The headlines were immediate and predictable. “Petrodollar under threat.” “Gulf turning to yuan.” “A structural shift in global energy markets.” But none of these readings capture what is actually happening.

The recent signal from the United Arab Emirates—that it may resort to alternative currencies like the Chinese yuan if access to US dollars tightens—is not a declaration of intent. It is a stress response. A controlled system, under pressure, is mapping its failure scenarios. This is not about abandoning the dollar. It is about testing the consequences of its absence.

A System Built on Flow, Not Ideology

For decades, the Gulf’s financial architecture has been anchored in a simple chain: Energy exports → Dollar inflows → Currency stability → System confidence

In the case of the UAE, the dirham’s peg to the US dollar has held firm not because of policy declarations, but because of consistent dollar liquidity. Oil and gas revenues—directly or indirectly—feed that liquidity. Trade, finance, and investment cycles reinforce it.

This is not a political system. It is a flow system. As long as dollars arrive, the system holds. If they slow, the system adjusts. If they stop, the system is tested.

The Disruption: When Flows Are Interrupted

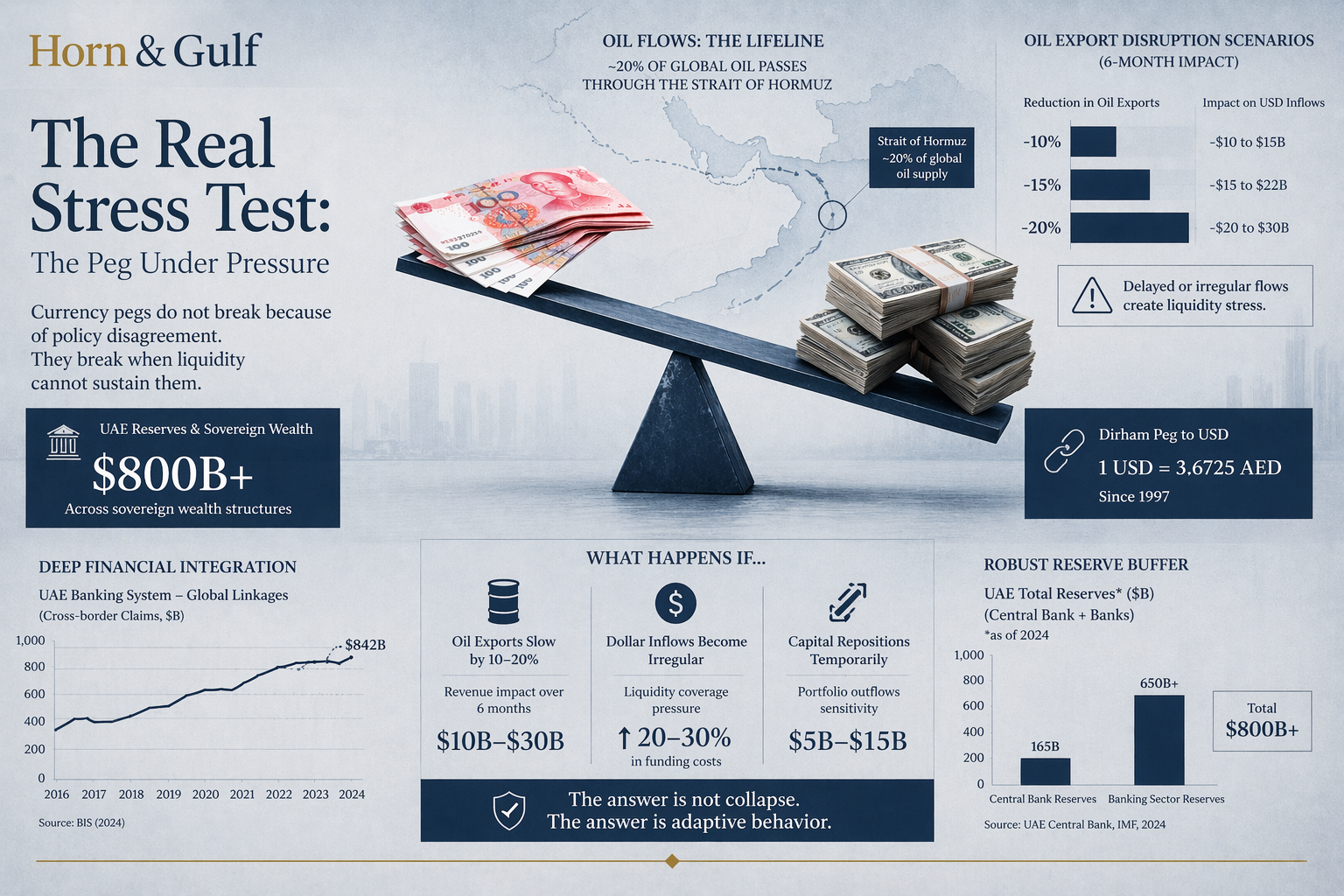

The current tension is not theoretical. It is logistical. The Strait of Hormuz—through which roughly 20% of global oil supply passes—has become a point of friction. Even partial disruptions have immediate downstream effects:

- Tanker traffic slows or reroutes

- Insurance premiums spike

- Delivery timelines extend

- Payment cycles delay

The result is not just an energy shock. It is a liquidity disturbance. If oil shipments are delayed, dollar receipts are delayed. If dollar receipts are delayed, balance sheets tighten. If balance sheets tighten, currency systems feel pressure.

This is the chain reaction now being quietly modeled.

The Signal: A Contingency, Not a Pivot

Within this context, the UAE’s message becomes clearer. It is not saying: “We will price oil in yuan.” It is saying:

“If dollar liquidity becomes unreliable, we have alternatives.” That distinction matters. This is not a currency shift. It is a liquidity hedge.

The mention of the Chinese yuan is not ideological alignment with China. It reflects a practical reality: China is the largest buyer of Gulf energy, and it has spent the past decade building bilateral currency channels, swap lines, and settlement infrastructure.

In a disruption scenario, these channels become usable—not preferable, but available.

The Real Stress Test: The Peg Under Pressure

At the center of this system sits the dirham’s peg to the US dollar. Currency pegs do not break because of policy disagreement. They break when liquidity cannot sustain them.

The UAE holds substantial reserves—well above $800 billion across sovereign wealth structures—and its banking system remains deeply integrated with global markets. There is no immediate threat to the peg.

But this is not about current stability. It is about scenario mapping.

What happens if:

- Oil exports slow by 10–20% for several months?

- Dollar inflows become irregular?

- Capital begins to reposition temporarily?

The answer is not collapse. The answer is adaptive behavior. Alternative currencies, short-term liquidity arrangements, and bilateral settlements are all part of that adaptation toolkit.

Beyond the Headlines: What This Is Not

It is important to define what this moment does not represent.

- It is not the end of the petrodollar system

- It is not a geopolitical realignment away from the United States

- It is not a structural shift in oil pricing mechanisms

The dollar remains dominant because of:

- Deep, liquid capital markets

- Global trade settlement infrastructure

- Institutional trust and scale

No alternative currently matches this combination. What is changing is not dominance. It is dependency awareness.

A Subtle but Important Shift

For decades, the system operated on an implicit assumption: Dollar liquidity would always be available when needed. That assumption is now being tested—not because the system is collapsing, but because the environment has changed.

Geopolitical tensions, supply chain disruptions, and regional conflicts have introduced a new variable: intermittency. The Gulf is responding accordingly. It is not redesigning the system. It is reinforcing it—by understanding its limits.

Conclusion: Testing the System, Not Replacing It

The Gulf is not walking away from the dollar. It is doing something more precise—and more important. It is identifying what happens when the system is stressed, when flows are interrupted, and when assumptions are challenged.

The question is not: “Will the dollar be replaced?” The real question is: “What happens to a dollar-based system when the dollar itself becomes intermittent?” That is the scenario now being explored.

And in that exploration, the Gulf is not signaling a break. It is demonstrating control.