The Strait did not collapse. It did something more complex—and more consequential. It shifted from a sudden shock into a prolonged state of friction.

In the first phase of the crisis, the signal was clear: flows stopped, production shut in, and risk repriced instantly. But over the last 72 hours, a different pattern has emerged. Tankers are moving again—selectively. LNG cargoes are approaching Hormuz—cautiously. Production is not restarting at scale, but systems are probing their limits.

This is no longer a story about closure versus reopening. It is about how quickly a fractured system can re-synchronize across production, insurance, shipping, and geopolitics.

Production Halt Was Immediate. Restart Is Not.

When the shock hit, Gulf producers reacted with speed and discipline. Output was curtailed, facilities were shut in, and inventories began accumulating across the region. But restarting is not the reverse of stopping.

The current bottleneck is not capacity—it is coordination. Oil and gas cannot flow unless multiple layers align simultaneously: upstream production, terminal readiness, tanker availability, insurance coverage, and maritime security guarantees. A single weak link delays the entire chain.

As a result, the Gulf is now dealing with a structural lag. Production was halted in days. Restart will take weeks—if not months.

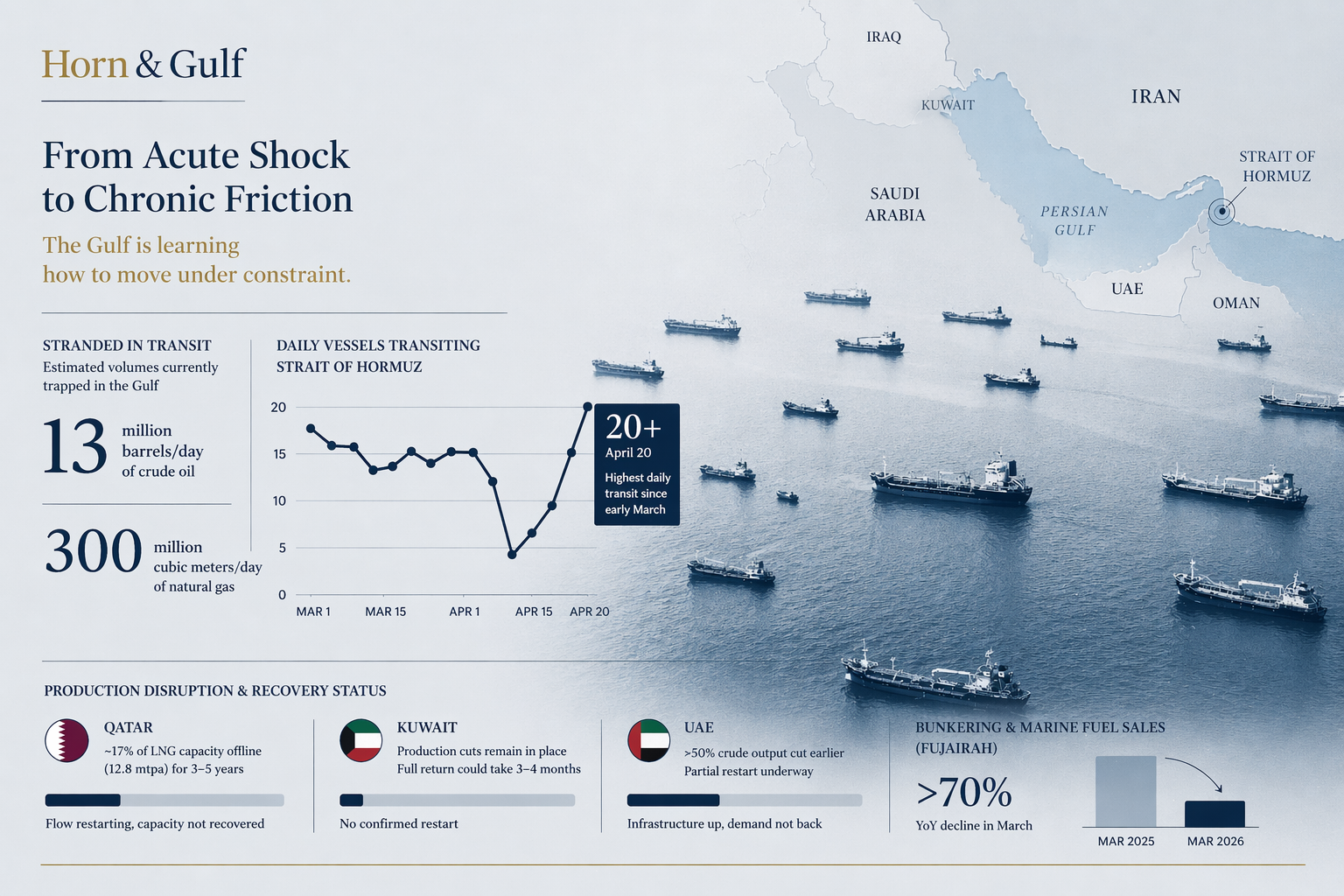

Qatar, Kuwait, UAE: Three Different Recovery Speeds

The most telling signal of this transition comes from how the three key Gulf producers are moving—each at a different speed, each constrained by a different bottleneck.

Qatar:

The clearest signs of recovery are emerging here. On April 18, according to Reuters data, five LNG vessels loaded at Ras Laffan approached the Strait of Hormuz—potentially the first significant physical attempt to resume LNG exports since the conflict began. Kpler data also detected flaring activity indicating that some trains in the North Field at Ras Laffan and the Das Island LNG facility in the UAE are restarting operations.

However, the structural constraint remains severe. Earlier Reuters reporting indicates that Iranian strikes knocked out approximately 17% of Qatar’s LNG capacity, with around 12.8 mtpa potentially offline for 3–5 years. The implication is clear: flows are resuming, but capacity has not recovered. Qatar is testing the system—not restoring it.

Kuwait:

In contrast, Kuwait offers no clear signal of normalization. There has been no confirmation of a full production restart in the past 72 hours. The most reliable reference point remains the early March force majeure declaration by Kuwait Petroleum Corporation, which framed the cuts as precautionary and reversible under stable conditions.

Recent recovery analyses do not indicate a rapid turnaround. Instead, they reinforce a consistent constraint: insurance and logistics remain binding limitations.

The most realistic assessment is that production cuts persist and the recovery timeline remains uncertain. Previous guidance from Kuwait Oil Company leadership suggested that even under stable conditions, a full ramp-up could take 3–4 months. Kuwait is not testing the system yet. It is waiting for it to stabilize.

United Arab Emirates:

The UAE sits somewhere in between—showing early movement, but not full recovery. ADNOC had previously cut production by more than half, implementing both onshore and offshore shut-ins.

Recent vessel tracking data indicates that two ballast ADNOC tankers have re-entered the Gulf of Oman, while flaring activity suggests partial reactivation at Das Island LNG facilities. These are early signals of operational restart.

However, downstream indicators tell a different story. Fujairah’s bunkering and marine fuel markets remain severely depressed, with March sales down more than 70% month-on-month and year-on-year.

The conclusion is nuanced: terminal and LNG operations are showing signs of life, but the broader maritime ecosystem—fueling, shipping confidence, and trade volume—has not recovered. The UAE is restarting infrastructure. The market has not followed yet.

Inventories Are Trapped Between Production and Trust

Across the Gulf, millions of barrels remain effectively stranded—not because they cannot be produced, but because they cannot be moved safely and predictably. This is the defining feature of the current phase.

Even where production can resume, cargoes cannot move without insured tankers, secure transit corridors, and confidence that vessels will not be targeted mid-passage. Each of these elements operates on its own timeline—and none respond instantly to political announcements. The result is a growing disconnect between available supply and deliverable supply.

This gap is where friction lives.

Normalization Is No Longer a Political Event

The past 72 hours have shown that reopening the Strait is not a binary decision. It is a layered process. A statement can open Hormuz in minutes. A system takes weeks to trust that opening.

Five LNG vessels approaching the Strait do not signal normalization. They signal experimentation. Ballast tankers repositioning do not signal recovery. They signal preparation. What matters now is not whether flows have resumed—but whether they can continue without interruption.

Conclusion: A System Learning to Move Again

The Gulf is no longer in shock. It is learning how to move under constraint.

Qatar is probing export routes with partial capacity.

The UAE is reactivating infrastructure without full demand recovery.

Kuwait remains on hold, constrained by systemic risk rather than physical limits.

This is what chronic friction looks like: not collapse, not recovery—but a slow, uneven reactivation shaped by uncertainty. And in this phase, the key variable is no longer production capacity.

It is trust.