Hormuz governance negotiations—not the ceasefire itself—are becoming the central issue in the Doha talks. While diplomatic attention has focused on reducing military tensions, the more consequential question is who will administer the Strait of Hormuz once temporary commitments expire. That distinction has important implications for Gulf energy security, maritime insurance, and institutional risk assessment.

Coverage of the Doha contacts reads like a peace process: a US delegation on the ground, an Iranian delegation on the ground, Qatar mediating between them. That frame is not wrong, but it is incomplete. The parties are not negotiating the terms of ending a war — they are negotiating who operates the strait once the ceasefire holds. That distinction maps onto a different risk landscape for every institutional portfolio exposed to the Gulf.

The Format Pre-Defines the Scope

Iran is refusing to meet directly with the US delegation while keeping the Qatari channel open. That choice is not incidental — an indirect format lets both sides advance technical issues without conceding they are at the same table. This matters. An indirect format cannot carry a comprehensive peace agreement — it can only carry limited, reversible technical protocols. What emerges from Doha is therefore unlikely to be a signed peace text. It is more likely to be a provisional administrative formula linking frozen funds, sanctions relief, and a maritime transit regime.

That limitation does not mean the talks are failing — it means the format itself has already narrowed what negotiators can put on the table. And at the center of that narrowed space sits one question: who will operate Hormuz.

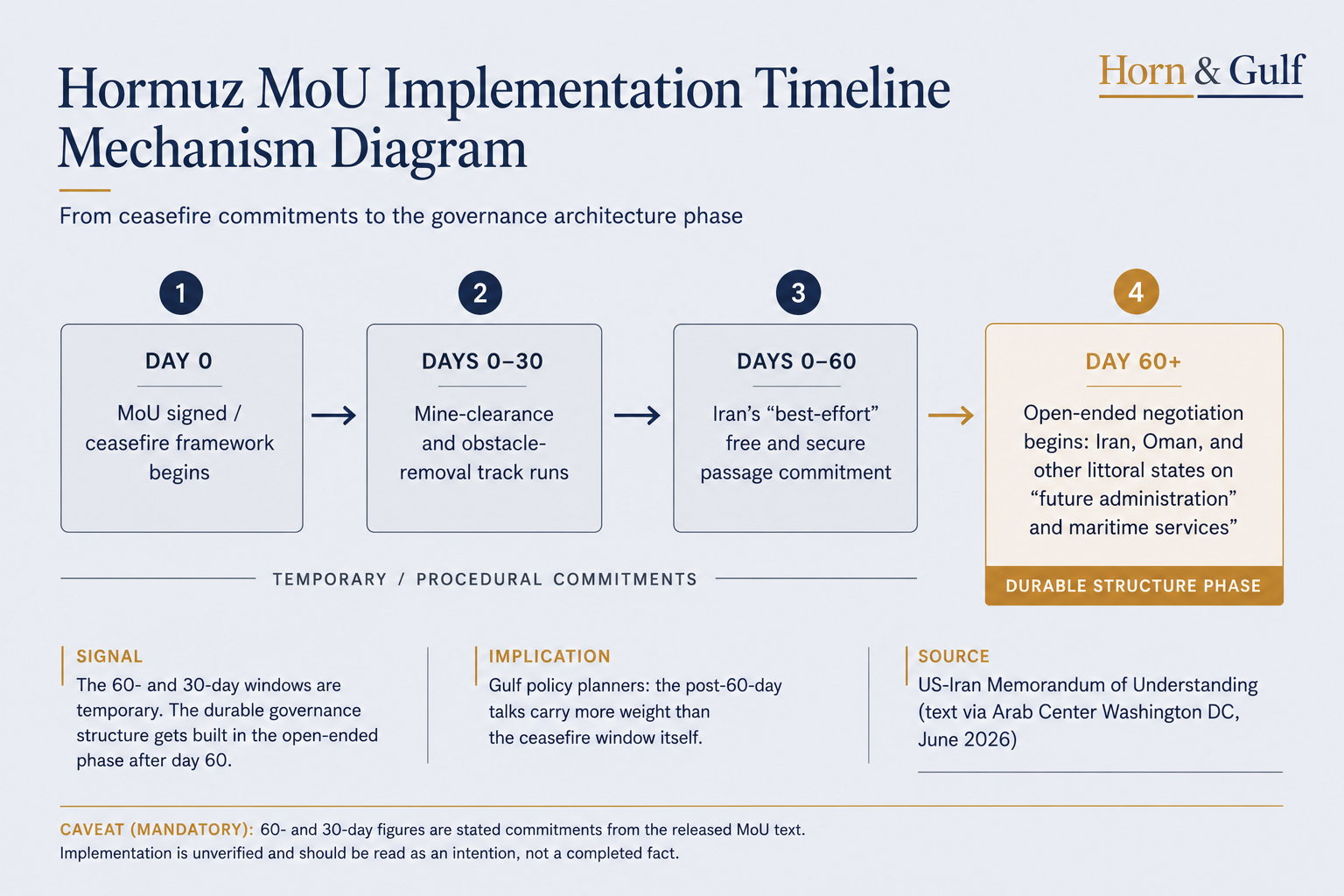

The Real Question: Not Whether the Strait Opens, but Who Runs It

The text of the US-Iran Memorandum of Understanding contains two concrete commitments. Iran will make its “best effort” to provide free and secure passage for 60 days. A 30-day mine-clearance and obstacle-removal track runs inside that window. Once that timeline expires, a separate negotiation begins among Iran, Oman, and other littoral states over “future administration and maritime services.”

That second phase matters more than the first. The 60- and 30-day commitments are temporary. The durable structure gets built in that second round of talks: who administers passage, under what legal authority, and at what cost. As Chatham House has noted, Iran may have lost part of its military deterrence. But Tehran is rebuilding that deterrence differently — not through the threat of direct confrontation, but through the administrative and operational costs it can impose on Gulf littoral states. This is a shift from hard power to bureaucratic-legal leverage.

The Market Is Pricing That Leverage in a Different Layer

A Reuters poll shows analysts cutting their 2026 oil price forecasts, on the logic that Hormuz’s reopening eases fears of a supply disruption. But that correction does not mean the risk has closed — it means the layer where the market prices that risk has shifted. Spot oil prices may be easing. But the uncertainty around Doha and Iran’s terms of passage hasn’t disappeared — it now shows up as a risk premium in a different layer of the market: insurance premiums, tanker charter durations, and LNG delivery schedules.

That distinction is decisive for institutional readers. An observer watching the price per barrel concludes the crisis has passed. An observer watching the insurance and freight market concludes the crisis has converted into an administrative regime. The second reading is the more accurate one — because the market is no longer pricing the probability of a physical supply cutoff. It is pricing legal uncertainty over who authorizes passage.

The Same Architecture Is Repeating at the Western Gate

This administrative-leverage logic is not confined to Hormuz. The International Crisis Group’s Red Sea assessment finds that regional competition has not cooled. The East African’s analysis goes further: it argues that Bab el-Mandab now demands a wider lens — one that tracks undersea cables, the digital economy, and financial infrastructure, not just shipping traffic. Hormuz carries energy. Bab el-Mandab links energy to trade and data infrastructure. For that reason, readers should not treat headlines out of Sudan, Eritrea, Ethiopia, and Somalia as separate national files. They are extensions of the same dual-chokepoint architecture at its western end.

What This Means, by Actor

For sovereign wealth funds, the implication is direct: risk models that measure Gulf exposure through a binary “strait open/closed” logic are no longer adequate. The relevant indicator is how predictable the transit regime’s licensing, oversight, and fee structure becomes. That shift requires reweighting portfolios — away from pure geographic risk, toward institutional-legal risk.

For logistics and freight investors, the data worth tracking isn’t the daily oil price. It’s how quickly tanker insurance premiums and charter durations react to news out of Doha. That reaction speed is the most direct measure of how seriously the market is taking the administrative uncertainty.

For Gulf policy planners, the message is that the second-phase talks with Oman and other littoral states carry more weight than the first phase. The administrative framework built in those talks will set the baseline for Hormuz risk pricing over the coming decade. Planners who arrive unprepared will carry direct exposure to future transit costs.

For creditors and development finance institutions, the Red Sea-Hormuz linkage carries a clear message: treat debt and infrastructure exposure in the Horn of Africa not as standalone local risk, but as a function of the same dual-chokepoint system.

Verdict

Doha’s real test is not peace — it is administration. Iran is converting technical control of Hormuz into a tool of sovereignty and leverage. That marks a shift — from a world where the strait is simply open or closed, to a regime where authorities license, insure, and monitor passage. That shift is already underway — the market’s reaction in the insurance and freight layer, rather than in the spot oil price, is the evidence. For institutional actors, the question is no longer whether the strait will open. It is who bears the cost of the new administrative regime.

Sources: Reuters, Financial Times, The Guardian, Chatham House, Arab Center Washington DC, International Crisis Group — reporting from June 30–July 1, 2026.

Note: The 60- and 30-day windows in the MoU are drawn from the publicly released text; their implementation remains an unverified commitment and should be read as such.