived instability can introduce friction into the global system.

Delays matter. Insurance repricing matters. Perceived threat and navigational uncertainty matter. Market psychology matters.

Modern maritime pressure is often less about stopping trade entirely and more about introducing enough uncertainty to alter cost structures and strategic calculations across the wider system.

That is why bypass infrastructure has become increasingly important.

The UAE’s Fujairah corridor, Saudi Arabia’s East-West pipeline toward Yanbu, Red Sea port investments and alternative logistics networks are not merely diversification projects. They also reflect broader efforts to strengthen resilience against corridor vulnerability and supply-chain disruption.

The Real War Market May Be Insurance

One of the most underappreciated dimensions of Gulf escalation is that the first major market reaction may emerge not from oil itself, but from insurance.

War-risk premiums, vessel coverage conditions, underwriting confidence and shipping liability calculations frequently begin adjusting before energy supply disruptions fully materialize. This increasingly positions maritime insurance as an important early indicator of geopolitical stress.

Shipping companies do not necessarily wait for physical closure scenarios. They also react to perceived escalation risk.

A sustained perception of instability around Hormuz or the Red Sea can gradually alter route selection, transit costs, fleet deployment and cargo timing. Over time, these adjustments may reshape elements of trade geography itself.

This is particularly important for the Gulf because the region’s economic transformation increasingly depends on predictability, connectivity and capital confidence in addition to hydrocarbons.

A conflict environment therefore creates two parallel realities simultaneously:

the operating environment becomes more complex, while the region itself may become even more strategically indispensable.

That paradox sits near the center of the emerging order.

Capital Does Not Always Leave Crisis Regions

One of the older assumptions in geopolitical analysis is that instability automatically drives capital away from exposed regions. Gulf dynamics increasingly challenge that assumption.

In many cases, capital may not exit the region altogether. Instead, it may reprice internally toward governance systems perceived as more resilient, predictable and internationally connected.

This distinction is critical.

Periods of regional instability can strengthen the relative attractiveness of highly institutionalized Gulf centers capable of offering legal continuity, financial infrastructure, sovereign backing and logistical reliability.

The UAE’s expanding role in finance, insurance and global capital intermediation reflects elements of this broader trend. Saudi Arabia’s large-scale state-capacity expansion operates within a similar strategic logic, though through a different model centered on industrial transformation, infrastructure development and long-term economic diversification.

The result may not necessarily be capital flight from the Gulf.

Instead, the region could experience greater concentration around jurisdictions perceived as stable, connected and operationally resilient.

That possibility may become one of the defining features of the next regional cycle.

The Red Sea Is No Longer Secondary

Much of the international discussion surrounding Iran still focuses overwhelmingly on the Gulf itself. Yet the secondary effects increasingly reshape the Red Sea and Horn of Africa corridor as well.

As pressure rises around Hormuz, Bab al-Mandab naturally gains additional strategic weight.

This changes the importance of Aden, Djibouti, East African ports, Suez-linked infrastructure and Red Sea maritime security architecture. These are no longer merely peripheral transit points operating separately from Gulf dynamics. They are increasingly becoming interconnected variables within the same logistics and security environment.

The consequences extend beyond shipping.

Energy diversification routes, food-security corridors, maritime infrastructure, subsea cable security, port financing and insurance calculations all increasingly intersect across the wider Gulf–Red Sea–Horn system.

The region therefore behaves less like isolated theaters and more like a connected strategic ecosystem.

That shift remains underappreciated in much of the broader international analysis.

The Emerging Order Is About Managed Continuity

The deeper lesson of the Iran crisis may ultimately have less to do with war itself and more to do with how systems adapt under sustained pressure.

The global economy no longer depends solely on uninterrupted stability. Increasingly, it depends on managed continuity under persistent uncertainty.

That distinction defines the current era.

Trade does not fully stop. Energy systems do not fully collapse. Capital does not necessarily disappear. Instead, systems adapt through rerouting, repricing, redundancy, insurance layering and stronger resilience mechanisms.

This is why the Gulf’s role is changing so fundamentally.

The region is evolving from an energy frontier into a strategic control layer linking maritime security, capital protection, logistics continuity and geopolitical risk management.

The old order was built primarily around access to resources.

The emerging order is increasingly being shaped by the management of movement, permission, resilience and systemic trust.