The Dubai property market repricing visible during Q2 2026 appears increasingly tied to regional uncertainty rather than structural weakness in fundamentals. While transaction sentiment softened across parts of the secondary apartment segment, the available data still points to resilient long-term market conditions, particularly in villas, rental yields and ongoing development activity.

A Regional Uncertainty Entered the Market Faster Than the Data Could Explain

For most of the past five years, Dubai’s residential market operated under a relatively consistent assumption: periods of regional uncertainty often reinforced the emirate’s position as a preferred destination for internationally mobile capital. Wealth, businesses and investors increasingly viewed Dubai not simply as a real estate market, but as part of a broader continuity and diversification strategy.

That assumption was tested during the recent period of heightened regional uncertainty.

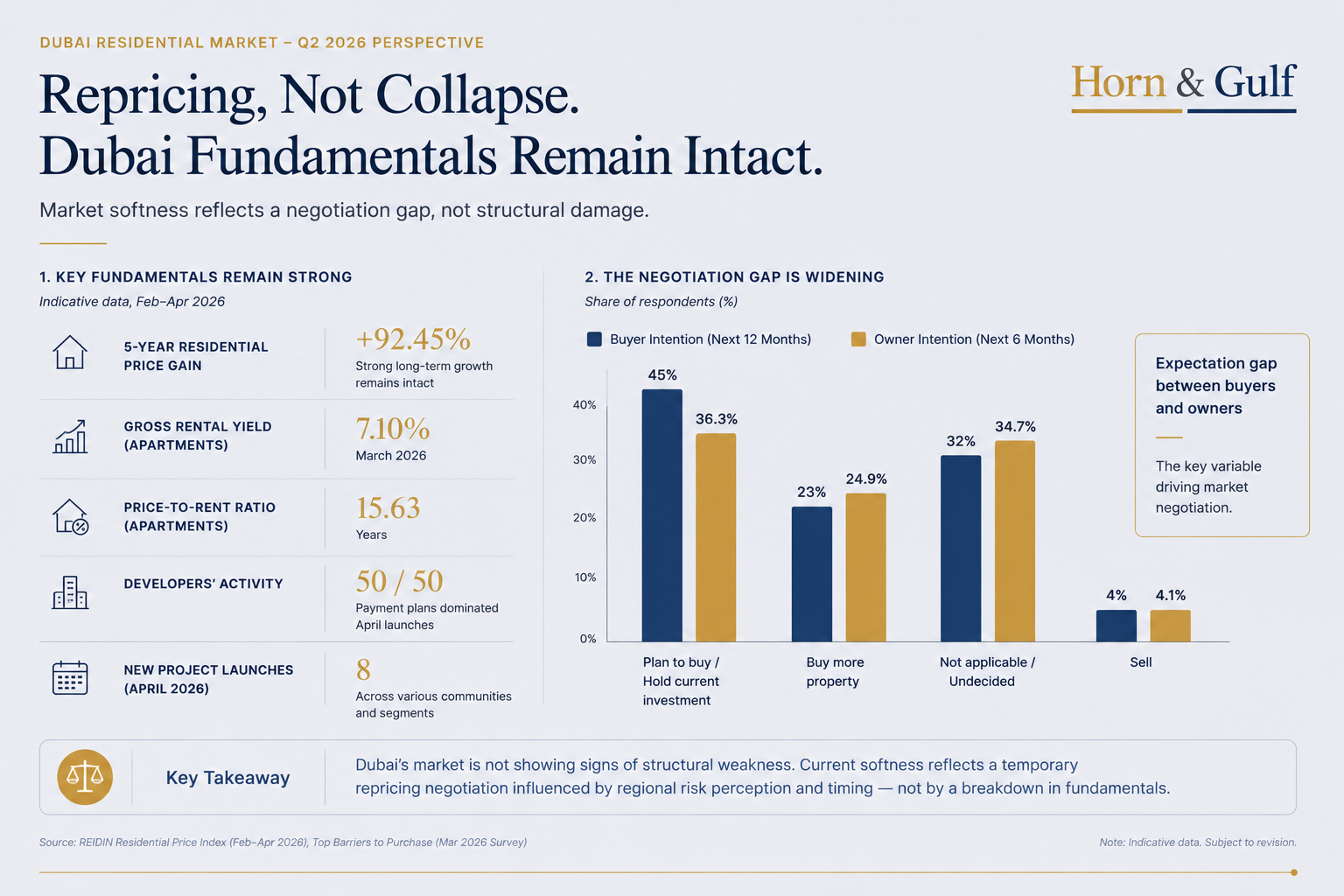

The available data from February through April 2026 does not indicate structural damage to the market. Residential prices remained positive year-on-year, villas continued to outperform apartments, and rental yields above 7% remained visible across parts of the apartment segment. Developers also continued announcing new launches, particularly in mid-market and upper-mid categories.

Yet the market did change. Not structurally, but behaviorally.

The most important signal was not the modest movement in headline prices themselves. It was the widening gap between what buyers expected to pay and what sellers were willing to accept.

That gap may now matter more than the indices alone.

The Market Is Negotiating Risk, Not Pricing Collapse

The recent softness visible in parts of Dubai’s secondary apartment market appears closer to a repricing negotiation than a systemic correction. That distinction matters.

Historically, severe property downturns are often associated with distressed leverage, forced liquidation and rapid deterioration in balance-sheet conditions. There is currently limited evidence in the available data that these dynamics are dominating Dubai’s residential market.

A meaningful share of the market continues to be supported by cash buyers, long-term holders, international capital inflows and relatively stable ownership structures.

This helps explain why many sellers have remained firm despite softer short-term sentiment. The issue does not currently appear to be panic selling. It is hesitation.

Some buyers increasingly want regional uncertainty reflected more clearly in pricing. Sellers, meanwhile, continue to anchor valuations around Dubai’s longer-term structural strengths:

- infrastructure continuity,

- capital mobility,

- aviation connectivity,

- legal predictability,

- and relative economic resilience.

Both sides are therefore pricing different time horizons.

Buyers are reacting to short-term uncertainty across the wider regional environment. Sellers are pricing the continuation of Dubai’s long-term capital attraction model.

That divergence appears to be contributing to the negotiation gap emerging across parts of the market.

Dubai’s Property Market Is Becoming More Sensitive to Regional Risk Perception

The deeper structural shift may be that Dubai property pricing is no longer functioning purely as a local supply-demand story. It is increasingly influenced by the wider regional risk environment.

Recent discussions surrounding maritime security, shipping continuity and regional escalation scenarios did not directly affect Dubai’s real estate infrastructure. However, they may have altered broader perceptions surrounding continuity, stability and investment timing across the region.

That matters because Dubai’s economic model is deeply interconnected with:

- maritime logistics,

- aviation flows,

- financial services,

- tourism continuity,

- and cross-border capital movement.

The Emirate’s property market therefore behaves less like an isolated housing market and more like a confidence-sensitive component within a larger Gulf economic system. This is where many conventional real estate readings remain incomplete.

The question is no longer simply: “Are Dubai’s fundamentals strong?”

The more important question may be: “How does regional uncertainty temporarily influence the pricing of those fundamentals?”

That is a different analytical framework from the traditional boom-and-bust property narrative.

The Hidden Layer May Be Timing, Not Demand

The most underpriced dimension of the recent market hesitation may not be construction activity or long-term demand. It may be timing and confidence perception.

Periods of heightened regional uncertainty often affect expectations before they affect asset values directly.

Shipping insurers may reassess exposure assumptions.

Freight routes can become more cautious operationally.

Aviation and travel-related risk assessments may tighten temporarily.

Some corporate treasury departments may delay regional allocation decisions.

Certain family offices may slow deployment activity until visibility improves.

None of this necessarily indicates structural deterioration. But it can affect transaction timing and market velocity.

This matters because Dubai increasingly functions as a regional coordination hub for trade, logistics, finance and wealth management. Even temporary uncertainty around maritime corridors or regional escalation scenarios can influence transaction behavior across sectors connected to international capital movement.

In this sense, Dubai real estate is increasingly behaving as a confidence-sensitive asset class. The property itself is only part of the equation. The larger variable is perception surrounding regional continuity.

Not All Segments Are Behaving the Same Way

One weakness in many broad market narratives is the tendency to describe “Dubai real estate” as a single market.

The reality is more segmented.

Prime villas and trophy assets continue to demonstrate relative resilience because they are more closely connected to long-term wealth preservation strategies. These buyers are generally less sensitive to short-term volatility and often allocate capital with multi-year horizons.

Secondary apartments, particularly within highly competitive inventory clusters, appear more sensitive to financing conditions, investor caution and transaction liquidity.

This divergence matters. It suggests the market is not experiencing uniform stress. Instead, it is experiencing selective repricing across different segments.

That distinction may become increasingly important during the next phase of the cycle.

The Larger Question Extends Beyond Property Data

The most important conclusion is also the most difficult to quantify. Dubai’s underlying fundamentals continue to appear relatively resilient:

- infrastructure capacity remains intact,

- rental yields remain internationally competitive,

- development activity continues,

- and there is no clear evidence in the cited data of a structural reversal in market confidence.

However, the pace at which buyer confidence normalises will likely remain connected to the broader regional environment through the rest of Q2 and beyond.

No single property index can fully answer that question. Because the market is no longer pricing only real estate fundamentals.

It is increasingly pricing perceptions of regional continuity, economic resilience and cross-border stability. That may become one of the defining characteristics of Gulf capital markets in the years ahead.

Dubai’s property sector is therefore not simply facing a cyclical pause. It is increasingly operating within a broader repricing environment where logistics continuity, maritime stability, capital mobility and regional confidence interact simultaneously.

The fundamentals remain resilient. But resilience itself is now being evaluated through a wider geopolitical and economic lens.