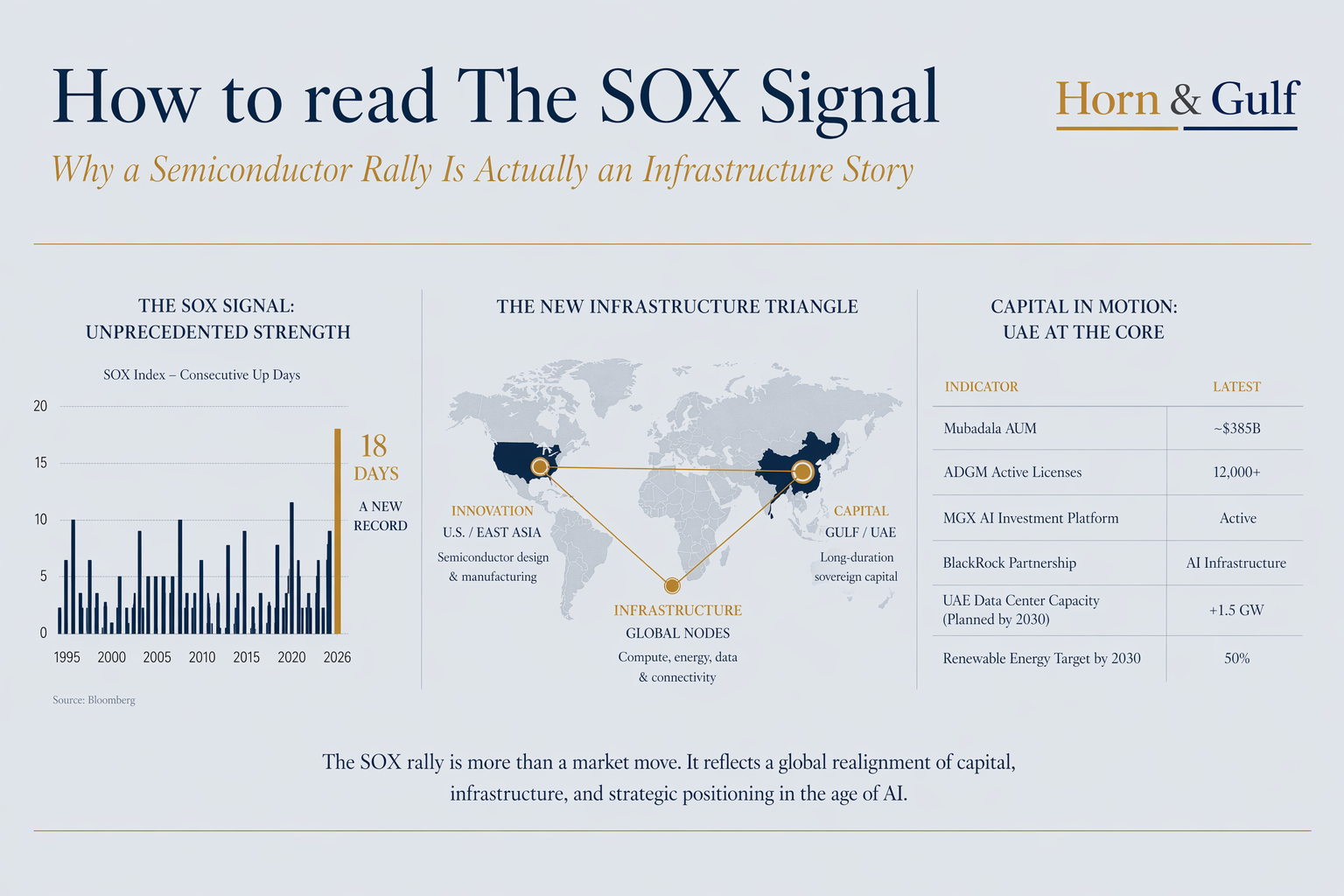

For 18 consecutive sessions, the PHLX Semiconductor Sector Index (SOX) has moved higher. On the surface, this looks like a sector rally. It is not. What we are observing is not a price movement. It is a signal — one that points beyond equities, into the structure of the next global infrastructure cycle.

The re-rating of companies such as NVIDIA, TSMC and Advanced Micro Devices is often explained through earnings growth, product cycles or demand visibility. While these factors are relevant, they are insufficient to explain the persistence and intensity of the current move. These companies are not merely being repriced as businesses. They are being repriced as entry points into a much larger system transition.

That transition is frequently described in abstract terms — artificial intelligence, digital transformation, automation. Yet these labels can obscure more than they clarify. AI does not scale in abstraction. It scales physically. It requires compute capacity, and compute capacity, in turn, requires infrastructure. What appears as a technological shift is, at its core, an infrastructural build-out.

Once framed this way, the analytical lens changes. The focus moves away from products and toward systems. From innovation toward deployment. From software narratives toward physical constraints. The expansion of AI is not simply a question of model development or algorithmic capability. It is a question of energy availability, land use, cooling systems, regulatory clarity and, ultimately, capital allocation at scale.

From Price Action to System Signal

Markets often compress complex transitions into simple indicators In this case, the signal is unusually clear:

- sustained capital inflow

- concentrated sector exposure

- absence of meaningful pullbacks

This is not typical momentum. It reflects conviction. But conviction in what?

Not in semiconductors as a sector — but in AI as an infrastructure layer.

Layer 1: Silicon Is the Entry Point, Not the End State

The companies driving this move — NVIDIA, TSMC, Advanced Micro Devices — are not being repriced simply because of earnings. They are being repriced because they sit at the front edge of a larger build-out cycle. That cycle is not about chips. It is about compute capacity.

And compute capacity is not a product. It is infrastructure.

Layer 2: Infrastructure Requires Energy, Capital and Jurisdiction

AI systems do not scale in abstraction. They scale physically.

Which means:

- energy supply becomes a constraint

- land and cooling become variables

- regulatory clarity becomes a requirement

- capital intensity becomes unavoidable

This shifts the conversation from technology to deployment environments. And this is where geography re-enters the system.

Layer 3: The Re-Emergence of Strategic Locations

Not all regions can host this next layer. The requirements are specific:

- surplus or scalable energy

- stable governance

- capital availability

- global connectivity

A limited number of nodes meet these conditions. Among them, the Gulf — and specifically Abu Dhabi and Dubai —

is increasingly positioning itself as a viable host.

This is the point at which geography re-enters the equation. Infrastructure does not exist in a vacuum. It is anchored in specific locations, shaped by political stability, economic policy and resource availability. Not every region is equally positioned to host the next generation of compute infrastructure. The requirements are too stringent, the capital intensity too high and the operational risks too complex.

Within this emerging landscape, the Gulf — and in particular Abu Dhabi and Dubai — has begun to assume a more defined role. This is not a sudden development, nor is it driven by a single initiative. It is the result of a gradual alignment between capital, policy and strategic intent.

DATA LAYER — Capital and Institutional Build-Out

Recent data points reinforce this structural shift:

Institutional data points provide a clearer picture of this alignment. Mubadala has expanded its assets under management to approximately $385 billion, with an increasingly explicit focus on future-oriented sectors such as AI and robotics. Abu Dhabi Global Market (ADGM) continues to scale its financial ecosystem, now hosting thousands of active licenses and a growing concentration of asset managers. Meanwhile, platforms such as MGX, alongside partnerships involving global actors like BlackRock, indicate a deliberate move toward large-scale AI infrastructure investment.

- Mubadala AUM: ~$385B

- Abu Dhabi Global Market (ADGM): 12,000+ active licenses, expanding fund ecosystem

- MGX: dedicated AI infrastructure investment platform

- BlackRock partnerships targeting large-scale AI infrastructure deployment

Taken individually, these developments are noteworthy. Taken together, they suggest something more structural. The UAE is no longer functioning solely as a node for capital accumulation or redistribution. It is evolving into an environment where capital is translated into infrastructure.

Individually, these are notable. Collectively, they describe a system: capital is not only accumulating — it is being directed toward infrastructure.

From Financial Hub to Execution Layer

Historically, the UAE functioned as a capital hub. A place where money moved, settled and was redistributed. That function is evolving. This distinction matters. Financial hubs facilitate flows. Infrastructure hubs anchor them. The difference between the two is not semantic but functional. In one, capital passes through. In the other, it is deployed, fixed and operationalized.

The connection between the semiconductor rally and this regional positioning is not immediately visible, but it is nonetheless real. Semiconductor demand increases as compute requirements expand. As compute requirements expand, infrastructure must be built. As infrastructure expands, capital seeks jurisdictions capable of supporting large-scale, long-duration projects with minimal systemic risk. Over time, specific locations begin to absorb disproportionate importance within this chain.

The current trajectory suggests a transition toward: execution infrastructure

This includes:

- data center development

- AI compute hosting

- cross-border capital structuring

- regulatory environments optimized for scale

In this configuration, the UAE is not upstream (innovation) nor downstream (consumption). It is midstream infrastructure.

The Structural Connection: SOX and the Gulf

The relationship between the semiconductor rally and Gulf positioning is not direct. But it is causal. The chain is as follows:

- semiconductor demand rises

- compute infrastructure expands

- physical deployment requirements increase

- capital seeks stable jurisdictions

- infrastructure nodes emerge

This is not a coincidence. It is a sequence. And the SOX rally is the earliest visible layer of that sequence.

The System Is Repricing Infrastructure, Not Technology

What appears as a tech rally is, in fact, something broader:

- trade routes are being reassessed

- energy demand is being restructured

- capital allocation is shifting toward physical systems

- AI is acting as a catalyst across all layers

This is not cyclical behavior. It is structural repricing.

The New Configuration

A simplified model of the emerging system:

Layer 1 — Innovation (US / East Asia)

Semiconductor design and manufacturing

Layer 2 — Capital (Gulf / Sovereign Platforms)

Long-duration, large-scale funding capacity

Layer 3 — Infrastructure (Distributed Global Nodes)

Data centers, energy systems, connectivity networks

The Gulf is increasingly positioned at the intersection of Layer 2 and Layer 3.

Conclusion: Reading the Signal Correctly

An 18-day rally in semiconductor stocks is statistically rare. But its importance is not statistical. It is directional. It indicates where capital believes the next infrastructure layer will be built. And more importantly: it suggests that the build-out has already begun.

The market is not anticipating change. It is pricing early-stage implementation.

Final Frame

The question is no longer: “Will AI transform the global system?” The question is: Where will its infrastructure physically reside — and who will control its execution layer?

The answer is beginning to take shape. And the signal did not come from policy. It came from the market.