Ethiopia’s Gulf crisis budget signal offers a new way to understand the economic consequences of Gulf instability. While analysts often focus on tanker traffic, insurance premiums and oil prices, Ethiopia’s latest budget suggests that Gulf security disruptions are increasingly appearing inside Horn of Africa fiscal systems.

When analysts track the consequences of Gulf instability, they watch tanker traffic, insurance premiums and oil prices. Those are the right instruments for measuring what happens inside the strait. They are the wrong instruments for measuring what happens downstream.

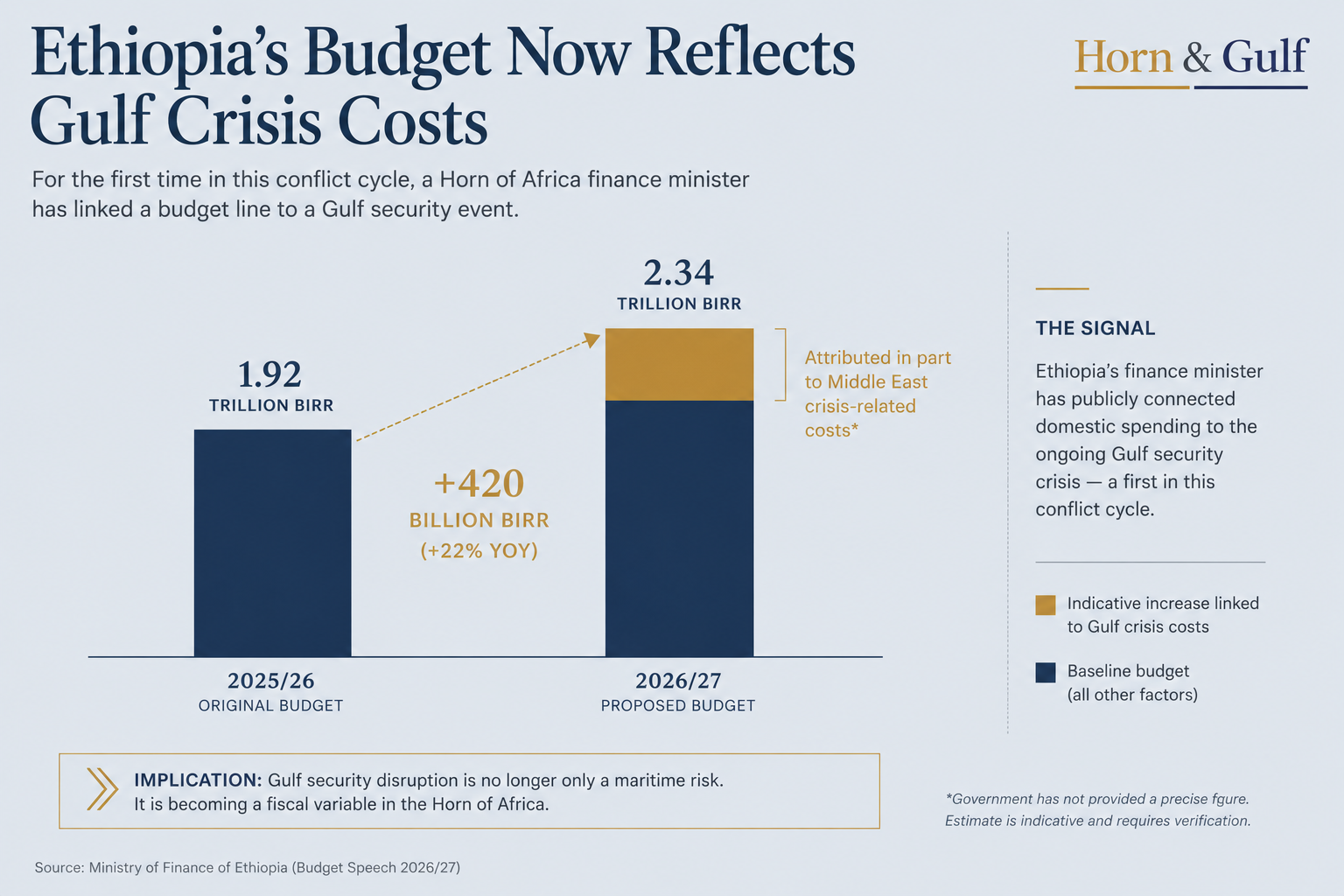

Ethiopia’s recently announced budget provides a different reading. Finance Minister Ahmed Shide presented the government’s plan to raise expenditure from 1.92 trillion birr to 2.34 trillion birr in the next fiscal year. He attributed part of that increase to costs arising from the ongoing Middle East crisis. The government had already expanded fuel subsidies since the conflict began. The 420 billion birr increase — roughly 22 percent year-on-year — is not entirely Gulf-driven. The government has not broken out a precise figure. But the minister’s framing is itself the signal. For the first time in this conflict cycle, a Horn of Africa finance minister stood in front of a legislature and connected a domestic budget line to a Gulf security event.

That connection deserves more analytical attention than it has received.

The Mechanism Is Not New — But It Is Now Visible

The basic mechanism linking Gulf energy disruptions to Horn economies is well understood in development economics. Energy-importing states face higher import costs when oil prices rise or when shipping and insurance costs increase. They absorb those costs in one of two ways. They pass them to consumers — generating inflation and political pressure. Or they expand subsidies, which transfers the cost to the fiscal account. Ethiopia has done the latter.

What makes this moment analytically significant is not the mechanism itself. It is the scale at which the mechanism now operates. It is the fiscal context in which it arrives. And it is the fact that it now appears in public budget documents rather than staying buried in trade statistics.

Three Pressure Points Operating Simultaneously

Ethiopia is managing one of Africa’s most complex sovereign debt restructuring processes under the G20 Common Framework. Its foreign exchange reserves have been under sustained pressure for several years. The IMF programme imposes fiscal targets calibrated against a specific set of external financing assumptions. None of those assumptions included a prolonged Gulf security crisis pushing energy import costs higher.

The result is a compounding problem. The subsidy expansion is not simply a budget line. It is a variable that now interacts with the debt restructuring timeline, the IMF programme conditionality, and the government’s foreign exchange management at the same time. Each of those interactions creates a different kind of fragility.

On debt restructuring: creditors evaluating Ethiopia’s debt sustainability path now work with fiscal projections that include an energy cost variable the original restructuring models did not contain. Even a modest sustained increase in subsidy expenditure tightens the fiscal space available for meeting restructuring terms. That does not make restructuring impossible. But it shrinks the margin for error and complicates creditor negotiations.

On the IMF programme: the programme set fiscal deficit targets before Gulf instability reached its current level. If subsidy costs push the deficit above agreed thresholds, the government faces a direct choice. It can let the programme slip — with consequences for disbursement and market confidence. Or it can cut spending elsewhere to compensate. Both options carry costs that the original programme design did not price.

On foreign exchange: fuel imports are priced in dollars. When import bills rise, reserves fall faster. Ethiopia’s reserve position was already thin before this conflict cycle began. Sustained higher energy costs accelerate the depletion of a buffer that was already below IMF adequacy standards.

These three interactions are not the same risk. They operate on different timelines and require different management responses. But a single external shock — transmitted through energy prices — is now producing simultaneous pressure on all three pillars of Ethiopia’s external financial stability. None of those pillars had significant spare capacity to begin with.

Ethiopia Is the Visible Case. It Is Not the Only Case.

Most Gulf-Horn analysis treats the two regions as economically distinct. Gulf security disruptions are a Gulf problem. Horn economic fragility is a Horn problem. The two occasionally intersect at Bab al-Mandab but largely remain in separate analytical compartments.

Ethiopia’s budget shows that this compartmentalization is becoming less accurate.

How the Mechanism Runs Across the Region

The same transmission mechanism operates across the Horn’s energy-importing economies, at varying intensity.

Djibouti serves as the primary logistics hub for Ethiopian trade and hosts a concentration of external military presences. It imports virtually all of its energy. Its public finances depend heavily on trade volume and port revenue — both of which regional shipping disruption affects directly. A sustained decline in Bab al-Mandab transit traffic reduces port fee income at precisely the moment when import costs are rising.

Somalia’s federal government already operates with extremely limited fiscal capacity. It faces the same energy cost pressure as Ethiopia, but without the subsidy infrastructure or IMF programme access that gives Ethiopia tools to manage it. The transmission mechanism arrives. There is almost nothing to absorb it.

Eritrea is less integrated into global financial systems and therefore less visible in international data. But it is an energy importer with limited reserves and significant fuel subsidy obligations. Its exposure to the transmission mechanism is real even when it is harder to track.

The pattern holds across the region. The Horn economies most exposed to Gulf shock transmission share the same profile: thin fiscal buffers, limited reserve adequacy, active debt pressures, and subsidy obligations that make it politically difficult to pass energy cost increases on to consumers. That description fits most Horn economies simultaneously.

What Changes If Gulf Disruptions Become Recurring

The current period of elevated Gulf security pressure may prove temporary. A diplomatic resolution, a shift in Houthi operational capacity, or sustained de-escalation could reduce maritime risk premiums. In that scenario, the fiscal pressures documented above ease. Horn economies return to managing their structural challenges without the Gulf-origin variable.

But a second scenario deserves serious consideration. Gulf security disruptions may become a recurring feature of the regional environment rather than an exceptional event. Not necessarily at current intensity — but as a persistent background condition that Horn fiscal planners can no longer treat as a tail risk.

What Structural Embedding Would Require

If that scenario materialises, the consequence is not simply a higher baseline for fuel subsidy costs. It is a structural shift in how Horn governments design their fiscal frameworks.

Development finance institutions would need to build energy-volatility buffers into programme design for Horn borrowers. Programmes that do not price Gulf-origin energy risk are calibrated to a regional environment that may no longer exist.

Creditors evaluating Horn sovereign debt would need to add Gulf disruption sensitivity to their default models. A shock that was previously an outlier becomes a recurring variable.

Infrastructure investors planning logistics assets along the Addis Ababa–Djibouti corridor, the Berbera corridor, and Red Sea-adjacent trade routes would need to price in periodic Gulf-origin shipping disruption. Their current utilisation assumptions do not account for it.

These are not abstract adjustments. They change the economics of specific investment decisions, specific programme designs, and specific lending terms. The Horn of Africa’s development finance environment is already under stress — from post-pandemic debt accumulation, weak growth recoveries and climate vulnerability. A permanent additional variable would arrive in a framework not built to handle it.

What Decision-Makers Should Watch

The leading indicator for whether the temporary or structural scenario is materialising is not in the Gulf. It is in the budget documents of Horn governments.

If Ethiopia’s next budget cycle — and those of Djibouti, Somalia and other regional governments — continues to show energy-linked expenditure increases, the transmission mechanism is becoming embedded rather than temporary. Budget documents are slow, noisy signals. But they reveal when a government has stopped treating a cost as exceptional and started planning around it as permanent.

The second indicator sits in the debt restructuring process. If Ethiopia’s creditors begin incorporating Gulf energy cost sensitivity into their restructuring models — adjusting debt service paths to account for recurring subsidy pressure — that signals the professional risk community has concluded the mechanism is durable. Watch for any reference to energy cost volatility in IMF Article IV language or creditor committee communications on the Common Framework process.

The third indicator is the most geopolitically significant. Watch whether Gulf states begin treating Horn fiscal stability as part of their own strategic risk environment. The Gulf-Horn relationship has historically centred on Gulf investment in Horn infrastructure and Gulf interest in Red Sea security. That calculus is shifting. A world where Gulf security disruptions produce measurable fiscal stress in Horn governments gives Gulf states a direct reason to care about Horn fiscal resilience. An unstable Horn is a less useful strategic partner and a less functional logistics corridor. Whether Gulf sovereign wealth funds or bilateral development finance arms begin engaging with Horn fiscal vulnerability as a strategic question — rather than a purely humanitarian one — would confirm that the transmission dynamic has registered at the level of regional strategic planning.

Assessment

Ethiopia’s budget announcement is a data point, not a verdict. The precise scale of Gulf-linked fiscal pressure remains unclear. The government’s own projections suggest the expansion can be managed within its broader economic programme. Those projections may prove accurate.

What the announcement establishes — for the first time in this conflict cycle, in public official data — is that the economic boundary between Gulf security conditions and Horn fiscal conditions is more permeable than most regional analysis has assumed. The Horn is not simply adjacent to the Gulf security environment. Through energy pricing, import costs, subsidy obligations and the fiscal interactions that follow, it is increasingly a downstream recipient of Gulf-origin economic shocks.

The strategic implication is not that the Horn is in crisis because of the Gulf. It is that treating maritime risk and Horn economic fragility as parallel but separate problems is no longer analytically adequate. That habit of mind does not serve the investors, lenders or governments operating across this corridor.

Ethiopia put a number in a budget. That number is telling a regional story that deserves to be read at regional scale.

H&G covers strategic risk, capital flows and geopolitical architecture across the Gulf, Red Sea and Horn of Africa. Analysis reflects conditions as of June 2026.