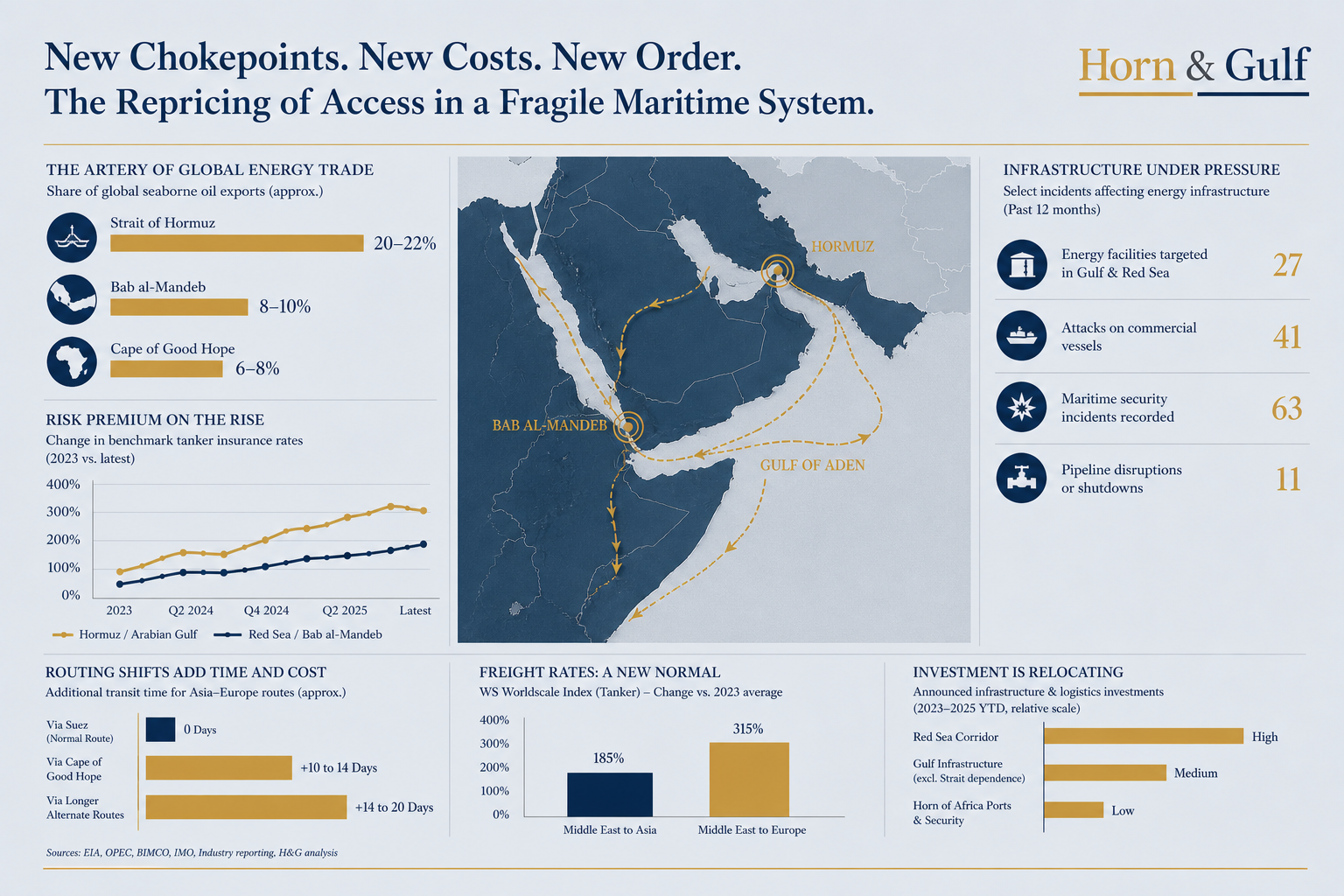

Hormuz Red Sea shipping risk is no longer a temporary disruption. It is reshaping global trade routes, energy flows and cost structures as maritime access shifts from open transit to controlled systems.

The last 24 hours did not produce a single defining headline. They rarely do. What they revealed instead was a pattern — a sequence of events that, when read together, points to a deeper structural shift.

This is not about escalation in isolation. It is about transformation. The Gulf is no longer pricing oil alone. It is pricing access.

US Escort Plan in the Strait of Hormuz Signals Market Fragility, Not Stability

The announcement of a potential US naval escort for commercial vessels in the Strait of Hormuz appears, at first glance, as reassurance. It is not.

A shipping corridor that requires military escort is no longer functioning as an open market route. It becomes a managed passage — one where movement depends on security guarantees rather than commercial logic.

In practical terms, this shifts pricing behavior. Insurance premiums, freight rates, and charter decisions begin to reflect controlled risk, not open flow. The signal is clear: Hormuz is moving from a transit route to a permission-based system.

Fujairah Oil Facility Attack Exposes Limits of UAE’s Hormuz Bypass Strategy

For years, the UAE invested heavily in bypass infrastructure — pipelines, storage, and export capacity designed to reduce reliance on Hormuz. Fujairah was central to that strategy. The recent strike on a key oil facility there reveals a critical vulnerability. Bypass does not eliminate risk; it redistributes it.

If infrastructure outside the Strait becomes targetable, then the concept of “bypassing Hormuz” loses its strategic certainty. The system adjusts accordingly: Risk is no longer tied to a single chokepoint. It expands across the entire export architecture.

UAE’s OPEC Exit Reflects a Shift from Energy Diplomacy to Strategic Autonomy

Abu Dhabi’s move away from OPEC coordination is often framed in terms of production freedom. That interpretation is incomplete.

What we are seeing is a shift from collective discipline toward unilateral flexibility — not just in output, but in investment, logistics, and pricing strategy. In a system where routes are uncertain and infrastructure is exposed, speed matters more than alignment.

The UAE is positioning itself to act independently in a fragmented energy landscape. This is not a policy adjustment.

It is a structural repositioning.

Saudi Arabia Rebalances Toward the Red Sea as a Strategic Energy Corridor

For Riyadh, the implications are more complex. Vision 2030 is not built solely on النفط revenues. It depends on logistics, tourism, industrial zones, and predictable access to global markets.

Hormuz instability exposes that dependency. The response is visible: increased strategic weight on the Red Sea corridor — ports, logistics hubs, and infrastructure tied to westbound flows.

The Red Sea is no longer a secondary route. It is becoming a parallel system — a hedge against Hormuz uncertainty.

Horn of Africa Security Risks Are Re-emerging as System Pressure Builds

As attention and resources concentrate in the Gulf, pressure shifts outward.

The Horn of Africa — particularly Somalia and the Gulf of Aden — is once again showing early signs of instability tied to maritime security. This is not coincidence.

When primary chokepoints become constrained, alternative routes absorb both traffic and risk. Weak governance environments then amplify that risk. The result is a widening security perimeter:

From Hormuz → to Bab al-Mandab → into the Horn. The system is stretching.

From Disconnected Events to a Single System Shift

Taken individually, these developments appear fragmented:

- A naval escort plan

- A facility strike

- A policy shift

- A strategic pivot

- A regional security flare-up

But they are not separate stories. They are stages of the same transition. A system built on open maritime flow is being replaced by one defined by control, access, and conditional movement.

The Core Shift: From Flow to Control

For decades, global energy trade operated on a simple assumption: routes remain open, and disruptions are temporary.

That assumption is eroding. What is emerging instead is a layered system:

- Hormuz becomes a controlled entry point

- Red Sea evolves into a strategic alternative corridor

- Horn of Africa re-emerges as a pressure zone

- Infrastructure beyond chokepoints becomes part of the risk map

- States adapt independently, not collectively

The market is adjusting accordingly. Not through panic — but through repricing.

What This Means for Capital and Strategy

Capital does not wait for clarity. It reacts to structure. And the structure is changing.

Shipping costs will not simply rise — they will differentiate. Insurance will not just increase — it will fragment. Energy flows will not stop — they will reroute under new conditions.

Most importantly: Access itself becomes a priced asset.

Conclusion

This is not a temporary disruption. It is a transition toward a new maritime order — one where chokepoints are no longer just geographic constraints, but strategic control layers.

The Gulf is not entering a crisis phase. It is entering a pricing phase. And in that system, the question is no longer:

Can ships pass?

But:

On what terms — and at what cost?