The Hormuz toll regime has become one of the most consequential issues in Gulf maritime governance since the Doha ceasefire negotiations began. Rather than focusing only on security, policymakers and investors must now assess how a potentially permanent toll authority could reshape regional incentives, sanctions exposure and access to the Strait of Hormuz.

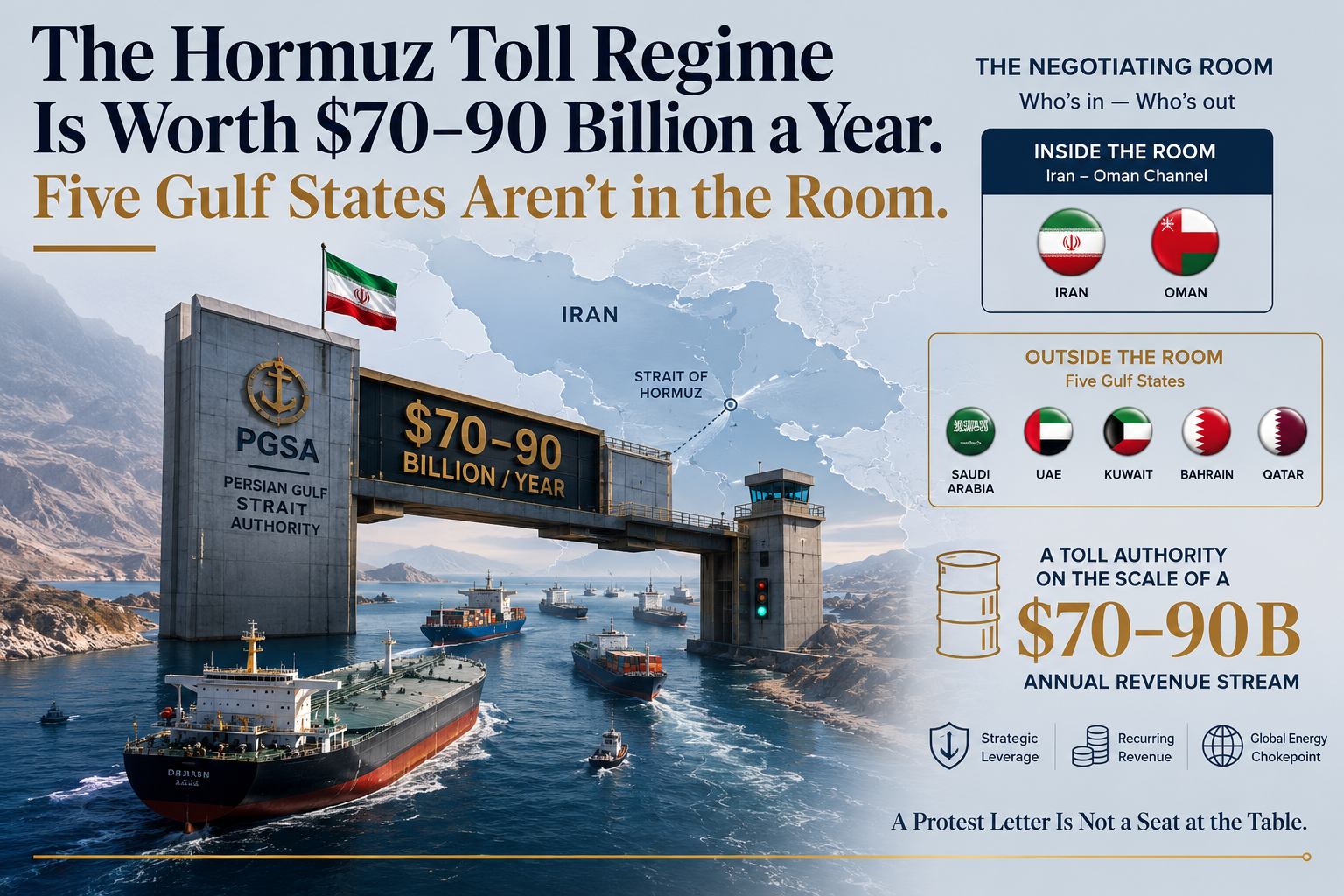

Horn and Gulf argued on July 1 that the real Hormuz negotiation is not happening at the Doha ceasefire talks. It is happening in a narrower channel between Iran and Oman. That conclusion still holds, and this piece will not revisit it. Instead, it examines a number that deserves its own scrutiny. J.P. Morgan estimates that Iran’s Persian Gulf Strait Authority could generate $70–90 billion a year, if its toll structure survives the current negotiating window. Reporters have cited that figure and moved on. It deserves more attention, because it reframes the PGSA. This is not a wartime irritant. It is a fiscal instrument on the scale of a mid-sized sovereign budget. And the list of parties with no formal say in its future is longer than the list with one.

A Number Large Enough to Change Iran’s Incentives

Iran built the PGSA during a war. The U.S. Treasury Department describes Tehran’s government as cash-starved under its “Economic Fury” sanctions campaign. That context matters for sizing this number. A toll authority worth $70–90 billion a year is not a marginal revenue line for a sanctioned economy. Reports during the crisis put individual per-vessel charges as high as $2 million. Historically, more than 100 vessels transited the strait each day. Even at a fraction of pre-war traffic, and a fraction of the maximum toll, the PGSA’s revenue potential sits in a different category from Tehran’s past negotiating leverage.

Sanctions relief, prisoner exchanges, frozen-asset unlocks: these were one-time or episodic tools. A functioning toll authority generates recurring revenue instead. Recurring revenue changes what a government will trade away at the table. So the current 60-day toll suspension is not an ordinary concession. Tehran is deferring a revenue stream large enough to give it strong reasons to keep the underlying authority intact once the suspension lapses — regardless of what else the Doha talks produce.

A Protest Letter Is Not a Seat at the Table

Five Arab Gulf states depend directly on the strait the PGSA claims to administer, through oil exports and import routes alike. They responded to the authority’s creation with a formal joint letter of objection. That letter did real diplomatic work. It put on record that Riyadh, Abu Dhabi, Kuwait City, Manama and Doha reject the authority’s legitimacy, and it warned against treating the PGSA as a workable precedent.

But the letter secured none of those five governments a formal role in the Iran-Oman channel now shaping the strait’s post-war administration. Oman notably did not sign it. Muscat has itself rejected the PGSA’s toll principle publicly, so that is not the reason. Oman sits in a different position from the other five: it is the strait’s co-littoral state, and therefore Iran’s only necessary governance counterpart under the international law that governs straits used for global navigation. A protest letter states a position. A seat in the room where the strait’s administration is actually being negotiated is a different asset — and right now, only one Gulf state holds anything resembling one.

Who Is Priced Out and Who Is Priced In

Sovereign wealth funds and institutional investors should model a specific number: $70–90 billion in potential annual revenue, flowing to an entity under active OFAC sanctions. Even partially realized, that scale of recurring income would materially expand Tehran’s capacity to fund regional activity. Military reconstitution, proxy support and sanctions-evasion infrastructure all become easier to finance. Investors who assume a nuclear deal caps Iran’s resources are working from an incomplete balance sheet, if the PGSA’s institutional shell survives intact.

For Gulf policy planners, the protest letter carries a procedural lesson. A joint statement of objection does not substitute for formal accession to the channel where the administrative facts are being set. The five signatories registered a grievance. They did not register a claim to participate. Their near-term choice is direct: press Oman and Qatar, the two Gulf states with functioning access to the Muscat channel, to carry a formal request for inclusion before the 60-day suspension lapses. The alternative is to keep objecting from outside the process.

Creditors and trade-finance institutions with exposure to Hormuz-transiting cargo should reclassify the toll risk now. Treat it as structural, not episodic, in loan and insurance pricing. A body capable of generating tens of billions annually has strong institutional incentives to survive negotiation rather than fold under diplomatic pressure. Underwriting decisions that assume the toll regime disappears once the ceasefire holds are underwriting a best case, not a base case.

Maritime insurers and logistics operators face a compounding risk. OFAC’s designation of the PGSA means compliance with its permitting and payment process carries its own exposure. Paying the toll is not simply a commercial cost of doing business through the strait; it triggers a separate sanctions-exposure decision. Insurers and operators should price these two risks separately, not net them together.

The governance question — who ultimately controls the Strait of Hormuz — remains open, as H&G argued on July 1. The scale of what is being fought over is no longer in reasonable doubt. Neither is this: the five governments most exposed to the outcome are negotiating for a seat, not occupying one.