In periods of geopolitical tension, markets tend to default to a simple reflex: risk rises, prices fall. It is a clean narrative—almost comforting in its predictability. But the Gulf and its surrounding corridors have once again exposed the limits of that assumption.

Tensions escalated across the Hormuz axis. Risk premiums re-entered the conversation. Headlines intensified. Yet the signal from the energy market diverged from the expected script. Brent crude fell. And that decline did not mean the region became cheaper. It meant the pricing mechanism changed.

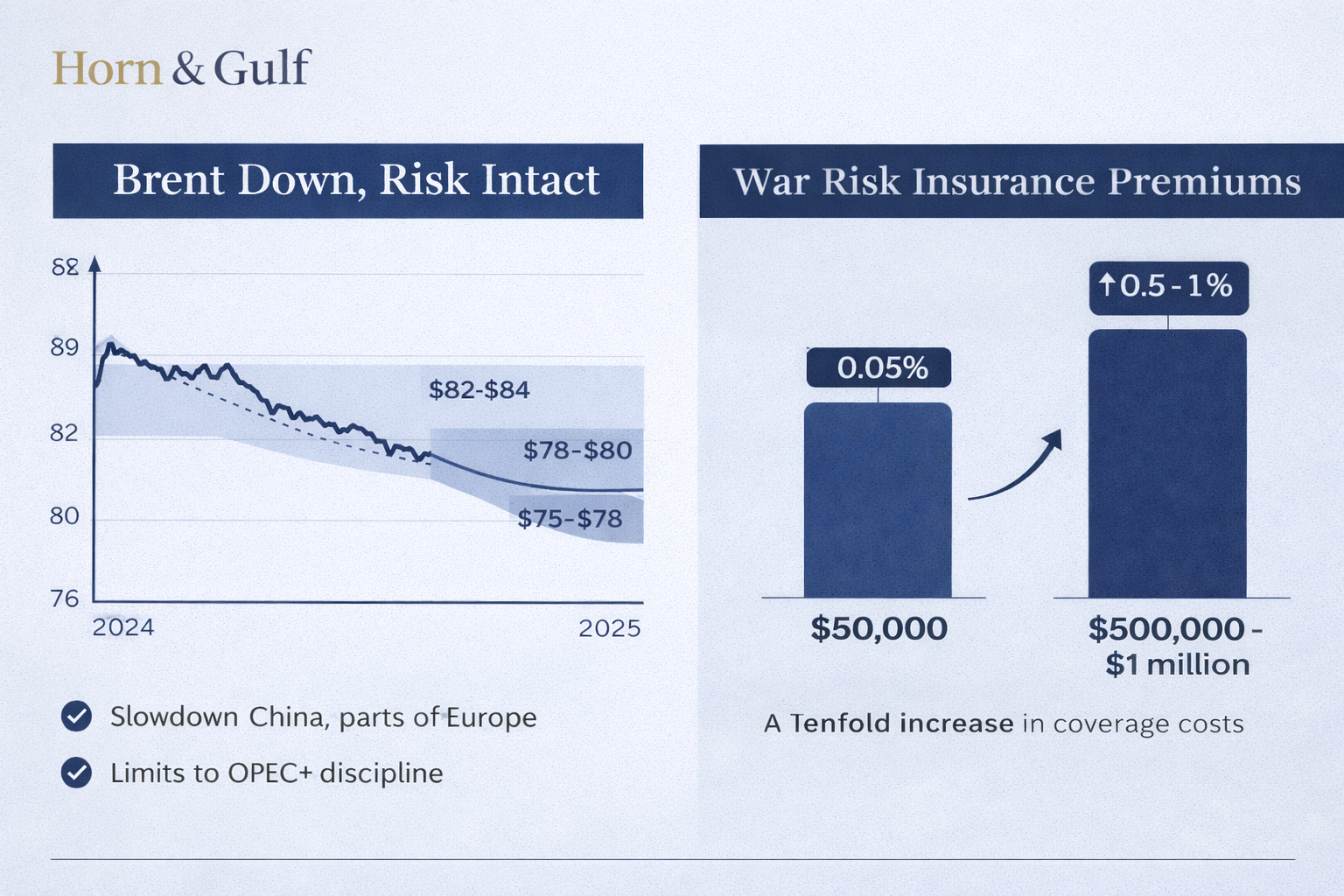

Price Down, Risk Intact

At first glance, the pullback in Brent can be interpreted as easing pressure. But the underlying structure tells a different story.

Throughout 2024, Brent averaged in the $82–84 range. Entering 2025, it softened toward $78–80. During the latest wave of regional tension, instead of spiking, prices drifted lower—settling in the $75–78 band.

This behavior reflects two dominant expectations:

- A slowdown in global demand, particularly from China and parts of Europe

- The limits of OPEC+ discipline in sustaining upward price pressure

In other words, the market is no longer reacting to geopolitical tension in isolation. It is filtering it through demand elasticity. The question is no longer “Is there risk?” It is “Will this risk materially disrupt supply?”

So far, the answer priced into Brent has been: not yet.

The Invisible Cost: Insurance and Transit

While oil prices softened, the cost of moving that oil did not.

War risk premiums surged across key maritime corridors. In insurance markets such as Lloyd’s, coverage for tankers transiting high-risk zones climbed from roughly 0.05% of cargo value to as high as 0.5–1%.

That translates into a tenfold increase in protection costs.

A $100 million cargo that previously required $50,000 in additional insurance now carries a burden of $500,000 to $1 million.

At the same time:

- Some insurers began restricting coverage altogether

- Charter rates for tankers moved upward under risk pressure

- Transit planning became more complex and constrained

So while Brent declined, the logistics layer became significantly more expensive. The market did not remove cost.It relocated it.

Fragmentation: The Return of Regional Pricing

Brent remains a global benchmark—but physical markets are becoming increasingly regionalized. Price spreads between Middle Eastern exports and Atlantic Basin alternatives have widened. For Asian buyers in particular, the effective cost of Gulf-origin barrels has risen once insurance, routing, and risk adjustments are factored in.

This is driving three structural shifts:

- Refiners are diversifying supply portfolios

- Long-term contracts are regaining strategic importance

- Spot market volatility is increasing

The implication is clear: Oil may appear cheaper on paper, but access to that oil is becoming more expensive.

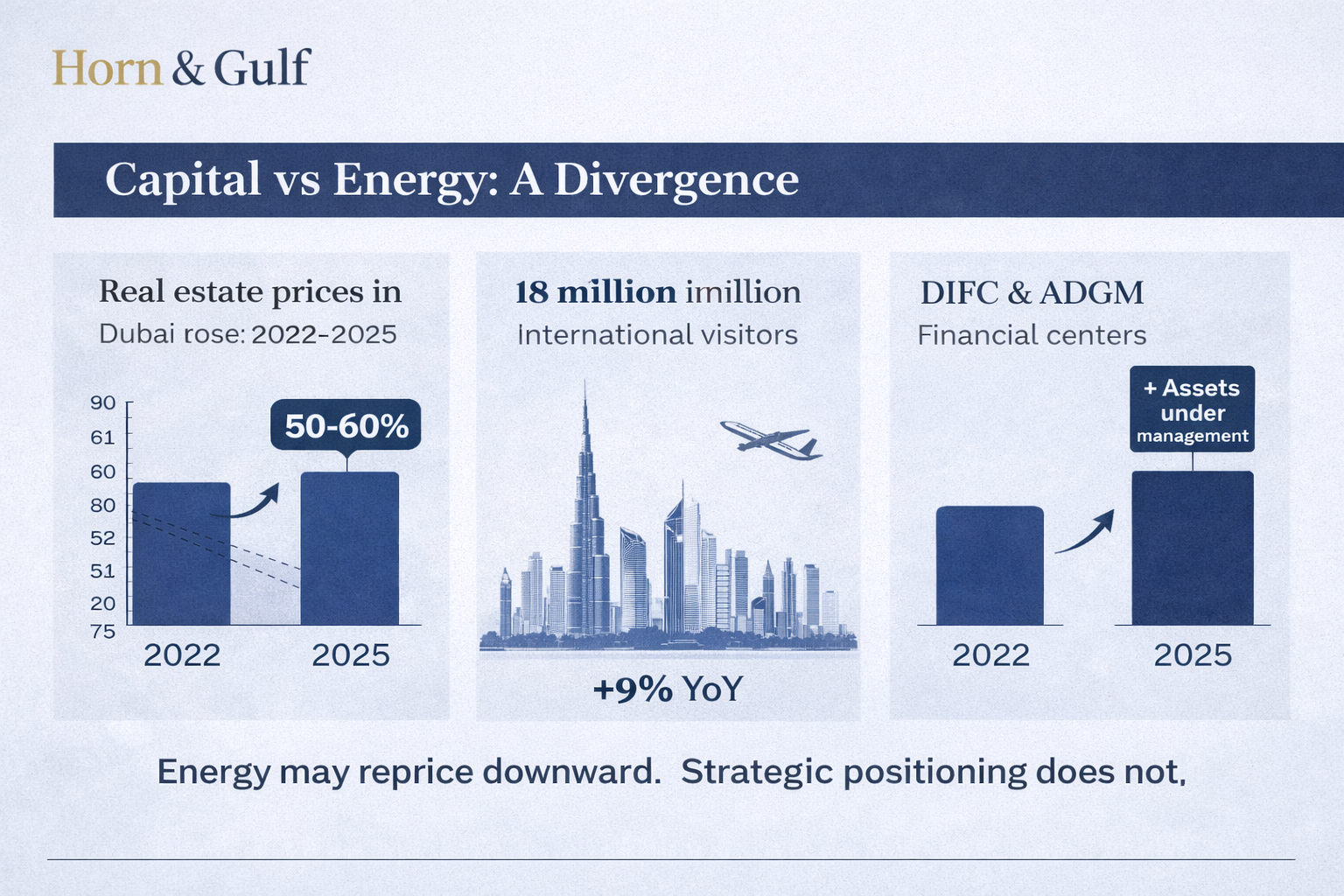

Capital vs Energy: A Divergence

While energy pricing softened, capital flows told a different story.

Across key Gulf hubs:

- Real estate prices in markets like Dubai rose approximately 50–60% between 2022 and 2025

- Dubai recorded around 18 million international visitors in 2024 (+9% year-on-year)

- Financial centers such as DIFC and ADGM continued to expand in both firm count and assets under management

These are not peripheral indicators. They represent capital behavior under stress. Energy may reprice downward.

Strategic positioning does not.

Risk Is Being Priced, Not Avoided

Historically, geopolitical instability triggered capital flight. That model is weakening. In today’s Gulf system, capital is not exiting—it is recalibrating.

Three factors explain this shift:

- Operational continuity across logistics infrastructure (ports, air corridors, trade zones)

- Institutional depth in financial systems (DIFC, ADGM)

- Stronger regulatory frameworks for capital protection

This creates a different equilibrium. Instead of fleeing risk, capital absorbs it—provided the system remains functional. That is a fundamental change in how crisis environments are priced.

The Illusion of Cheapness

The decline in Brent creates a surface-level impression of easing conditions. But that impression does not hold when examined structurally.

Because beneath the headline price:

- Insurance costs are rising

- Transport complexity is increasing

- Supply chains are fragmenting

- Risk-adjusted access is tightening

The system is becoming more expensive—even as the benchmark price declines.

Conclusion: The Price Moved. The Cost Did Not.

This is not a story about oil becoming cheaper. It is a story about where pricing power resides.

Energy markets are no longer defined solely by extraction and demand. They are shaped by logistics, insurance, routing, and geopolitical control. Brent is just one layer of that system.

The region did not get cheaper. The cost simply migrated beyond the chart. And those who read only the price will continue to miss the structure.