The Horn of Africa vulnerability debate is no longer limited to domestic fragility alone. As tensions around Iran pressure Gulf maritime systems and energy corridors, the Red Sea and Gulf of Aden are becoming increasingly exposed to secondary economic and logistical shocks.

For African states positioned near these routes, the challenge is not only geopolitical proximity — but institutional capacity under external pressure.

The Horn of Africa May Still Absorb the Shock

The war surrounding Iran is not African in origin. Yet Africa is not outside its consequences. The first analytical mistake would be to treat the crisis as a distant Middle Eastern confrontation with limited relevance to the African continent. The second would be to assume that every external shock automatically produces continental-scale structural transformation.

The more disciplined reading sits between those two errors.

The immediate signal is increasingly difficult to ignore. A confrontation involving Iran, Israel and the United States places pressure on the energy corridors, maritime routes and political alignments linking the Gulf, the Red Sea and the Horn of Africa. The Strait of Hormuz matters not only because of the volume of energy that passes through it, but because it functions simultaneously as an energy artery, a pricing mechanism and a psychological pressure point for import-dependent economies.

The Red Sea and Gulf of Aden matter because they form the African-facing continuation of that system.

The central question, therefore, is not whether Africa is exposed. The more important question is how that exposure travels — and whether it manifests as temporary economic stress, political pressure or longer-term strategic adjustment.

The Immediate Reality

For many African economies, the first transmission channel is economic rather than military. Higher fuel prices, shipping delays, currency pressure and food-import costs tend to move faster than diplomatic positioning. In countries where transport systems, electricity generation and food distribution networks already operate under strain, even limited disruption can become socially and politically visible.

The Horn of Africa is more exposed than many other regions because geography compresses multiple vulnerabilities into a single corridor. Djibouti, Somalia, Ethiopia, Eritrea, Sudan and Kenya sit adjacent to the Red Sea, Gulf of Aden and Western Indian Ocean maritime system. They are not merely near crisis routes. They are part of the logistical and security environment through which Gulf instability is absorbed and managed.

This does not automatically mean the region is moving toward large-scale escalation. It means the operational margin for error is narrow.

The Underestimated Layers

Most public discussion around the crisis remains too narrowly focused on military confrontation itself. Several deeper layers receive insufficient attention.

The first is the insurance layer.

Modern maritime disruption is often priced before it is physically enforced. War-risk premiums, chartering behavior, rerouting decisions, vessel tracking patterns and port congestion can alter trade flows even when major sea lanes technically remain open. In practice, perception can reshape commercial behavior before physical interruption becomes measurable.

The second is the Gulf resilience layer.

Gulf states are not passive transmitters of instability. Regional governments have spent years building redundancy through ports, storage infrastructure, pipeline diversification, logistics hubs, sovereign investment capacity and diplomatic balancing mechanisms. Any serious reading of African exposure must account for the continuity-management capabilities that exist within the Gulf itself.

The third is the market psychology layer.

Energy prices, freight costs and food-import pressures are influenced not only by physical disruption, but also by expectation, hedging behavior and risk anticipation. For import-dependent economies, the perception of prolonged instability can generate economic consequences before structural shortages fully emerge.

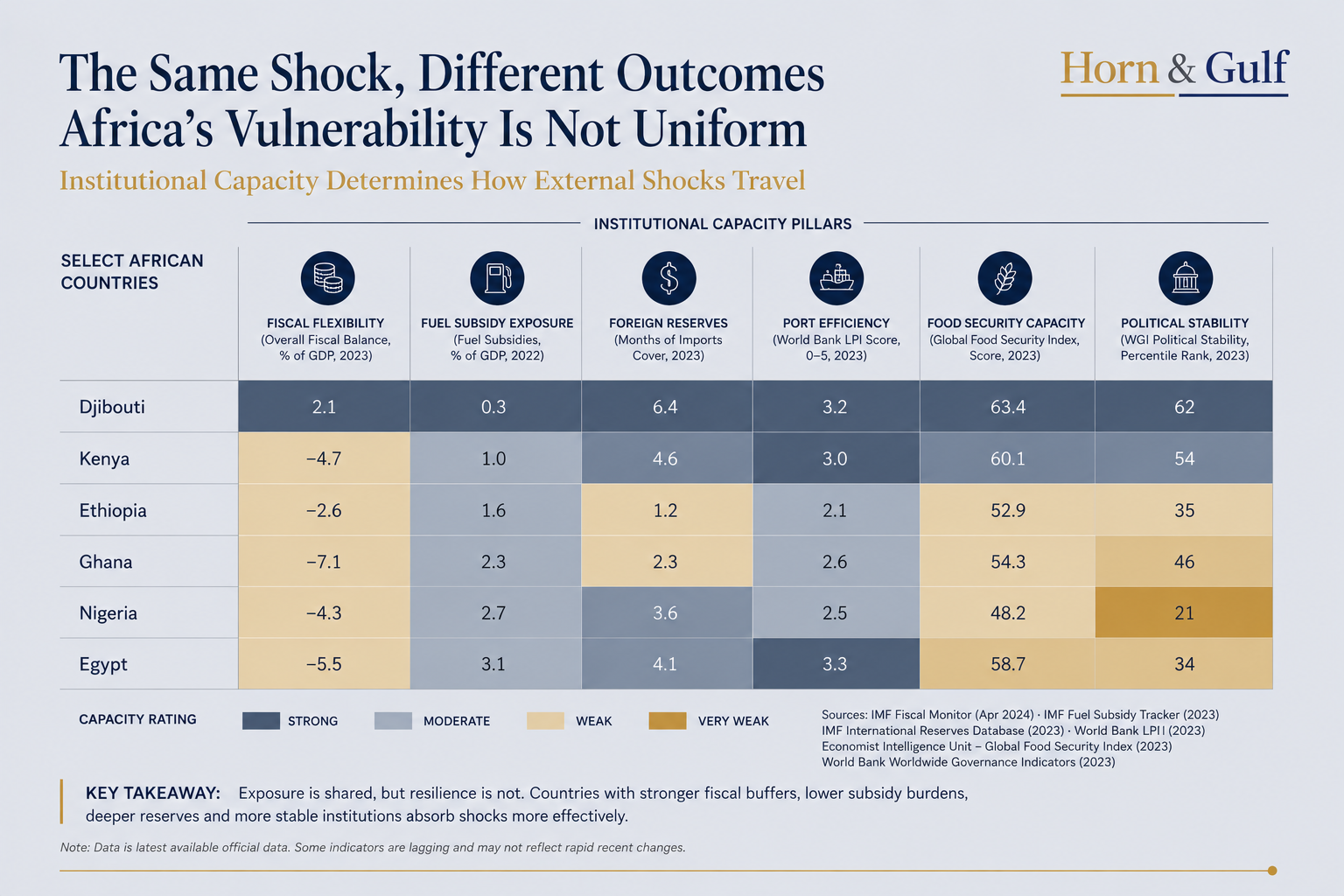

The fourth is the institutional-capacity layer.

African vulnerability is not uniform. The same external shock will produce very different outcomes depending on fiscal flexibility, fuel-subsidy exposure, foreign reserves, port efficiency, food-security capacity and domestic political resilience.

The H&G Interpretation

From an H&G perspective, the most important development is not simply that Africa may be affected by a Middle Eastern conflict. The deeper issue is that the Gulf, Red Sea and Horn of Africa systems are becoming increasingly difficult to separate into isolated regional categories.

Hormuz may function as the initial pressure point. The Red Sea may operate as the maritime continuation of that pressure. The Horn may become part of the logistical and political absorption environment surrounding the crisis.

But these relationships should not be overstated.

Not every disruption represents a systemic transformation. Not every maritime crisis produces a new geopolitical architecture. In some cases, these connections emerge less from coordinated strategy than from geography, insurance exposure, shipping behavior and uneven institutional capacity.

That distinction matters.

The most important structural implication is not inevitable collapse or regional fragmentation. It is that states positioned near the Red Sea are increasingly exposed to disruptions they do not fully control, but must still economically absorb, politically manage and operationally navigate.

That exposure operates across three levels.

The first is operational: shipping delays, fuel-price volatility, port pressure and supply-chain uncertainty.

The second is political: inflation pressure, food-cost sensitivity and public frustration linked to broader economic conditions.

The third is strategic: external security arrangements, maritime corridors and Gulf partnerships may become more sensitive as governments and commercial actors reassess risk, continuity and access.

The Counter-Argument

A disciplined framework must also acknowledge what may weaken this thesis.

The crisis may remain geographically contained. Energy markets may absorb disruption more effectively than anticipated. Gulf continuity mechanisms may preserve shipping stability. Commercial adaptation may prevent sustained rerouting. Inflationary pressure across African economies may ultimately prove more connected to domestic fiscal and currency conditions than to Gulf instability itself.

It is also possible that analysts are overextending the “corridor transformation” framework onto events that remain temporary in nature.

That possibility deserves serious consideration.

The H&G framework should not force every disruption into a theory of systemic repricing. The more cautious interpretation is that the Iran crisis does not automatically transform Africa’s strategic position. Rather, it reveals where structural pressure could emerge if instability becomes prolonged.

The Underpriced Dimension

The most overlooked dimension is not energy alone. It is the interaction between energy costs, food security, insurance pricing and governance pressure.

For fiscally constrained states, the danger is not simply higher prices in isolation. It is the chain reaction through which higher prices travel across the social and economic system. Fuel affects transport costs. Transport affects food distribution. Food inflation affects urban stability. Currency pressure affects import capacity. Import strain affects public confidence.

Under those conditions, a maritime-security disruption can gradually evolve into broader governance pressure even without direct military spillover onto African territory.

This is where the Horn of Africa remains particularly exposed. Its vulnerability is not only geographic. It is also institutional.

Time Horizon

Over the next 24 to 72 hours, the most important indicators remain energy prices, shipping behavior, Gulf diplomatic signaling, Red Sea security alerts and any signs of maritime escalation.

Over the next 3 to 12 months, the more important question is whether temporary disruption evolves into long-term planning behavior. If insurers, shipping companies, Gulf states and African governments begin treating the Gulf–Red Sea corridor as persistently unstable, commercial adaptation may occur before physical infrastructure changes.

Over the next 1 to 10 years, the strategic implications become larger. States along the Red Sea and Western Indian Ocean may gradually reassess port policy, food-security reserves, fuel-storage capacity, maritime-security arrangements and Gulf economic partnerships. Under sustained pressure, the crisis could evolve from a temporary shock into a broader strategic forcing mechanism.

Humility Layer

Several critical variables remain unclear.

It is not yet clear whether the conflict will remain contained or widen geographically. It remains uncertain whether shipping disruption will prove episodic or sustained. It is also unclear how effectively existing Gulf resilience systems can absorb prolonged pressure without broader regional consequences.

At the same time, H&G may still be underestimating the adaptability of commercial shipping systems, insurers, energy markets and Gulf logistics infrastructure.

The thesis would weaken significantly if energy flows stabilize rapidly, war-risk pricing normalizes, Red Sea shipping remains manageable and African inflation dynamics continue to be driven primarily by domestic structural conditions rather than external maritime disruption.

For now, the most credible conclusion remains calibrated rather than dramatic.

Africa is not outside the Iran crisis. The Horn of Africa is particularly exposed to its secondary effects. But exposure alone does not predetermine systemic rupture.

The more important question is whether regional governments interpret this period merely as another external shock to absorb — or as evidence that maritime security, Gulf stability and global risk pricing are becoming increasingly central to African economic resilience itself.