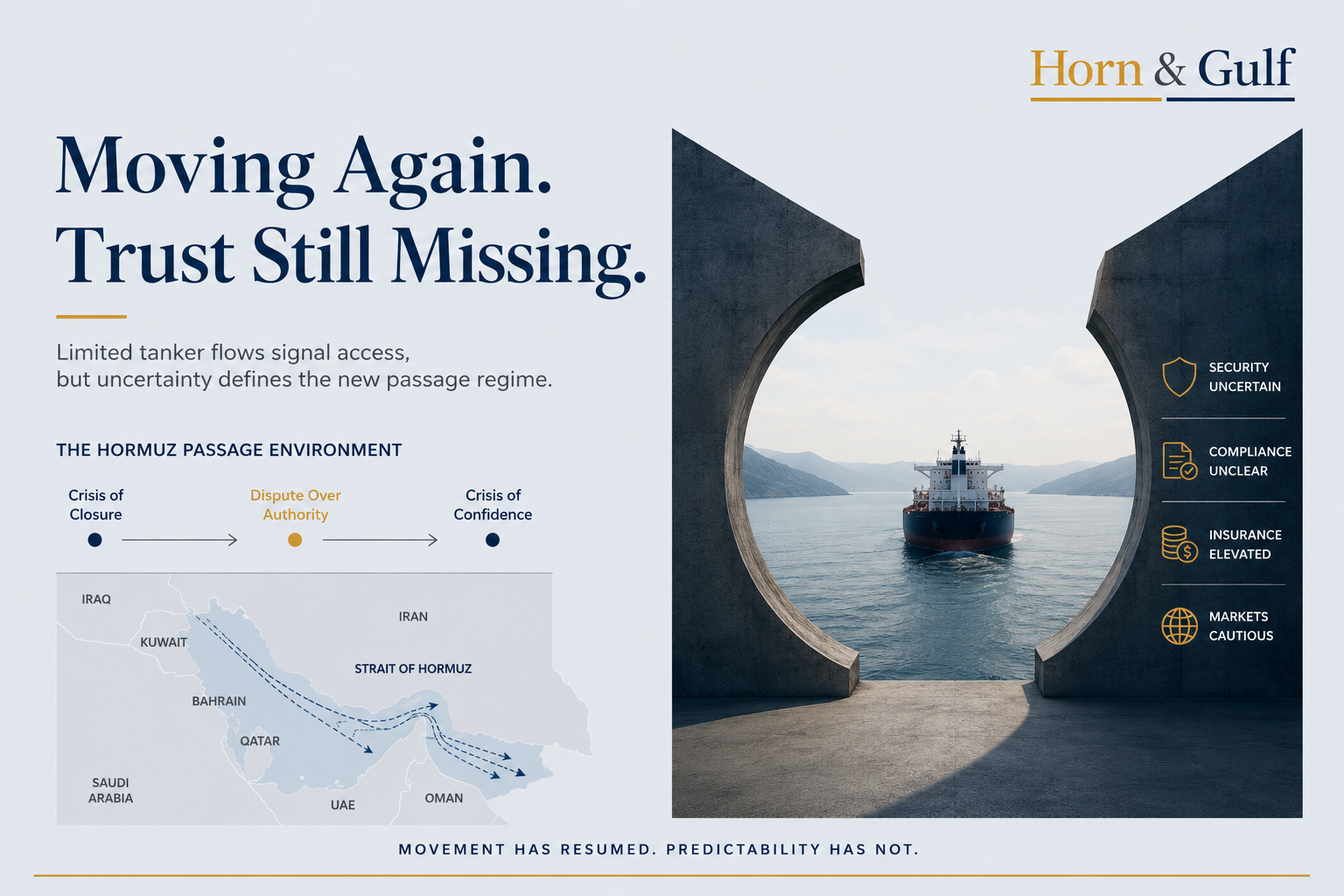

Hormuz tanker traffic has started to recover after recent disruptions, with limited oil and LNG cargoes moving again toward Asian markets. Yet the Strait of Hormuz has not returned to operational normality, as insurers, shipowners and energy markets continue to price uncertainty into Gulf maritime activity.

Limited Movement Returns to Hormuz

The first signal emerging from Hormuz is not resolution. It is limited movement under unresolved political uncertainty.

In recent days, a small number of oil and LNG tankers resumed movement through the Strait of Hormuz toward Asian markets. Several Qatar-linked LNG cargoes appear to have moved toward Pakistan and China. Additional energy shipments also exited the Gulf under uneven operational conditions.

At first glance, this may look like partial reopening. Strategically, however, the picture remains more complicated.

The key question is no longer whether vessels can move through Hormuz. Some clearly can.

The deeper question is whether the passage environment is becoming predictable again.

That remains uncertain.

Diplomatic Signals Remain Mixed

Recent reports surrounding a possible informal understanding between Tehran and Washington should be approached carefully.

At this stage, the situation appears less like a formal diplomatic breakthrough and more like a combination of negotiation signaling, market messaging and strategic positioning.

This distinction matters.

A Strait of Hormuz that is partially functioning is not necessarily a Strait of Hormuz that has returned to operational normality.

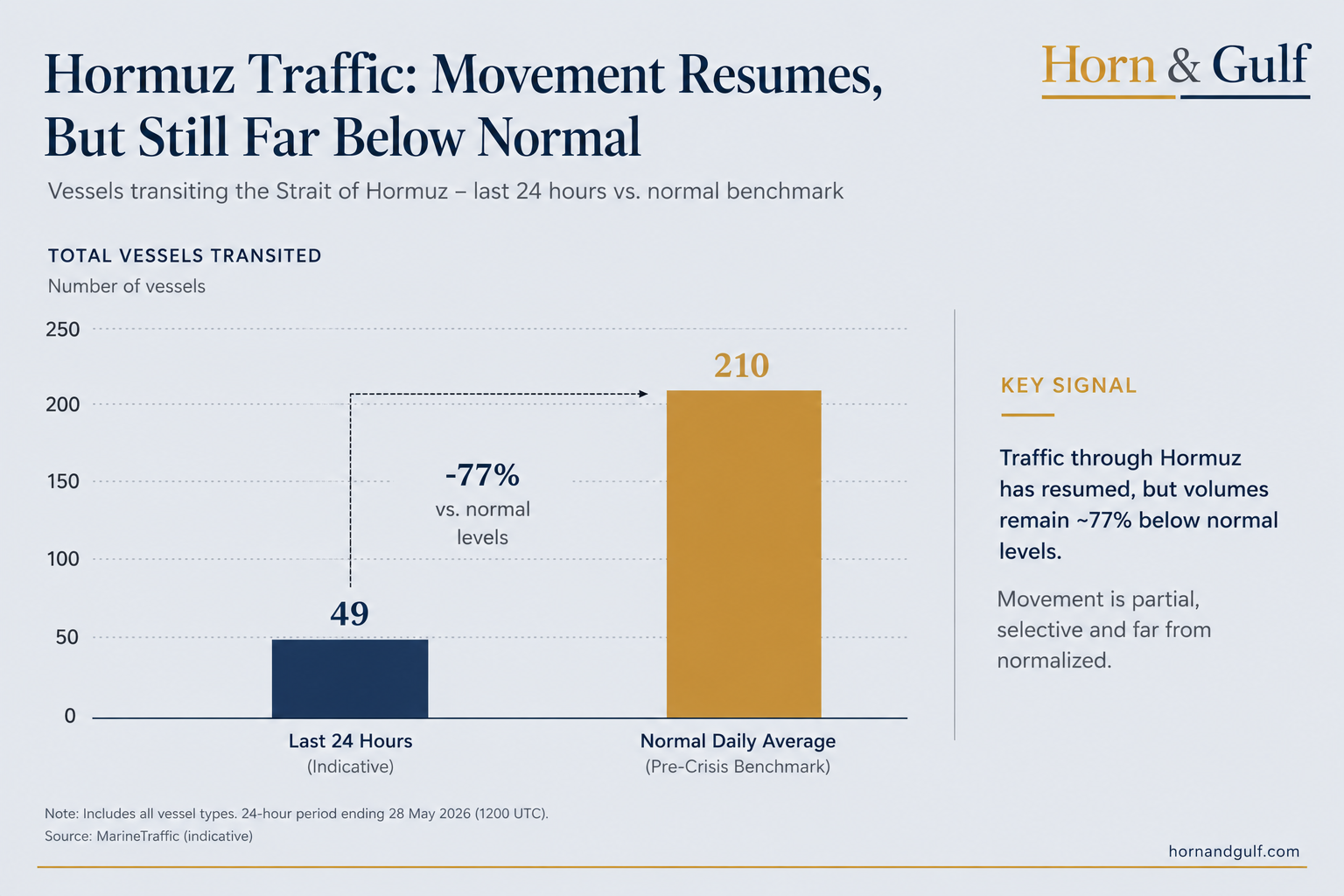

The immediate reality remains mixed. Limited tanker traffic has resumed. Some Asian buyers appear willing to receive selected cargoes. Qatar’s LNG flows are receiving particular attention because they sit at the intersection of Gulf energy stability and Asian demand security.

Yet movement alone does not restore confidence.

Why Predictability Matters More Than Access

In maritime systems, predictability often matters more than technical access itself.

A shipping corridor may remain commercially constrained even when physically open if the surrounding military, insurance, legal and compliance environment remains uncertain.

This is where the Hormuz story begins to acquire a broader structural dimension.

Recent discussions surrounding possible passage-management mechanisms or additional transit arrangements suggest that the debate may gradually be shifting away from simple closure scenarios toward questions of authority, legal exposure and operational conditions of passage.

That does not mean a new maritime system has emerged. Nor does it mean any proposed framework has gained broad acceptance.

However, it does indicate that the strategic conversation itself may be evolving.

The Emerging Risk Question

For H&G, the central interpretation should remain disciplined and cautious.

Hormuz may be moving from a crisis centered on physical disruption toward a broader dispute over passage conditions, risk allocation and operational predictability.

The old binary framework — open or closed — increasingly appears insufficient.

The emerging issue is more complex:

- Who defines acceptable passage conditions?

- Who absorbs insurance and compliance costs?

- How much uncertainty can global energy systems tolerate before commercial behavior begins to adjust?

The Counter-Argument Should Not Be Ignored

There is also a strong counter-argument to the broader structural thesis.

This may still prove to be temporary turbulence rather than durable transformation.

Iranian messaging may primarily reflect negotiation positioning. Washington’s responses may aim to prevent premature normalization of unofficial transit arrangements. Tanker operators may simply be testing the corridor under exceptional conditions while broader market systems remain fundamentally resilient.

That possibility should not be dismissed.

The strongest argument against overinterpretation is straightforward.

Limited tanker movement alone does not constitute a new regional order. A small number of LNG or oil cargoes cannot by themselves prove structural realignment. Nor do disputed diplomatic signals establish a durable framework for passage governance.

What would strengthen the larger thesis is persistence.

Repeated controlled transits, sustained insurance repricing, formal compliance guidance, state-backed transit arrangements or long-term adjustments in buyer and shipowner behavior would carry far greater significance than isolated vessel movement.

Until then, caution remains necessary.

Insurance and Compliance Remain Underpriced

Even provisional signals matter in Hormuz because the corridor operates at the intersection of energy security, sovereign risk, maritime insurance and strategic deterrence.

The Strait is not simply a waterway. It also functions as a pricing mechanism for Gulf stability.

When operational assumptions change — even partially — the effects extend beyond shipping lanes. They reach LNG contracting behavior, Asian energy planning, Gulf fiscal calculations, naval positioning and strategic infrastructure investment.

One underpriced dimension remains insurance and compliance risk.

Markets often focus primarily on whether oil or LNG physically moved through the corridor. Yet the deeper issue is whether cargoes can move without abnormal legal exposure, sanctions uncertainty, elevated war-risk premiums or unclear compliance arrangements.

If commercial passage increasingly depends on negotiation, exception management or politically sensitive coordination mechanisms, then the corridor may remain operationally open while still commercially impaired.

That is not full normalization.

Gulf States Continue to Hedge Beyond Hormuz

The medium-term implication is likely to reinforce existing Gulf diversification strategies.

Saudi Arabia’s Red Sea orientation, the UAE’s Fujairah infrastructure logic, Qatar’s LNG diplomacy and broader investment into alternative logistical resilience mechanisms all become more strategically relevant in this environment.

These developments should not automatically be interpreted as replacements for Hormuz.

They are more accurately understood as strategic hedging mechanisms against excessive dependency on a single chokepoint.

The Longer-Term Strategic Signal

The longer-term implication is more subtle.

If the current crisis leaves a durable psychological imprint on insurers, sovereign investors, shipowners and Asian buyers, then Hormuz-related risk may remain embedded in strategic planning even after immediate tensions cool.

Large systems do not always change because routes close completely.

Sometimes they change because confidence in previous assumptions weakens.

That may be the more important signal emerging now.

Hormuz is not fully closed. However, it has not fully returned to normal operational confidence either.

The Strait currently exists in the grey zone between access and certainty.

Final Reading

The current moment does not yet prove the emergence of a new maritime order. However, it does suggest that the old language of simple “reopening” may no longer be sufficient to describe the evolving reality.

What is increasingly being tested is not only traffic flow, but also operational confidence, risk allocation and the political management of uncertainty itself.

The next indicators will matter more than the current headlines:

- sustained tanker movement

- insurance pricing behavior

- compliance guidance

- Gulf diplomatic coordination

- operational behavior of major Asian energy buyers

What remains unclear is whether the present situation represents the beginning of a deeper structural adjustment or simply a temporary period of crisis-management turbulence.

H&G may also be underestimating the speed at which commercial systems can normalize once immediate military risks decline.

The broader thesis would weaken considerably if tanker traffic rapidly returns to pre-crisis levels, insurance markets stabilize, escalation subsides and no durable passage-management structure emerges.

For now, the most disciplined conclusion remains this:

Hormuz is reopening in movement, but not yet in confidence.