Gulf energy security has traditionally been measured through production capacity, export volumes and spare capacity. Recent developments around Hormuz, the Red Sea and maritime insurance markets suggest that Gulf energy security may increasingly depend on something else as well: the ability to sustain reliable delivery during periods of disruption.

For decades, analysts measured Gulf energy security largely in barrels produced.

That measure still matters. Production capacity remains the foundation of the region’s strategic weight in global energy markets. Yet recent pressure around the Strait of Hormuz, the Red Sea and regional shipping insurance markets highlights another question that is becoming harder to ignore.

Can those barrels still reach global markets during periods of military pressure, maritime disruption and insurance stress?

This is not yet a fully formed doctrine. Gulf producers are not abandoning a production-led energy model. Nor should observers treat every period of regional escalation as evidence of a new strategic era. The Gulf has navigated war risk, tanker threats and infrastructure challenges before.

Even so, the latest cycle of tension raises a broader question. Should analysts evaluate energy security not only through extraction capacity, but also through the ability to sustain delivery under pressure?

From Production Security to Delivery Risk

Policymakers traditionally relied on a relatively straightforward energy-security equation: reserves, production capacity, spare capacity and export volume.

Today, additional variables influence the same calculation.

A producer may have the barrels. It may have the terminals. It may even have committed buyers. Yet commercial conditions change when shipping lanes become contested, insurance premiums rise, vessels reroute, ports face greater security exposure, or missile and drone threats increase around critical infrastructure.

This is where the Gulf’s energy-security calculation is becoming more complex.

The challenge no longer revolves solely around production. Regional planners must also consider whether energy can move reliably through an environment where maritime routes, infrastructure protection and insurance markets increasingly influence one another.

What Is Already Visible

Several developments support this discussion.

Missile and drone threats have elevated the importance of critical infrastructure protection. The Red Sea crisis demonstrated how maritime disruption can alter shipping routes, raise costs and reshape commercial planning. Insurance markets have also become more responsive to escalation around major chokepoints. Meanwhile, Gulf producers continue to invest in alternative routes, export terminals, pipelines and non-Hormuz options.

None of these trends is new on its own.

Saudi Arabia has long benefited from Red Sea export access. The UAE has developed Fujairah as an important outlet beyond the Strait of Hormuz. Across the region, governments have invested heavily in air and missile defence. Shipping insurers have also incorporated conflict-related risk into pricing models for decades.

What may be changing is the cumulative effect of these factors when they occur simultaneously.

A missile threat no longer affects only military planning. A shipping disruption no longer affects only logistics. Likewise, an insurance premium is no longer merely a financial detail. During periods of stress, all three can influence whether energy reaches buyers at an acceptable cost and within predictable timelines.

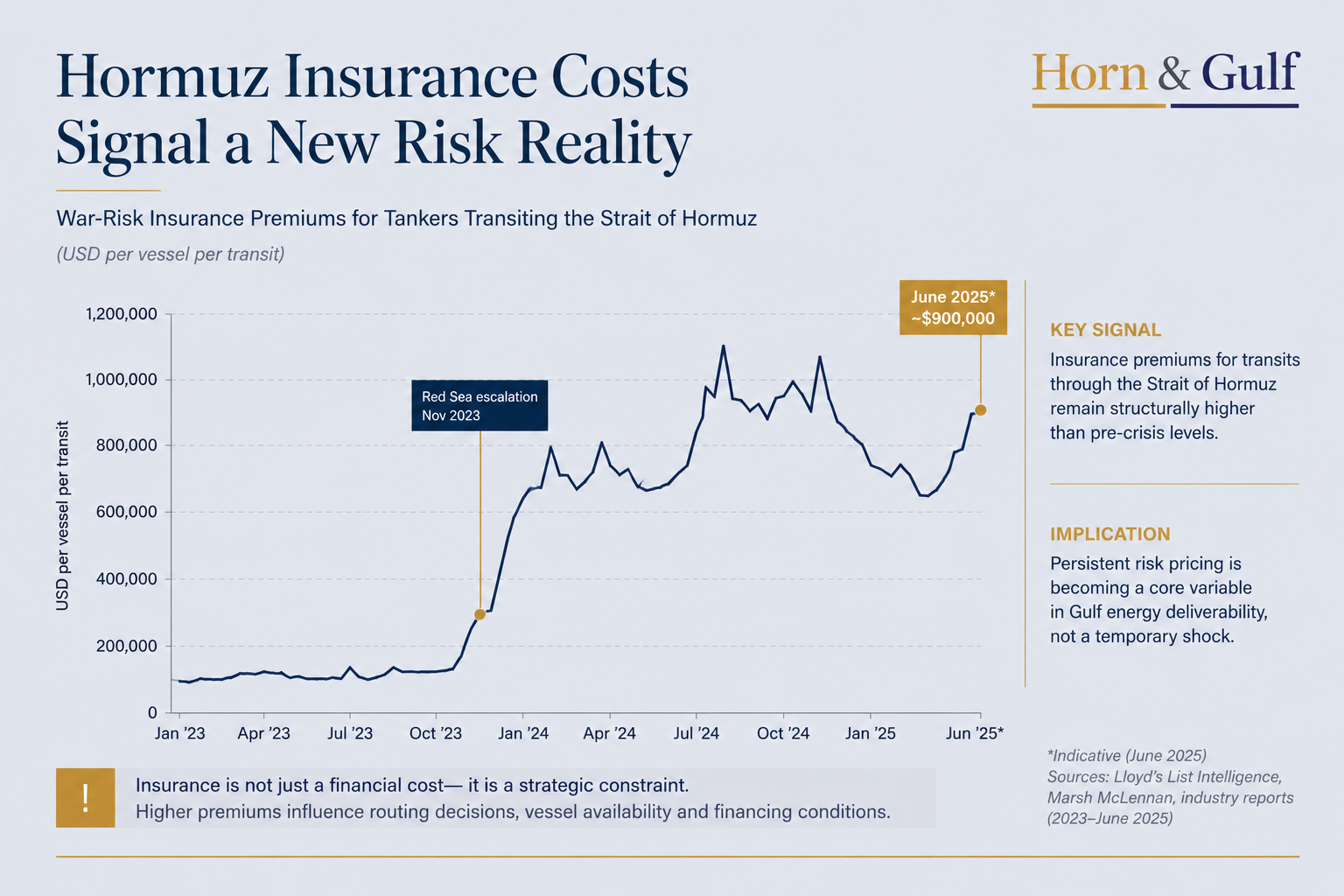

The Insurance Question

Insurance may represent the most underexamined part of this discussion.

Energy analysis often focuses on oil prices, tanker movements and military deployments. Those factors remain important. Modern energy markets, however, also depend on the ability to transfer and manage risk efficiently.

When premiums rise beyond commercially acceptable levels, insurers, financiers and shipowners become more cautious. Even if vessels can still use a route, higher war-risk premiums, reduced underwriting appetite, vessel shortages or financing hesitation can create a softer form of disruption.

Ships can still transit the corridor.

Yet commercial conditions change significantly.

That distinction matters because the Gulf’s role in global energy markets depends not only on production scale, but also on confidence in delivery. Buyers, refiners, traders, shipowners and insurers all contribute to that confidence. Once market participants adjust their behaviour, the effects of a crisis can spread without a formal blockade or direct military closure.

Hormuz and the Red Sea Are Not the Same Problem

It would be overly simplistic to merge every maritime disruption into a single strategic narrative.

Hormuz and Bab el-Mandeb are distinct chokepoints. Each involves different geographies, actors, security dynamics and commercial flows. A crisis in one does not automatically transform the other.

Nevertheless, analysts increasingly find it difficult to discuss the two in complete isolation.

If pressure increases around Hormuz, alternative routes through the Red Sea become more valuable. If instability grows in the Red Sea, those alternatives become more complicated to rely upon. This dynamic does not diminish Gulf export resilience. Instead, it highlights the importance of assessing resilience across multiple corridors.

Saudi Arabia’s Red Sea access remains a significant strategic asset. The UAE’s investment in Fujairah provides an important outlet beyond Hormuz. Kuwait and Bahrain operate within a different export geography and face different operating conditions. The regional picture is therefore not uniform.

Those differences matter when assessing resilience.

As a result, the next phase of Gulf energy security may depend not only on aggregate production capacity, but also on the geography of export options, infrastructure resilience and market access during periods of heightened pressure.

The Case for Caution

A strong counterargument deserves consideration.

The Gulf has experienced comparable periods of pressure before. The Tanker War of the 1980s, attacks on energy infrastructure, piracy concerns, Houthi campaigns and repeated maritime crises all generated predictions of systemic transformation.

Markets absorbed many of those shocks more effectively than expected.

Operators restored damaged infrastructure. Trade continued. Commercial systems adapted.

For that reason, a skeptical analyst could argue that the current environment represents another cycle of geopolitical turbulence rather than a new energy-security paradigm.

That perspective remains valid.

Energy markets have repeatedly demonstrated resilience. Gulf states possess extensive experience managing risk. Maritime systems often adapt faster than commentary assumes. Insurance costs can normalize when tensions ease. Shipping companies frequently return once immediate concerns recede.

Therefore, analysts should not treat deliverability security as an established doctrine. At present, it functions more effectively as an emerging lens through which regional energy resilience can be evaluated.

What Gulf States May Need to Measure Differently

If current trends persist, energy planning may gradually expand beyond output targets alone.

Production will remain central. Policymakers may also place greater emphasis on export flexibility, route redundancy, terminal protection, air and missile defence, port continuity, vessel availability, insurance capacity and the ability to sustain commercial flows during disruption.

This approach does not replace traditional energy security.

Rather, it expands it.

The Gulf’s strategic position has long rested on scale, reliability and market centrality. Looking ahead, policymakers may increasingly focus on how they preserve that reliability as surrounding routes face greater operational and security pressures.

Indicators to Watch

Several indicators may help determine whether current developments represent a temporary stress cycle or a more durable shift.

First, monitor war-risk insurance premiums around Hormuz, the Gulf of Oman and the Red Sea. A short spike would indicate market anxiety, while sustained elevation could point to a longer-term repricing of risk.

Second, track tanker-routing patterns. Repeated avoidance of specific waters or consistently higher compensation demands would reveal changes in commercial behaviour.

Third, watch utilization rates for alternative export infrastructure, including Red Sea-linked and non-Hormuz routes.

Fourth, assess Gulf investment in air defence, counter-drone systems and critical infrastructure protection.

Finally, review official GCC language surrounding energy security, maritime continuity and supply resilience. Policy language often reveals emerging priorities before formal doctrine appears.

A Measured Shift, Not a Turning Point

The Gulf is not entering a post-production era.

Production capacity remains central to the region’s role in global energy markets.

At the same time, policymakers increasingly evaluate resilience through a wider set of operational factors. Reliable transport corridors, insurable shipping activity and infrastructure continuity now form part of that assessment.

The stronger interpretation is not that a new era has fully arrived.

Instead, the traditional measure of energy security may be becoming incomplete.

One of the most important questions for the years ahead may not be how much energy the Gulf can produce under stable conditions. It may be how effectively producers can maintain transport, market access and commercial continuity when multiple sources of pressure emerge at the same time.