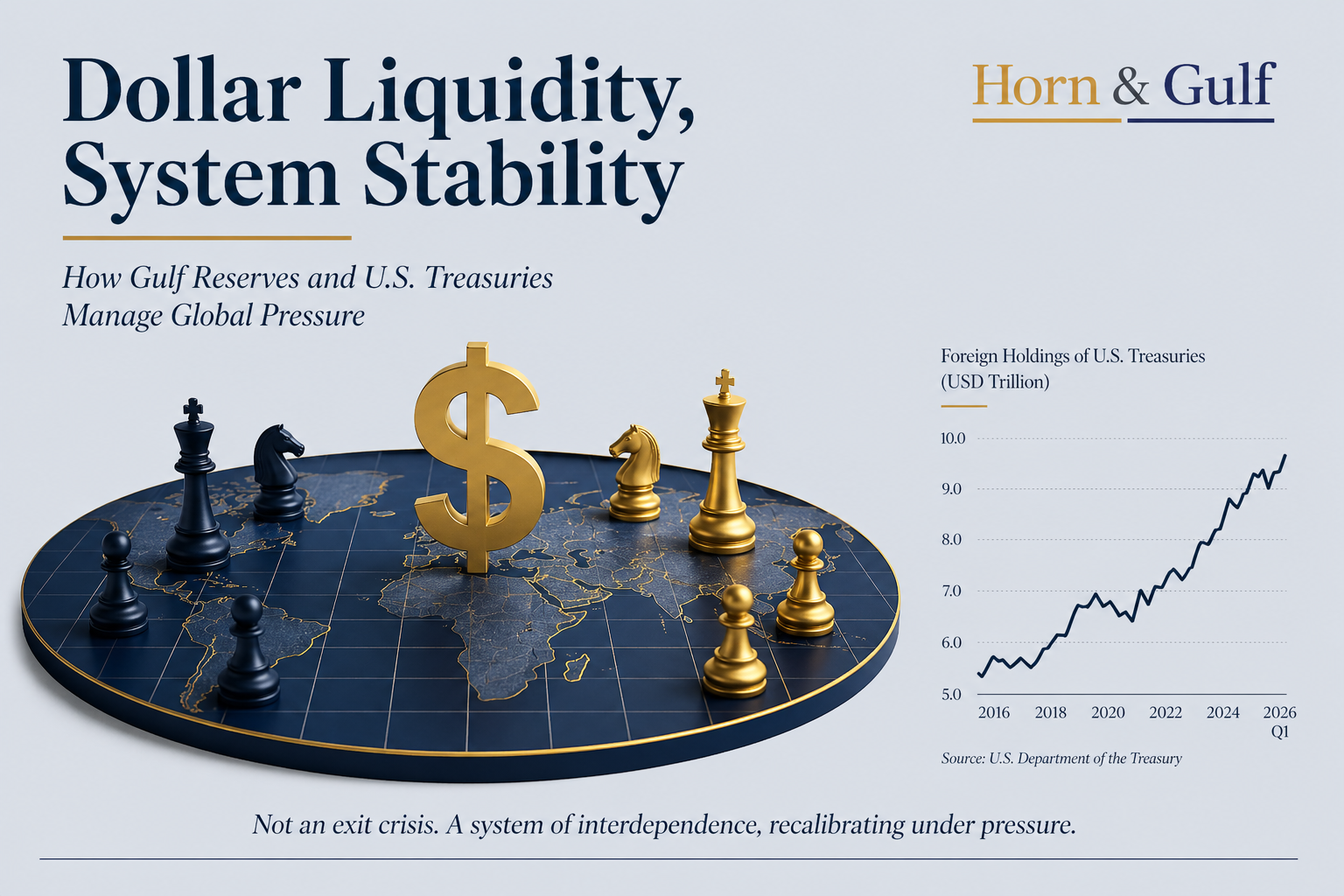

US Treasury foreign holdings and dollar liquidity are becoming central to global financial stability. What appears as a liquidity issue is in fact a structural shift in how capital, energy and risk interact across the Gulf system.

A Debate That Misreads the Same Signal in Two Different Ways

A recent debate has framed the issue in starkly different terms.

One view argues that Federal Reserve swap lines are a quiet admission of stress — that certain large holders of U.S. Treasuries are, in practice, constrained. That if conditions deteriorate, the “exit door” may narrow. In this framing, the real battlefield is the yield curve.

The opposing view rejects this entirely. Swap lines, it argues, are not about restricting sales but about providing dollar liquidity. Gulf economies facing volatile oil revenues and capital outflows need access to dollars. The United States, in turn, has no interest in forcing these actors to sell Treasuries into the market and destabilize yields.

Both interpretations are reacting to the same signal. But they are describing different systems.

What the Literature Actually Says About Swap Lines and Treasury Demand

In global financial literature, this is not a new debate. It appears under more technical language:

- Dollar liquidity backstops: Swap lines are crisis tools designed to prevent forced selling by ensuring access to USD funding. This was visible in 2008, 2020 and again during regional banking stress episodes.

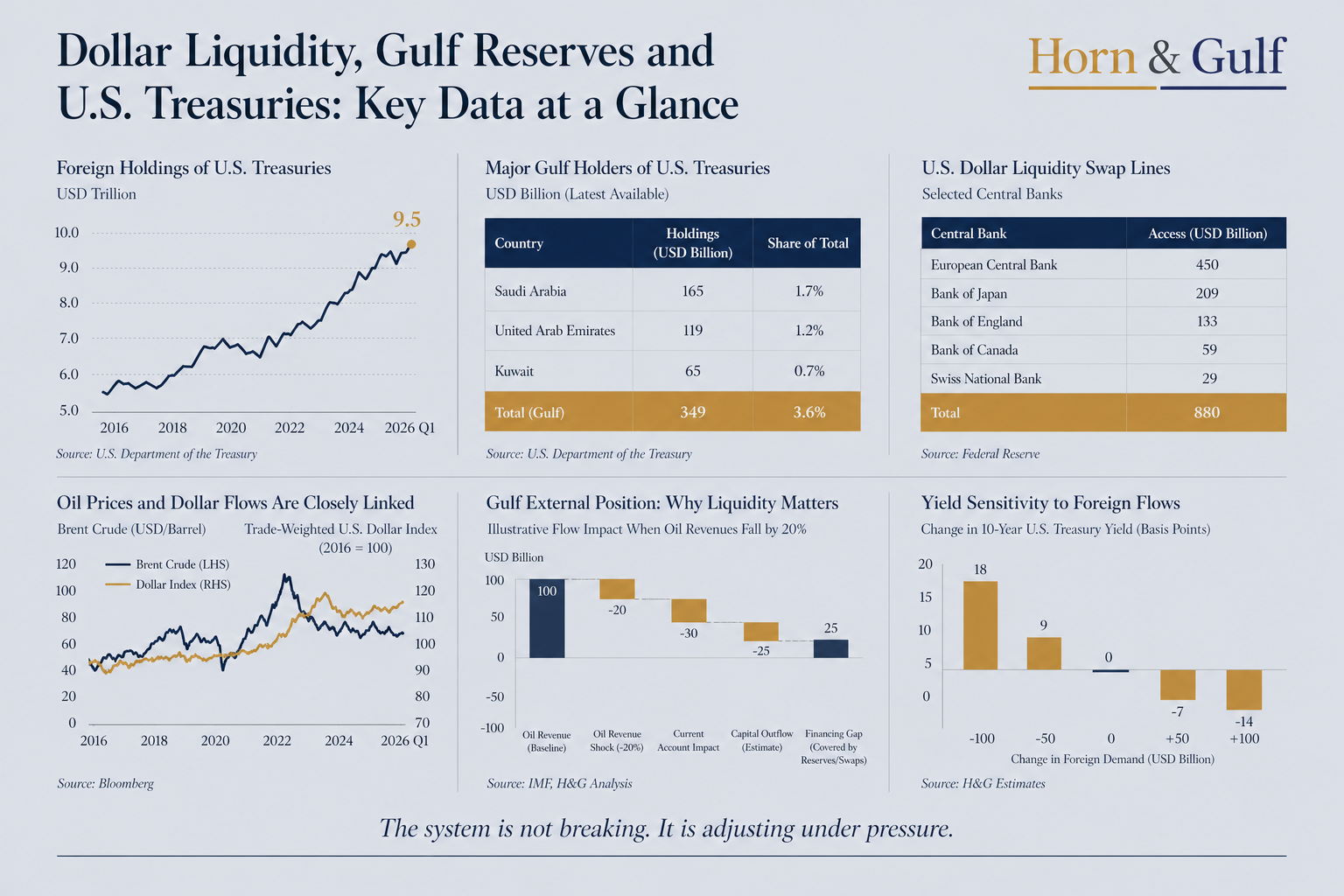

- Foreign demand and yield stability: U.S. Treasury markets rely on consistent foreign participation. Sudden shifts in demand do not need to be large to affect yields. Marginal flows matter.

- Interdependence, not control: Treasuries function both as a safe asset and as a structural dependency. Large holders are not simply investors; they are embedded within a system that ties reserves, trade and currency stability together.

The consensus is relatively clear: Swap lines are not mechanisms of restriction. They are mechanisms of stabilization.

The Misinterpretation: From Constraint to Intent

Where the first argument overreaches is in interpreting stabilization tools as evidence of hidden constraints. There is little evidence of formal or informal “caps” preventing sovereign holders from selling Treasuries. More importantly, such a constraint would be structurally difficult to enforce across multiple jurisdictions and actors.

The more relevant dynamic is not inability to sell, but lack of incentive to sell.

For Gulf economies in particular, Treasuries are not just portfolio assets. They are reserve instruments linked to currency stability, trade settlement and fiscal management. A large-scale liquidation would not only affect U.S. markets — it would feed back directly into their own financial systems.

This is not a locked door. It is a door that is rarely worth opening.

The Structural Layer: Energy, Dollars and Sovereign Balance Sheets

To understand the system, one has to move beyond the bond market. There is a deeper loop at work:

- Energy exports generate dollar inflows

- Dollar inflows accumulate as reserves

- Reserves are partially held in U.S. Treasuries

This loop has been stable for decades. But it is not static. When oil revenues fluctuate or capital outflows increase, Gulf states may draw down reserves or seek alternative sources of dollar liquidity. This is where swap lines enter the picture — not as a constraint, but as a bridge.

At the same time, the United States has its own incentive structure.

A disorderly sell-off in Treasuries would push yields higher, tighten financial conditions and transmit stress into the broader economy. The result is a system of mutual management rather than unilateral control.

Where the Pressure Actually Sits

The system is not breaking. But it is under pressure. That pressure appears in more subtle ways:

- Slower accumulation of Treasuries

- Shifts toward shorter-duration holdings

- Increased reliance on liquidity facilities

- Greater sensitivity of yields to marginal flows

These are not signs of exit. They are signs of recalibration. Markets do not require mass selling to reprice risk.

They require uncertainty around future flows.

The Geopolitical Overlay: Iran and the Price of Friction

The geopolitical layer complicates the picture further. Iran’s strategic objective is not to trigger a financial collapse. It is to increase friction across interconnected systems:

- Higher oil prices

- Elevated shipping risk

- Persistent uncertainty

These effects feed indirectly into financial markets. Higher energy prices affect dollar flows. Elevated risk premiums influence capital allocation. Over time, this shapes demand for U.S. assets at the margin. The mechanism is indirect, but the impact is real.

What This Is — And What It Is Not

This is not a crisis of forced liquidation. It is not a scenario where sovereign holders are suddenly unable to access their positions. It is something more complex and more familiar: A system adjusting under sustained, low-intensity stress.

The key dynamic is not exit. It is flow management.

A System That Rebalances, Not One That Breaks

The U.S. Treasury market remains the core collateral layer of the global financial system. That position is not easily displaced. But its stability increasingly depends on active management:

- By central banks providing liquidity

- By sovereign holders adjusting portfolios without triggering disruption

- By markets continuously repricing risk

This is not a moment of rupture. It is a period of controlled pressure. And in such systems, stability is not the absence of stress. It is the ability to absorb it without breaking.