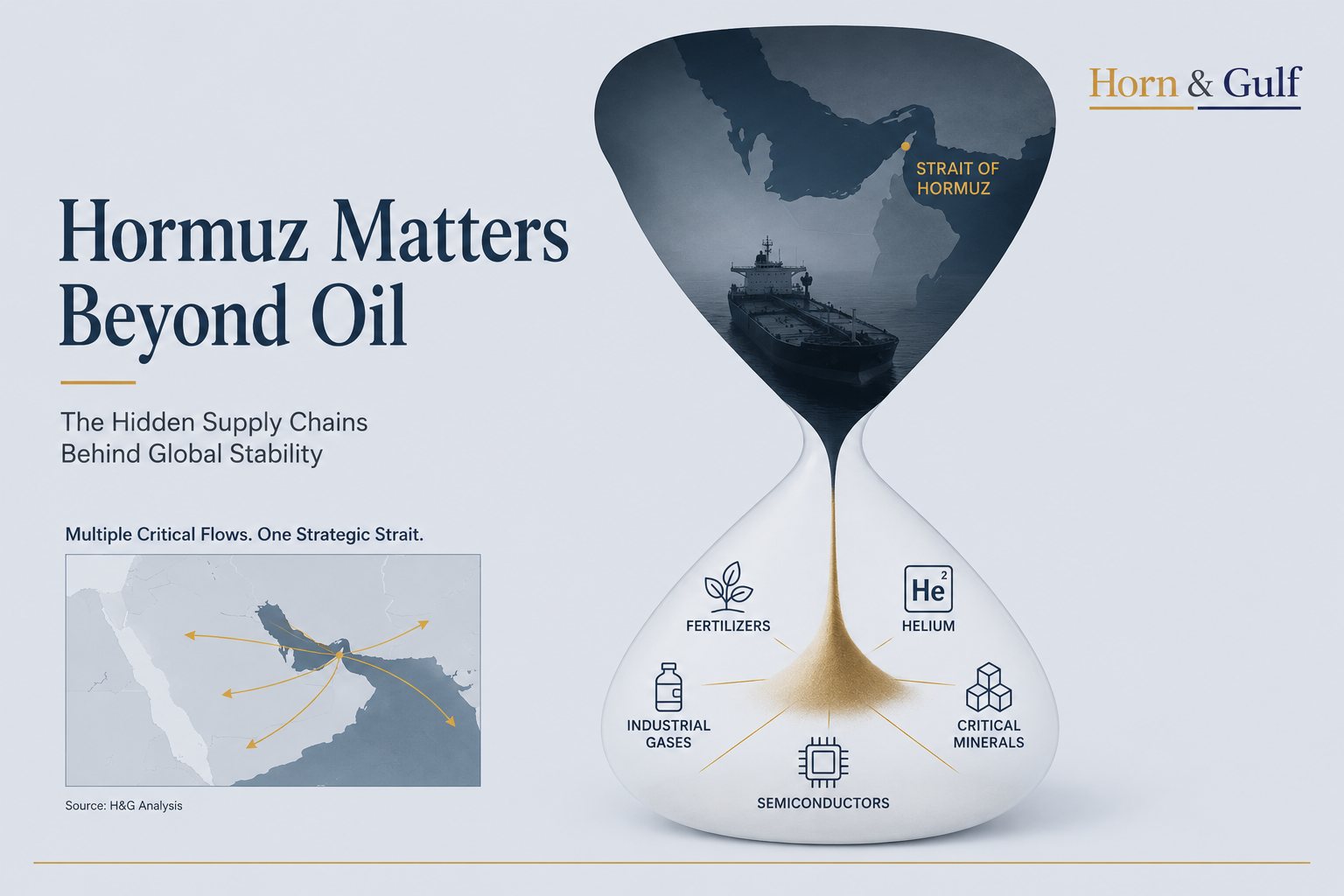

Hormuz supply chain risks are receiving renewed attention as tensions in the Gulf raise concerns beyond oil and LNG markets. While energy flows remain central, fertilizers, helium, sulfur products and industrial inputs also move through Gulf-linked supply chains, creating broader economic exposure during periods of maritime uncertainty.

For decades, analysts have viewed the Strait of Hormuz primarily through the lens of energy security. When tensions rise, attention usually turns to crude exports, LNG cargoes, tanker movements and the risk of military escalation.

That remains the right starting point. Yet it may no longer be the complete picture.

Recent analysis from different sources highlights a broader reality. The Gulf is not only an energy-exporting region. It also sits at the center of supply chains that support food production, semiconductor manufacturing, critical mineral processing and advanced industrial activity.

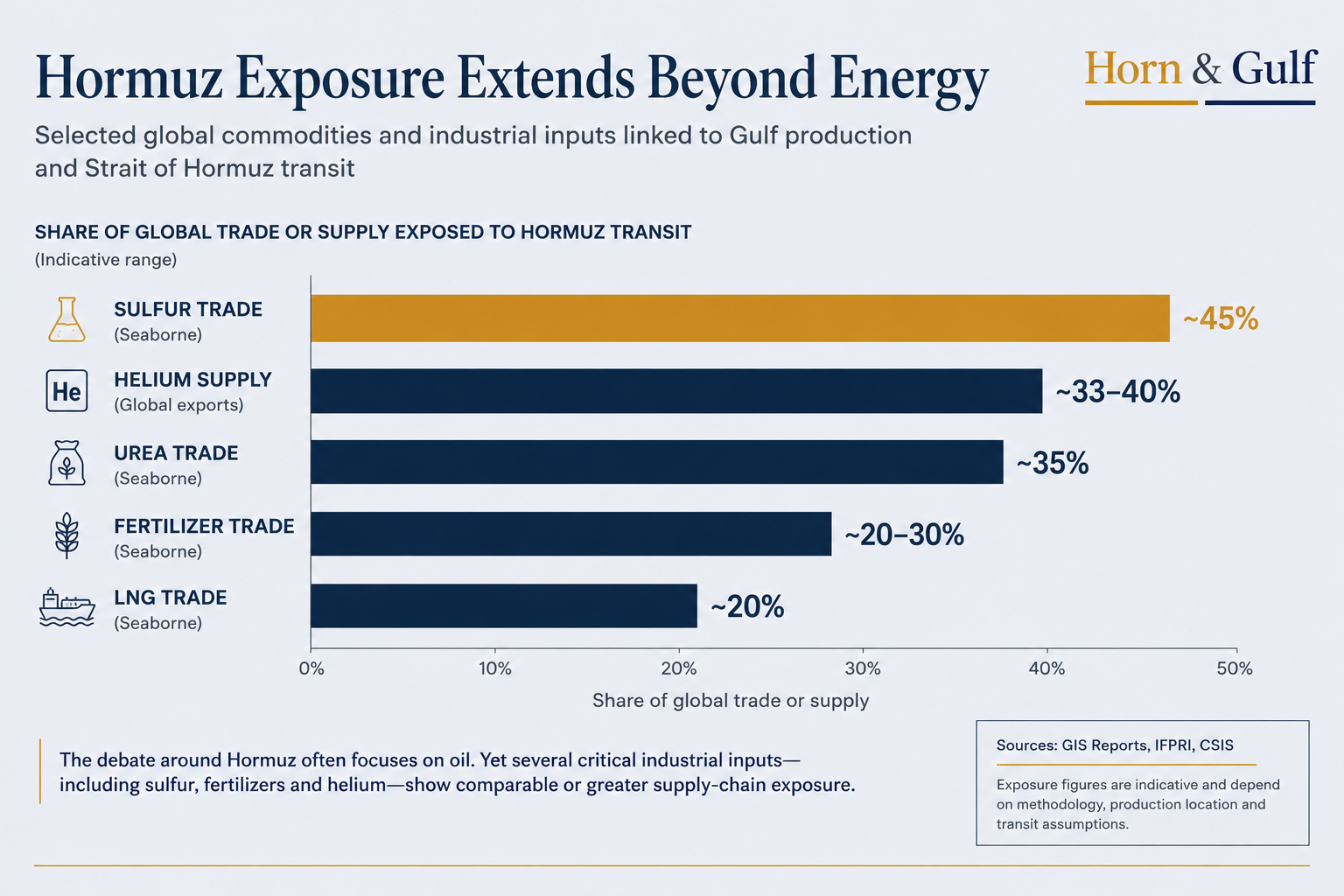

Fertilizer inputs, sulfur products and helium rarely receive the same attention as oil. During periods of maritime disruption, however, these industries can become strategically important.

Beyond the Traditional Energy Lens

The Gulf’s importance extends far beyond crude exports.

Qatar ranks among the world’s leading helium exporters. Gulf producers also play major roles in ammonia, urea and sulfur-related markets. These materials feed into agriculture, electronics manufacturing, mining, medical technology and high-end industrial production.

As a result, disruptions around Hormuz can affect more than energy markets. They can ripple across multiple sectors before policymakers or consumers fully notice the consequences.

This does not mean the global economy faces immediate disruption. It does suggest that the region’s strategic relevance reaches further than traditional oil-market analysis often assumes.

Not All Supply Chains Face the Same Risk

Different commodities respond differently to disruption.

Oil markets benefit from deep liquidity, strategic reserves and established adjustment mechanisms. Helium faces different constraints because storage and transportation options are more limited.

Fertilizer markets operate on seasonal agricultural cycles. Sulfur and sulfuric acid support industrial processes tied to metals, batteries and mineral refining.

These differences matter because exposure does not automatically translate into systemic vulnerability.

Many firms can adapt. They can draw down inventories, renegotiate contracts, reroute shipments or seek alternative suppliers. Markets rarely prove as fragile as the most dramatic crisis narratives predict.

The Cost of Uncertainty

Adaptation is rarely free.

For manufacturers, insurers, shipping companies and governments, uncertainty creates costs even when goods continue moving.

A cargo may still reach its destination, but higher insurance premiums, longer transit times and operational delays can alter investment decisions and planning assumptions.

The question is not only whether supply becomes unavailable.

The question is whether reliability becomes harder to guarantee.

In many industries, predictability matters almost as much as volume.

A Concentration of Industrial Dependencies

The most important observation emerging from latest analysis is not scarcity itself.

Rather, it is the concentration of multiple industrial systems within the same geographic space.

Energy exports, fertilizer production, industrial gases, petrochemical derivatives, maritime routes and insurance exposure all intersect around the Gulf.

That concentration does not guarantee systemic disruption whenever tensions rise. It does, however, increase the number of sectors exposed to the same source of geopolitical risk.

For policymakers and corporate planners, that reality deserves attention.

A Case for Caution

It is equally important not to overstate the argument.

Current tensions do not prove that Hormuz has become the central industrial chokepoint of the global economy. Nor do they prove that global supply chains are entering a period of fundamental reorganization.

A skeptical observer could argue that markets and analysts naturally search for additional vulnerabilities during periods of crisis.

In that reading, increased attention to helium, sulfur and fertilizer markets may reflect heightened risk awareness rather than evidence of a deeper structural shift.

That remains a reasonable challenge.

The burden of proof for long-term transformation remains significantly higher than the burden of proof for short-term disruption.

What to Watch Next

In the near term, vessel movements, military activity, shipping advisories and insurance premiums remain the most important indicators.

If tensions fade quickly, many current concerns may prove temporary.

A more significant signal would emerge if manufacturers begin increasing inventories, insurers maintain elevated risk pricing, or governments expand strategic planning beyond oil and gas.

Such developments would indicate that businesses and states are adjusting to a different assessment of supply-chain risk.

Conclusion

The strongest takeaway is not that Hormuz has suddenly become the world’s most important industrial chokepoint.

Instead, the current debate highlights how many critical supply chains converge around the Gulf.

Energy remains central to the region’s strategic significance. Yet fertilizers, helium, sulfur and industrial feedstocks increasingly deserve a place in the same conversation.

For now, the evidence points to heightened awareness rather than confirmed transformation.

The more important question is not whether Hormuz closes. It is whether governments, industries and investors begin treating Gulf-linked industrial inputs as strategic dependencies that require greater resilience, redundancy and long-term planning.