Hormuz shipping rates are no longer driven only by physical access through the Strait. The recent dispute surrounding TD3C freight benchmarks highlights how insurance costs, legal uncertainty and market confidence are becoming central to maritime pricing in the Gulf energy system. The issue is no longer simply whether vessels can transit Hormuz. It is whether that transit can still be priced, hedged and insured under commercially stable conditions during geopolitical disruption.

A Market That No Longer Prices Risk Normally

Hormuz shipping rates are no longer shaped only by physical access through the Strait. The recent dispute surrounding TD3C freight benchmarks suggests that insurance costs, legal uncertainty and market confidence are becoming central to maritime pricing in the Gulf energy system.

The issue is no longer simply whether vessels can transit Hormuz. The more important question is whether that transit can still be priced, hedged and insured under commercially stable conditions during geopolitical disruption.

Available reporting indicates that the dispute between Mercuria and the Baltic Exchange centres on whether TD3C adequately reflected market conditions during the recent Hormuz disruption. The case has drawn attention because TD3C underpins parts of the tanker freight market, including contracts and derivatives linked to Middle East Gulf crude shipments.

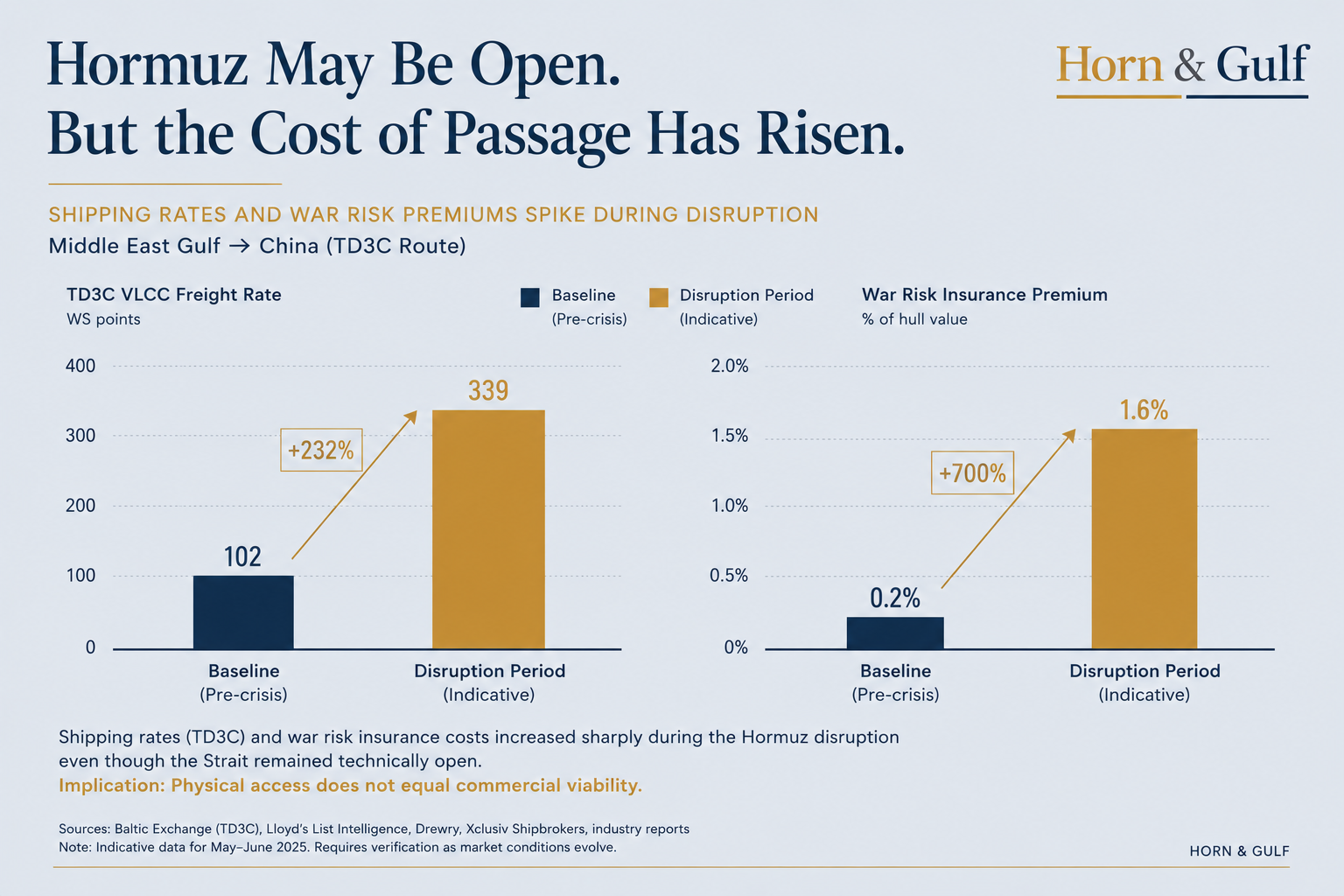

At the centre of the case is TD3C, the Baltic Exchange route assessment for VLCC crude shipments from the Middle East Gulf to China. The benchmark influences parts of the shipping, trading and derivatives ecosystem. According to publicly available reporting, Mercuria argues that the benchmark became less representative during the period of heightened disruption around Hormuz. Baltic maintains that the Strait was not formally closed to lawful commercial traffic.

When Open Routes Become Commercially Distorted

This is where the issue becomes structural rather than purely operational.

A maritime corridor can remain legally and physically open while becoming commercially distorted under stress. Ships may continue to move. Some cargoes may still clear. Naval protection may reduce part of the security risk. Yet the market environment can still deteriorate.

Insurance costs may rise sharply. Liquidity may thin. Private operators may hesitate. Only certain actors may remain willing or able to transit the route under exceptional conditions.

Under those conditions, the market may no longer be observing normal commercial activity. Instead, it may be observing a stressed corridor through a benchmark designed for more stable market environments.

That distinction matters because modern energy trade depends on more than ports, vessels and physical cargoes. It also depends on the credibility of reference prices. Benchmarks help traders, shipowners, insurers and financial institutions operate within a shared framework of market assumptions.

When confidence in those assumptions weakens, the effects can extend beyond the immediate disruption itself.

The Financial Layer of Maritime Risk

The Mercuria–Baltic dispute points to a broader vulnerability within the maritime system. Chokepoint risk is becoming increasingly financial as well as physical.

The question is no longer only whether a tanker can transit Hormuz. It is also whether that transit can be priced, hedged, insured and contractually managed under conditions that market participants continue to regard as commercially representative.

If confidence around those conditions weakens, then the Strait of Hormuz becomes more than a strategic maritime chokepoint. It also becomes a pricing chokepoint.

This is an underappreciated dimension of the current environment. Much Gulf security analysis traditionally focuses on interruption: closure, blockade, military escalation or physical supply shock. Those risks remain important. Yet partial functionality can also create systemic strain, particularly when contracts continue operating while the assumptions beneath them become less stable.

In such an environment, legal and commercial interpretation becomes increasingly important. Was the route closed or simply operating under elevated risk? Did benchmarks continue to reflect real transaction conditions? Were losses caused primarily by conflict, reduced liquidity, methodology limitations or commercial decisions taken by market participants themselves?

These are not merely theoretical questions. They shape liability, settlement exposure and contractual interpretation across multiple parts of the maritime economy.

Insurance, Capital and the Repricing of Passage

The insurance layer is particularly significant. War-risk premiums, exclusions, reinsurer appetite and route classifications can gradually reshape commercial behaviour before governments formally alter policy.

A corridor may remain navigable while becoming commercially difficult for parts of the private market. Once that occurs, shipping economics begin to reflect not only geography, but also protection costs, legal certainty and risk-transfer capacity.

The Gulf, the Red Sea and the Horn of Africa are increasingly interacting as components of a broader maritime risk architecture. Recent Red Sea disruptions already demonstrated how rerouting decisions can alter freight costs, insurance exposure and delivery timelines.

Hormuz introduces an additional lesson. Even when a corridor remains partially operational, confidence in the benchmark layer itself can become contested.

That uncertainty is likely to influence capital behaviour over time.

Energy traders may seek wider risk buffers. Shipowners may require higher compensation for uncertainty. Insurers and reinsurers may reassess exposure models. Banks financing vessels and cargoes may place greater emphasis on route-related risk assessment.

Gulf producers may also need to consider not only export capacity, but the resilience and credibility of the pricing infrastructure surrounding key maritime corridors.

The Long-Term Shift Beneath the Crisis

This may represent a medium-term structural shift. Maritime influence is no longer measured solely through physical control of sea lanes. It is increasingly linked to the ability to preserve commercially credible conditions for trade, insurance and financial settlement during periods of geopolitical stress. The longer-term implications may prove more consequential.

If confidence in benchmark systems weakens during repeated crises, maritime chokepoints may become more deeply embedded in the legal and financial architecture of global trade.

The centre of gravity may gradually shift from naval escort operations toward arbitration rooms, insurance committees, freight derivative markets and commercial litigation.

In that sense, the economic afterlife of a maritime crisis may continue well beyond the period of direct disruption itself. Hormuz may stabilize. Tanker flows may normalize. Freight markets may recover. Yet the broader lesson may remain: physical openness and market confidence are not necessarily the same condition.

If confidence in benchmark reliability weakens during periods of geopolitical stress, the cost of passage may increasingly be measured not only in freight rates, but also in legal exposure, insurance uncertainty and the repricing of strategic maritime risk across the Gulf energy system.