Dubai’s rental market is often read as a secondary indicator — a downstream effect of capital inflows.

This is no longer accurate.

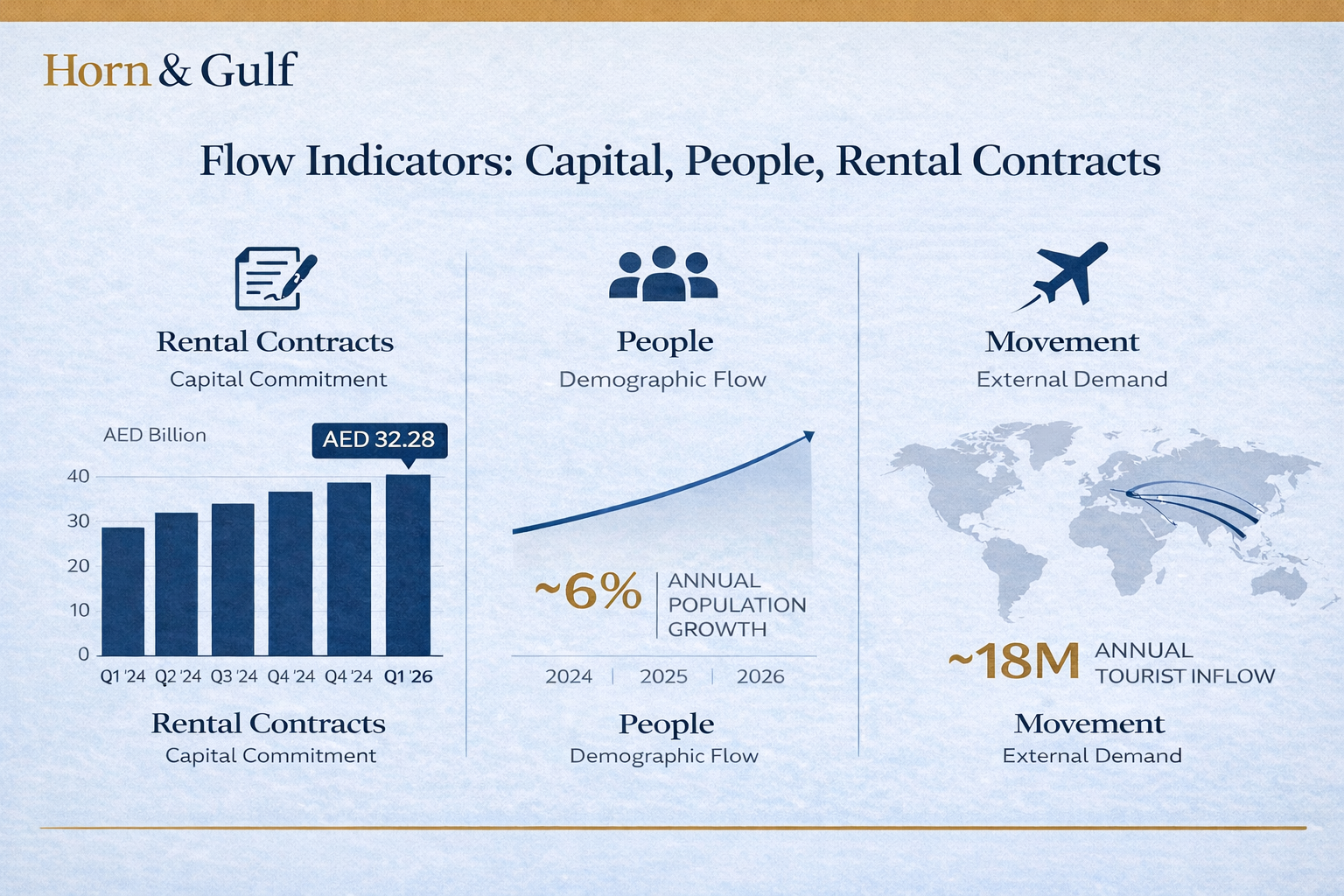

The AED 32.2 billion in rental contracts recorded in Q1 2026 is not simply a measure of activity. It is a signal of system continuity.

In periods of regional tension, the first stress point is not asset prices — it is human positioning. Where people choose to live, sign contracts, and commit liquidity.

If risk had materially altered sentiment, rental activity would have shown early signs of contraction:

fewer new contracts, delayed commitments, increased short-term flexibility. Instead, the system held.

This suggests a structural shift: Dubai is no longer behaving as a passive recipient of capital seeking safety.

It is functioning as an operational platform where capital, talent, and residency align.

The distinction matters. Because in this model, resilience is not defined by the absence of volatility —

but by the system’s ability to absorb it without interruption. Rental flows, in this context, are not lagging indicators.

They are confirmation that the system remains live.

Flow Indicators: Capital, People, Contracts

Understanding Dubai’s performance in early 2026 requires looking beyond prices. The real signal lies in how the system manages its flows. Three core indicators clarify this picture:

Contracts (Capital Commitment):

AED 32.2 billion in rental contracts in Q1 2026

People (Demographic Flow):

~6% annual population growth

Movement (External Demand):

~18 million annual tourist inflow

Taken together, these are not isolated metrics. They form a unified pattern:

Dubai is not functioning as a traditional asset market —but as a system of continuous flows.

Beyond Volume: What the Market Structure Reveals

The Q1 2026 data does more than confirm activity — it reveals structure.

With 118,385 new rental contracts and 135,607 renewals, the market is not only expanding but also retaining. At the same time, a 25% decline in canceled contracts points to increasing stability, where commitments are less likely to reverse once made.

This is further supported by the operational layer: over 10,200 real estate offices and 3,599 active licenses — including 1,564 in sales and brokerage — indicating a dense and functioning intermediary network that keeps transactions fluid.

Taken together, these are not isolated statistics. They point to a system where entry, retention, and execution are all active — a market not defined by spikes in demand, but by the consistency of its underlying structure.