The immediate instinct during any geopolitical shock is to look for exits. Ships reroute, insurers reprice, headlines escalate—and the assumption follows: capital will flee next. But capital, especially institutional capital, does not behave like cargo. It does not panic. It recalibrates.

The recent tensions around the Strait of Hormuz did not trigger a capital exodus from the Gulf. What they triggered instead was a repricing mechanism—fast, precise, and selective. And nowhere is this adjustment more visible than in the Dubai International Financial Centre (DIFC), where capital is not escaping risk, but actively redefining it.

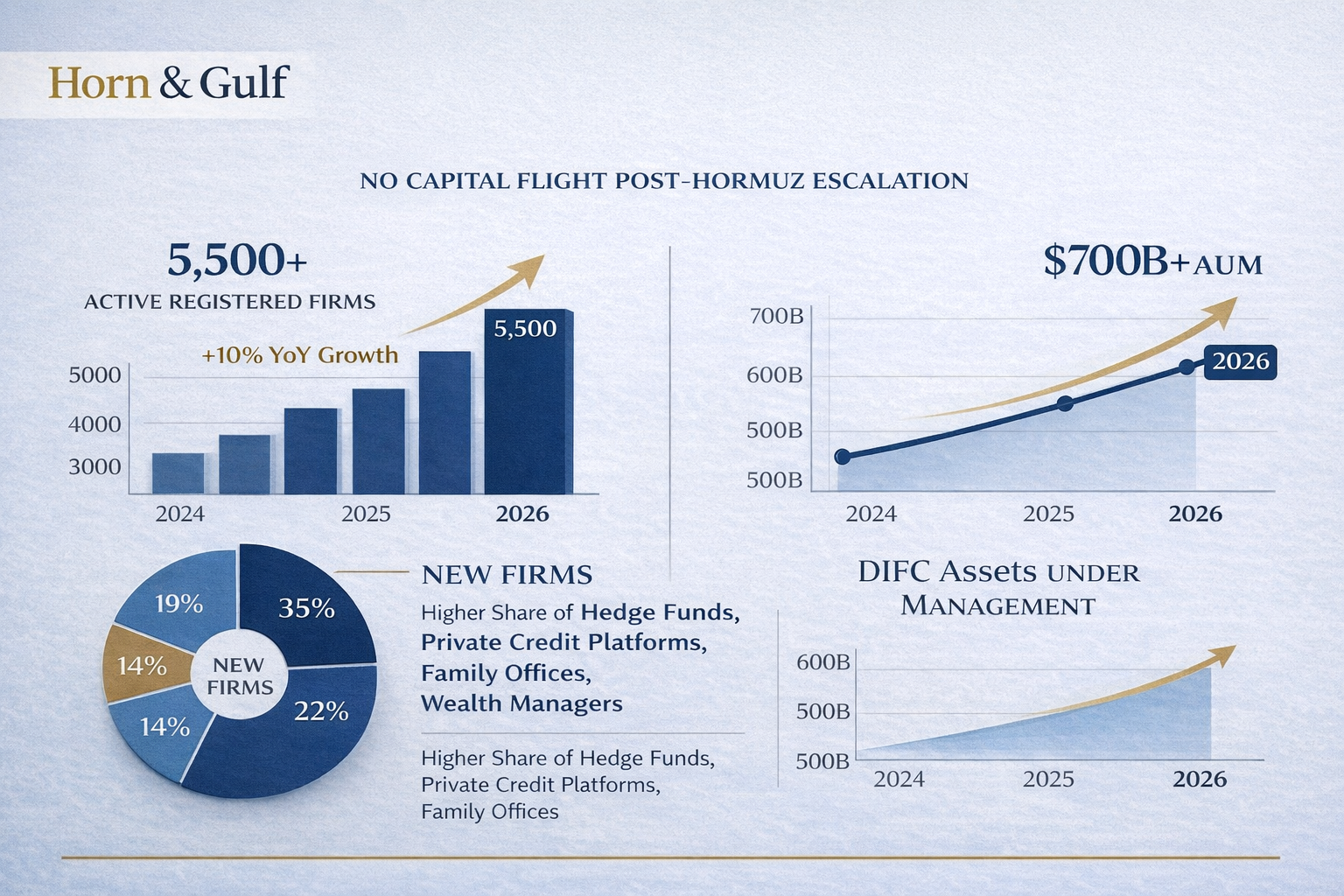

The First Signal: Flows Did Not Reverse

If Hormuz had meaningfully destabilized investor confidence, the first place it would show is in capital flows. That signal never came.

DIFC entered 2026 with over 5,500 active registered firms, marking a double-digit year-on-year increase. More importantly, the composition of these firms shifted. Hedge funds, private credit platforms, family offices, and wealth management entities accounted for a disproportionate share of new entrants.

This matters. Because these are not passive capital pools. These are allocators of risk.

In parallel, assets under management (AUM) within DIFC-linked entities continued to expand, crossing the $700 billion threshold across banks, asset managers, and financial institutions operating within or through the jurisdiction. There was no contraction. No visible withdrawal pattern. Instead, there was reallocation.

Insurance Prices Moved Before Capital Did

The most immediate response to Hormuz tensions came not from capital markets—but from insurance markets.

War risk premiums for vessels transiting the Strait rose sharply within days of escalation. In some cases, coverage costs increased by 30% to 50%, depending on route exposure and cargo type. For energy shipments, the repricing was even more sensitive.

This is not noise. It is the earliest form of capital intelligence. Insurance markets are where risk is quantified before it is debated. And what they signaled was clear: risk has increased, but it is measurable, priceable, and therefore manageable. That distinction is critical. Because once risk becomes priceable, it becomes investable again.

DIFC’s Advantage: Legal Certainty in a Volatile Geography

In moments like these, geography matters less than jurisdiction. DIFC is not just a location. It is a legal architecture.

Operating under an independent common law framework, with its own courts and regulatory regime, DIFC provides something the broader region often struggles to guarantee during periods of tension: continuity. Contracts remain enforceable. Dispute resolution remains predictable. Capital structures remain intact.

And that stability is not theoretical. During previous shocks—the COVID-19 dislocation, the Ukraine war, and successive regional escalations—DIFC did not experience structural disruption. Operational continuity was maintained, and more importantly, confidence in its legal and regulatory framework held.

This is why capital does not leave. Because the system that protects it does not break.

From Safe Haven to Pricing Hub

There is a tendency to label Dubai—and by extension DIFC—as a “safe haven.” It is a comfortable label, but an incomplete one. Safe havens absorb capital during crisis.

DIFC does something more sophisticated: it prices crisis. The growth of hedge funds and private credit platforms in DIFC is not incidental. It reflects a structural shift toward active risk management.

These institutions are not avoiding volatility. They are monetizing it. Energy derivatives, credit spreads, sovereign risk instruments, and structured financing vehicles all become more valuable in environments where uncertainty increases but does not collapse the system.

And that is exactly the environment Hormuz tensions have created. Volatility without systemic breakdown. For capital markets, this is not a threat. It is an opportunity.

The Quiet Expansion of Private Wealth

Another layer of this repricing dynamic is unfolding more quietly: private wealth migration. High-net-worth individuals (HNWIs) and family offices are not reacting to single events. They respond to patterns.

And the pattern they are reading is consistent: Global instability is becoming structural, not episodic.

In response, Dubai—and specifically DIFC—has seen a steady increase in family office registrations and wealth structuring activities. Estimates suggest that over 120 new family offices have been established or relocated to DIFC in the past 24 months alone.

This is long-duration capital. It does not move for headlines. It moves for jurisdictional advantage, tax efficiency, and legal protection. Hormuz did not reverse this trend. If anything, it reinforced it.

Liquidity Did Not Dry Up—It Shifted

One of the most misunderstood aspects of geopolitical stress is its impact on liquidity. The assumption is contraction.

The reality is redistribution. Post-Hormuz tensions, liquidity in certain sectors tightened—particularly in trade finance linked to high-risk corridors. Margins increased. Terms became stricter.

But at the same time, liquidity expanded elsewhere. Private credit funds increased deployment in short-duration, high-yield instruments. Banks adjusted risk models but continued lending, particularly in sectors backed by strong collateral and sovereign alignment.

Even capital markets activity—IPO pipelines, structured financing—did not stall. They recalibrated. Because liquidity, like capital, does not disappear. It moves toward clarity.

The Energy Factor: Risk Anchored to Revenue

Any analysis of Hormuz without energy markets is incomplete. Roughly 20% of global oil flows through the Strait. Any perceived threat to that corridor immediately feeds into price expectations.

But here lies the paradox: Higher geopolitical risk often translates into higher energy prices. And for the Gulf, this is not purely negative.

Increased oil revenues provide fiscal buffers, reinforce sovereign balance sheets, and indirectly support financial systems—banks, credit markets, and investment flows.

DIFC operates within this macro environment. It is not insulated from it. It is leveraged by it. This creates a feedback loop where risk elevates revenue, and revenue stabilizes capital.

A dynamic few regions can replicate.

The Real Premium: System Performance Under Stress

The true value of a financial center is not measured in growth periods. It is measured in stress scenarios. DIFC has now been tested across multiple cycles—pandemic disruption, global monetary tightening, regional conflicts, and now renewed Hormuz tensions.

Each time, the outcome has been consistent: No systemic failure. No capital flight. No legal breakdown. Instead, there has been expansion, adaptation, and repricing.

This is not resilience by chance. It is resilience by design.