DIFC insurance growth is no longer just a financial-sector story. It shows how Dubai is becoming a regional system for pricing, transferring and absorbing risk during periods of geopolitical pressure.

The latest insurance figures from the Dubai International Financial Centre do not read like a routine sector update. They sit in a very specific moment: a region marked by maritime disruption, rising geopolitical friction, and a steady repricing of risk across energy, logistics, and capital markets.

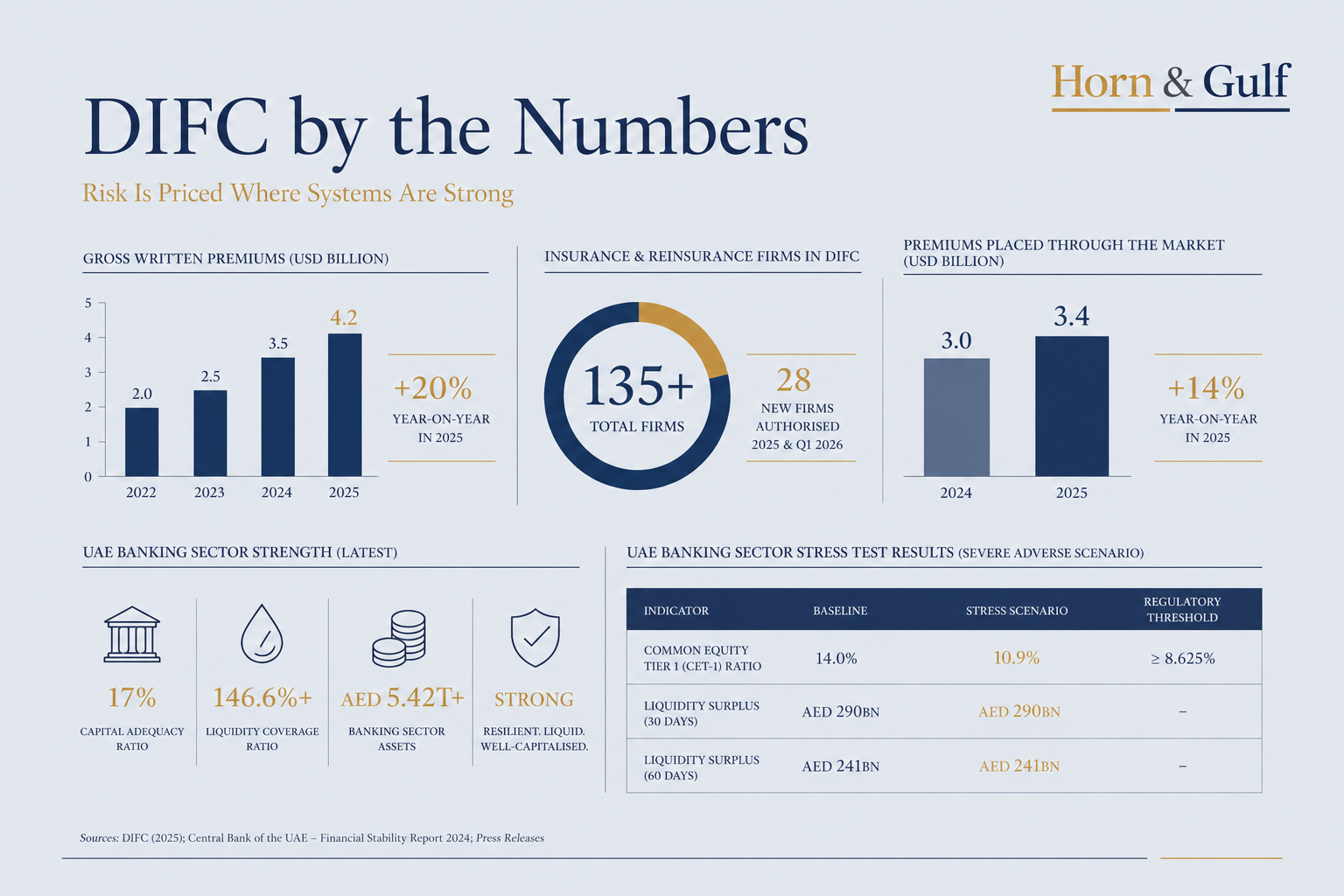

In 2025, gross written premiums reached USD 4.2 billion, marking a 20% year-on-year increase. Underwriting volumes have more than doubled since 2022. Premiums placed through the market exceeded USD 3.4 billion, up 14% compared to 2024. Over the course of 2025 and the first quarter of 2026, 28 new insurance-related firms were authorised, bringing the total number of insurance and reinsurance firms operating from DIFC to more than 135.

Taken in isolation, these are strong numbers. Read in context, they point to something more structural.

The Shift Is Not Growth — It Is Risk Migration

Insurance does not expand randomly. It expands where risk concentrates and where it can be priced with confidence.

The composition of DIFC’s insurance ecosystem is revealing. Growth is not limited to generic lines. It is concentrated in reinsurance, specialty underwriting, marine, aviation, property, and liability segments. These are the layers directly exposed to disruption — shipping routes, cargo flows, infrastructure assets, and cross-border trade.

At a time when the Red Sea has moved from a transit corridor to a contested space, when Hormuz intermittently signals fragility, and when piracy risks resurface along the Horn of Africa, insurance demand does not disappear. It relocates.

DIFC is increasingly where that relocation is being processed.

The System Behind the Market — Why Pricing Happens in Dubai

Insurance growth of this scale requires more than demand. It requires a system capable of absorbing volatility.

This is where the broader UAE framework becomes decisive. According to the Central Bank of the UAE, the country’s financial system entered this period of regional tension with capital adequacy at approximately 17%, a Liquidity Coverage Ratio above 146%, and total banking sector assets exceeding AED 5.4 trillion.

Stress testing provides the more relevant signal. In adverse scenarios combining geopolitical shocks, elevated interest rates, and economic slowdown, the system’s Common Equity Tier 1 ratio was projected to decline from 14.0% to 10.9% — a drop, but one that remains above regulatory thresholds. Liquidity buffers were estimated at roughly AED 290 billion over 30 days and AED 241 billion over 60 days.

These are not abstract indicators. They define whether insurance markets can function. Reinsurance capacity, claims settlement, counterparty risk, and cross-border placements all depend on the stability of the banking and regulatory backbone.

DIFC’s growth is therefore not independent of the UAE system. It is an extension of it.

From Financial Centre to Risk-Transfer Node

DIFC’s broader expansion reinforces this interpretation. The centre now hosts more than 8,800 active companies, over 1,050 regulated entities, more than 500 firms in wealth and asset management, and over 100 hedge funds.

Insurance is not growing in isolation. It is growing alongside capital.

This matters because insurance is not simply a financial service — it is the mechanism through which uncertainty is converted into tradable, quantifiable exposure. When capital moves into a region under stress, it does not ignore risk. It seeks locations where risk can be structured, priced, and transferred.

DIFC is increasingly fulfilling that role.

The Repricing Layer — Where Crisis Becomes Measurable

The common assumption in periods of instability is that capital exits. The evidence here suggests a different dynamic.

Risk is not being avoided. It is being repriced.

Shipping disruptions translate into higher marine premiums. Airspace uncertainty affects aviation risk models. Infrastructure exposure feeds into property and liability coverage. Trade volatility reshapes credit and political risk insurance.

These adjustments require a marketplace with legal clarity, regulatory predictability, and access to global reinsurers. Without that combination, pricing fragments. With it, pricing consolidates.

DIFC is becoming one of the points where that consolidation occurs.

Final Reading — Control Through Pricing, Not Stability

The significance of DIFC’s insurance growth is not that Dubai is insulated from regional instability. It is that Dubai is positioning itself within it.

The numbers — USD 4.2 billion in premiums, 20% annual growth, 135+ insurance firms, continuous inflow of new licences — are not just indicators of sectoral expansion. They are evidence of a deeper shift: risk is being routed through systems that can handle it.

In that sense, DIFC is no longer just a financial centre.

It is becoming part of the control layer through which uncertainty in the Gulf, the Red Sea, and beyond is priced, distributed, and ultimately absorbed.

Capital does not wait for stability. It moves toward the systems that can price instability.