Dubai real estate risk is increasingly being assessed through credit markets rather than property prices alone. Recent bond-market movements suggest investors are paying closer attention to developer cash flows, installment collections and the market’s ability to absorb a large future supply pipeline. While concerns about prices remain, the deeper question is whether demand can keep pace with what is scheduled to be delivered over the coming years.

Dubai’s property market is used to being questioned at moments of stress.

It was questioned after 2008. It was questioned again during the long correction between 2016 and 2020. Each time, the emirate eventually recovered through a familiar combination of capital inflows, population growth, regulatory confidence and its role as a safe, connected hub in a fragmented region.

The current test is different enough to deserve attention, but not yet severe enough to justify dramatic language.

A recent JPMorgan note points to a weaker market environment following the regional conflict. Transaction activity has reportedly fallen sharply, international buyers have become more cautious, rents have softened, and a large delivery pipeline is expected between 2026 and 2030. The headline figure — roughly 400,000 units — is the number that matters most.

Supply alone does not create a crisis. Dubai has often absorbed more demand than outside observers expected. Projects can also be delayed, phased or repriced before they fully reach the market. But the size of the pipeline changes the question investors need to ask.

The issue is no longer only whether prices fall.

It is whether future demand can absorb the next wave of supply without putting pressure on developer cash flows.

The Bond Market Is Asking a Different Question

Property buyers usually look at sale prices, rental yields and transaction volumes. Bond investors look elsewhere.

They ask whether developers can keep collecting cash, manage obligations and refinance debt if new sales slow.

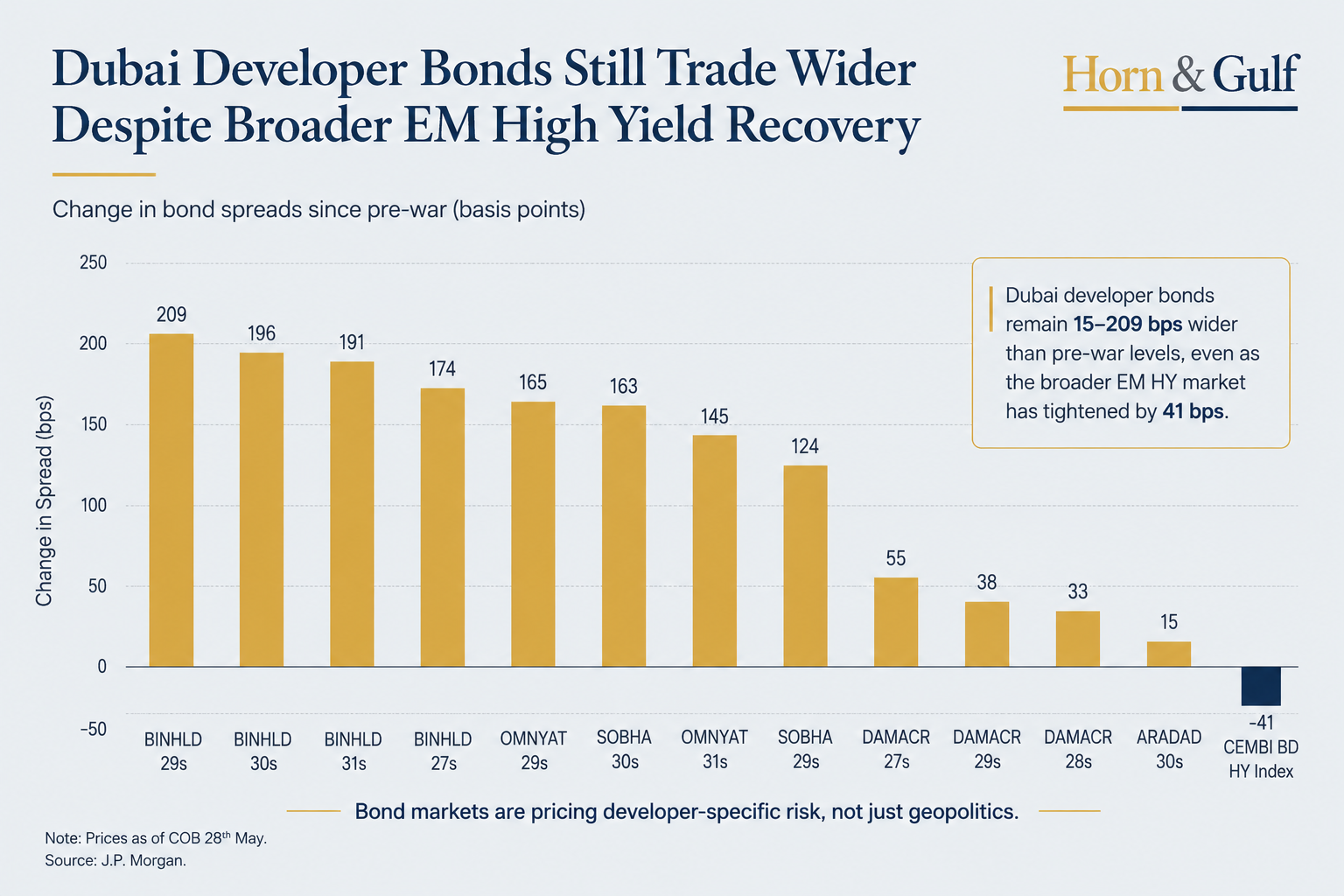

That is why JPMorgan’s credit data is useful. Several Dubai developer bonds remain wider than their pre-war levels even though broader emerging-market high-yield debt has largely recovered. JPMorgan’s CEMBI high-yield benchmark has tightened compared with pre-war levels, while Dubai developer names have not fully followed.

That gap is the signal.

It does not mean the market is pricing collapse. It means investors are demanding more compensation for uncertainty around sales momentum, collections and inventory absorption.

In other words, the credit market is not simply reacting to geopolitics. It is beginning to separate regional risk from Dubai real estate risk.

Not All Developers Are Being Treated Alike

The spread movements also show discrimination rather than panic.

Binghatti bonds have widened more aggressively in JPMorgan’s sample. Sobha has also widened, but with a different risk profile. DAMAC’s deterioration appears more contained.

The market is not saying every developer faces the same pressure.

For credit investors, the important distinction is not last year’s profitability. It is visibility of future cash flows. A developer with a strong pipeline of already-sold units and reliable installment collections is in a different position from one more dependent on new sales to preserve liquidity.

This is why the bond market often sees stress before the property market admits it.

A project can still look active. Sales offices can still operate. Reported earnings can still appear strong. But if collections slow, discounts rise or unsold inventory becomes harder to move, credit investors usually notice before headline property data fully reflects the change.

The Accounting Lag

There is another reason caution is necessary.

Developer financial statements may continue to look healthy even if the market is softening underneath.

Much of the revenue reported by developers can reflect projects sold earlier and recognized gradually under percentage-of-completion accounting. That means current earnings may still be carrying the strength of a previous sales environment.

This does not make the numbers misleading. It simply means they are backward-looking.

For the next phase of the cycle, two questions matter more than headline profit:

Are buyers still paying installments on time?

And at what price is unsold inventory actually clearing?

Those answers will say more about market health than a strong income statement built on earlier sales.

Supply Is Visible. Demand Is Harder To Measure.

The supply side of the argument is easy to understand. A large number of units is expected to reach the market over the next several years. If demand weakens at the same time, prices and rents may come under pressure.

The demand side is more complicated.

Dubai is not the same market it was in 2009, or even in 2017. Over the past five years, it has attracted a broader mix of international capital: family offices, entrepreneurs, wealth migration flows, regional corporate relocations, technology investors and high-net-worth buyers seeking regulatory stability.

These demand sources do not eliminate cyclicality. They do, however, make simple historical comparisons less reliable.

A market that looks oversupplied on paper may absorb more than expected if capital inflows remain strong. The opposite is also true. A large pipeline becomes much more dangerous if international buyers step back for longer than expected.

That is the tension now sitting beneath Dubai real estate.

Repricing, Not Distress

The evidence so far supports a repricing story more than a distress story.

Developer bonds are under pressure, but not at levels normally associated with a severe solvency crisis. Construction continues. Payments continue. Capital has not disappeared.

The market is pricing slower growth, weaker visibility and greater differentiation between developers.

That is still important.

Dubai’s property cycle may be moving from a phase where liquidity lifted most developers together into one where balance-sheet structure, collection quality and inventory discipline matter more. In a rising market, these differences are often ignored. In a slower market, they become visible quickly.

Indicators to Watch

The next phase will be clearer in operating data than in public sentiment. The most important indicators are:

- installment collection performance across major developers

- discounting or repricing of unsold inventory

- actual project completions versus announced delivery schedules

- residential rental growth and vacancy trends

- international buyer participation in new transactions

- developer bond spreads relative to broader emerging-market high yield

If collections remain steady and international capital returns, the current spread widening may prove temporary. If collections weaken while deliveries accelerate, the market could enter a more difficult adjustment phase.

What Remains Unclear

Several parts of the picture remain difficult to verify in real time.

Transaction declines and rental weakness are reported by market participants, but the depth and duration of the slowdown are still uncertain. Delivery pipelines may shift. Developers may delay, rephase or adjust launches. Geopolitical conditions may improve or worsen. Dubai’s ability to attract capital during periods of regional uncertainty has also surprised analysts before.

That resilience should not be dismissed.

Nor should the supply risk.

The more disciplined reading is that Dubai is not yet facing a systemic property crisis. But the market is no longer being priced as if momentum alone can solve every problem.

Credit investors have started to ask harder questions.

For now, they are not pricing a collapse. They are pricing the possibility that the next stage of Dubai’s real estate cycle will be more selective, more cash-flow sensitive and less forgiving than the last.