The Hormuz passage regime remains the central unresolved issue following the Islamabad MoU. While the agreement ended active hostilities, it did not determine who will administer navigation through the Strait of Hormuz, under what legal framework, or at what commercial cost. Those unanswered questions continue to shape insurance pricing, LNG deliverability and Gulf energy stability.

The Islamabad MoU ended the shooting war. It did not settle the question that determines whether Gulf energy markets normalise or fragment. Who administers Hormuz, under what legal basis, and at what cost to transit — all remain open. The 60-day window is not a peace timeline. Both parties entered it with incompatible starting positions. The MoU’s language bridged none of them.

I. What the MoU deliberately left open

Clause 5 of the Versailles memorandum commits Iran to toll-free passage for 60 days only. After that, “future administration and maritime services” will be defined through dialogue between Iran, Oman, and other Persian Gulf littoral states. The formulation is precise in its imprecision. It does not resolve the passage-regime question. It schedules it. Iran gains a negotiating forum it did not possess before the war. Tehran’s residual leverage at this moment consists almost entirely of its coastline.

The consequences moved faster than the diplomacy. Within 24 hours of the signing, Ghalibaf told reporters that Hormuz “will not return to pre-war conditions.” Iran, he said, will receive fees for services rendered to shipping. By June 23 — six days after the MoU — Iran and Oman had convened a joint working group in Muscat. Their joint statement mandated agreement on “the future administration of navigation in the Strait of Hormuz and the services that will be provided in this regard and the costs associated with them.” The pace of that convening is not a sign of progress toward resolution. It is a sign that Iran intends to use the 60-day window as a forum, not a countdown.

Why the pre-war baseline no longer applies

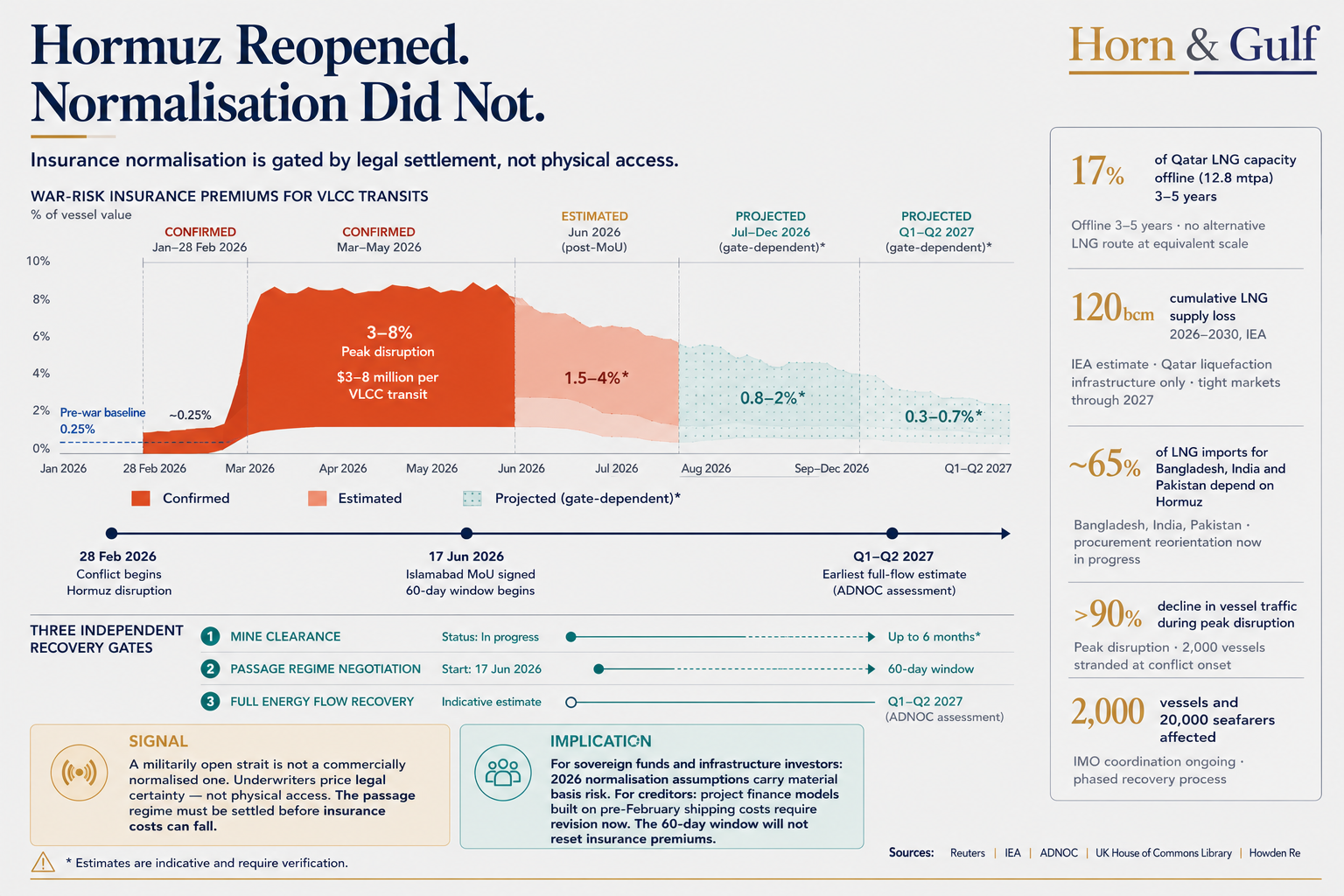

Before February 28, passage through Hormuz was governed by the 1968 Traffic Separation Scheme. Iran and Oman jointly administered it, the IMO endorsed it, and transit was free of charge. That baseline no longer exists as a given. It exists as a contested claim.

Iran’s Persian Gulf Strait Authority has already issued mandatory 48-hour pre-notification requirements for all vessels seeking transit. US defence estimates put mine clearance at up to six months. Cleared corridors will then require independent multilateral certification before insurers treat them as operationally reliable. The IMO’s coordination effort covers roughly 2,000 vessels and 20,000 mariners stranded during the conflict. It treats resumption as a phased process with independent technical, legal, and commercial gates — each of which must clear in sequence. The passage-regime question sits at the end of that sequence. The commercial architecture of the world’s most consequential maritime chokepoint will remain legally unsettled throughout the 60-day window. In all probability, it will remain so well beyond it.

II. The consequence chain

Before examining the mechanisms, the chain linking them to institutional outcomes deserves stating plainly. Each link is a distinct event with its own timeline and its own potential failure point.

Causal sequence

Passage regime unresolved→insurers price legal uncertainty→freight costs remain elevated→Gulf LNG and crude buyers extend alternative sourcing→Gulf deliverability premium erodes structurally→sovereign and infrastructure valuations require repricing

The chain does not require each link to fail catastrophically. It requires each link to persist long enough to alter commercial behaviour in the next. That is already under way. What follows maps the three mechanisms driving it.

III. Three mechanisms that make the window load-bearing

Insurance revalidation

Insurance revalidation is the first and most immediate mechanism. Before February, war-risk premiums for a single VLCC transit ran at approximately 0.25 percent of vessel value. At peak disruption they reached 3 to 8 percent — translating to $3 million to $8 million per transit for a vessel insured at $100 to $120 million. Marine insurers have been unambiguous: premiums will not normalise until mine clearance is independently verified and the passage regime’s legal status is settled. A commercially disputed strait carries elevated costs indefinitely. Underwriters price legal uncertainty alongside physical hazard — regardless of whether ships can physically pass. The passage-regime negotiation therefore directly gates insurance normalisation. These are not the same event, and the market has not yet priced the difference.

LNG deliverability

LNG deliverability is the second mechanism, and it operates on a longer lag with less reversibility. Qatar’s Ras Laffan terminals were struck in March. QatarEnergy declared force majeure on all LNG shipments. It has since confirmed that 17 percent of its export capacity — approximately 12.8 million tonnes per annum — will remain offline for three to five years. ADNOC CEO Sultan Al Jaber stated publicly in May that full Hormuz flows will not resume before the first or second quarter of 2027 regardless of diplomatic outcomes.

The scale of the LNG loss compounds that timeline. The IEA estimates a cumulative loss of approximately 120 billion cubic metres of LNG supply between 2026 and 2030. That figure covers damage to Qatar’s liquefaction infrastructure alone. Tight markets will persist through 2027. Bangladesh, India, and Pakistan imported nearly two-thirds of their LNG via Hormuz in 2025. They are now competing for constrained spot cargoes at materially higher prices. Procurement infrastructure for rerouted supply does not dissolve on a diplomatic headline. The contracts signed now will shape the Gulf’s LNG market position for years after the passage-regime question is settled.

Iran’s leverage architecture

Iran’s leverage architecture is the third mechanism, and the most analytically underweighted in current commentary. Tehran entered the MoU negotiations with significantly degraded military capacity. Trump claimed 158 Iranian naval vessels destroyed; CENTCOM’s own cumulative verified claims exceeded 100 ships across the campaign. Hormuz is now the primary residual leverage instrument Iran holds. Its proxy networks have been severely degraded. Its conventional naval capacity is a fraction of its pre-war level. Iran’s rational incentive is to keep the passage-regime question open — not resolve it. Doing so lets Tehran deploy Hormuz as concurrent pressure across the nuclear, sanctions, and Lebanon tracks that dominate the 60-day dossier. The Muscat working group’s convening six days after the MoU signing is consistent with that reading.

IV. What changes for each institutional category

Sovereign wealth funds and infrastructure investors

Gulf sovereign wealth funds and infrastructure investors are pricing a normalisation that the operational evidence does not yet support. ADNOC’s own 2027 estimate for full flow resumption sets a floor, not a ceiling, for the recovery timeline. The UAE’s Habshan-Fujairah bypass pipeline at 1.5 million barrels per day provided a genuine partial buffer. But it addresses crude only. It does nothing for LNG, containerised cargo, aluminium, fertilizer exports, or the roughly one-third of global helium production disrupted through Qatar’s LNG shutdown. Portfolio decisions premised on a 2026 normalisation timeline carry material exposure to the gap between diplomatic signal and operational reality.

Creditors and development finance institutions

For creditors and development finance institutions, the passage-regime outcome sets the floor for long-term shipping cost assumptions. Models with Gulf-linked project exposure need updating now. The pre-war cost structure — approximately $250,000 per VLCC transit — will not return in the near term under any scenario. Elevated freight costs will persist regardless of the Muscat fee outcome. Mine clearance uncertainty, convoy routing constraints, and insurer repricing on Gulf energy infrastructure each sustain them independently. Project finance models built on pre-February 2026 shipping cost assumptions require revision now. The 60-day window will not reset those costs.

Gulf policy planners

Gulf policy planners face the most structurally constrained position of any actor category. The GCC states have collectively opposed toll-like charges for Hormuz passage. Their position aligns with the US and with Oman’s preference to return to pre-war conditions under the 1968 Traffic Separation Scheme. They have the economic weight to make the Muscat working group difficult for Iran. They also have the most to lose from delay. Every month the passage-regime remains unsettled, Asian LNG buyers extend alternative arrangements. Insurance costs stay elevated. The deliverability premium Gulf exporters commanded before the war erodes further. The optimal outcome — a regime that satisfies Iran’s sovereignty claims in form while preserving toll-free access in substance — is achievable in principle. Whether Oman holds that line is the single most consequential procedural question of the next 60 days.

V. An alternative interpretation

Three scenarios that would falsify this analysis

The first and most plausible alternative: Iran may be seeking face-saving administrative language rather than sustained leverage. Its goal may be satisfying a domestic political narrative without materially changing transit conditions. A “service fee” labelled as Iranian sovereign administration — but functionally identical to Oman’s existing AMNAS Navdues system — could satisfy Tehran’s domestic requirements. In practice, toll-free transit would survive. Under this reading, the working group is a face-saving exercise. The 60-day window resolves faster and more completely than the main analysis implies. The falsification condition: a communiqué converging on a Navdues-style dues framework, with Hormuz shipping volumes recovering toward 50 percent of pre-conflict levels within 30 days.

The second alternative concerns insurance normalisation. If the IMO, in coordination with NATO mine-countermeasures assets, certifies cleared corridors within 30 to 45 days, war-risk underwriters may cut premiums sharply. Legal uncertainty would become economically secondary. Shipping economics, not passage-regime law, would then drive recovery. This scenario is operationally possible but contractually constrained. Hull war cover and war P&I extensions require formal JWLA listed area revision by Lloyd’s and the leading syndicates. That process follows sustained evidence of stability — not diplomatic announcements. The falsification condition is JWLA listed area status revision for the Persian Gulf within 45 days of the MoU signing.

The third alternative concerns the Asian buyer return. The analysis above treats buyer inertia as the default once alternative procurement is in place. Alternative LNG supply carries a real cost premium. IEA data shows global liquefaction plants outside the Gulf were already near nameplate capacity before the conflict. Replacement volumes come at spot prices materially above long-term Qatar contract rates. If that premium exceeds perceived Hormuz passage-regime risk, Asian buyers may return faster than contractual inertia suggests. This would accelerate the LNG deliverability recovery and shorten the window in which the consequence chain operates. The falsification condition: Japanese, South Korean, and Indian buyers cutting Q3 2026 spot LNG purchases from Atlantic and Pacific suppliers before the working group concludes.

VI. Three indicators to monitor

01

Lloyd’s JWLA listed area status

Watch whether leading war-risk syndicates revise Persian Gulf listed area status within 45 days of the MoU. Hull war cover returning below 1 percent of insured vessel value would confirm insurers have accepted the passage-regime trajectory. Continued elevation above 2 percent confirms legal uncertainty remains the dominant pricing input.

02

Asian LNG Q3 procurement decisions

Watch whether Japanese, South Korean, and Indian importers renew or extend Q3 2026 alternative supply contracts before the Muscat working group concludes. Early renewal signals buyers have already discounted Hormuz-dependent supply for 2026 — a commercial verdict more reliable than diplomatic language.

03

Muscat working group mandate scope

Watch whether the working group’s mandate expands beyond navigation dues to include vessel vetting, flag-state bilateral agreements, or IRGC oversight roles. Any such expansion indicates Iran is institutionalising the wartime vetting system — not negotiating its removal. That outcome has no precedent in the Traffic Separation Scheme era.

H&G assessment

The MoU did not restore Hormuz to its pre-war status. It created a 60-day negotiating forum. Iran holds residual leverage; the GCC states hold economic weight. Whichever pressure operates on the shorter timeline will determine the outcome. Iran’s leverage decays as mine clearance progresses and shipping volumes recover; the GCC’s economic weight is continuous. On that logic, a working-group outcome that preserves toll-free transit in practice remains the most probable scenario. The three alternative interpretations above are genuine, not constructed for balance, and any one of them could materialise.

What does not change under any of them is the consequence chain. A prolonged negotiation produces insurance cost persistence as its first-order effect. Asian LNG buyer reorientation away from Gulf-dependent contracts follows as the second. The strategic consequence is a permanent reduction in the deliverability premium Gulf exporters commanded before February 2026. Each of those consequences is already partially in motion. Institutional decision-makers who wait for the window to close will be adjusting to outcomes the market priced three to four weeks earlier. Passage resuming is not the same signal as the passage regime being settled. Those are different events. Only the second one closes the risk.

Sources: France24, Reuters (June 23, 2026) — Iran–Oman Muscat working group joint statement. ADNOC / Gulf News (May 21, 2026) — Sultan Al Jaber on 2027 flow resumption. Reuters (March 19, 2026) — QatarEnergy force majeure, 17% LNG capacity loss. IEA Gas Market Report Q2-2026 — 120 bcm cumulative LNG loss, 2026–2030. IEA Strait of Hormuz data — Bangladesh, India, Pakistan LNG dependency. Khaleej Times / Howden Re (May 2026) — VLCC war-risk premium ranges. UK House of Commons Library (June 2026) — mine clearance timeline. Stars and Stripes (March 16, 2026); Military Times (March 11, 2026) — CENTCOM naval vessel claims. Congressional Research Service — Qatar helium share (~30% of global production).