UAE crude export logistics are entering a new phase as rising Hormuz risk forces Gulf energy trade to adapt. Recent shipping patterns suggest the UAE is increasingly relying on alternative routing, storage integration and lower-visibility maritime operations to maintain export continuity under regional pressure.

The signal was not the oil — it was the method

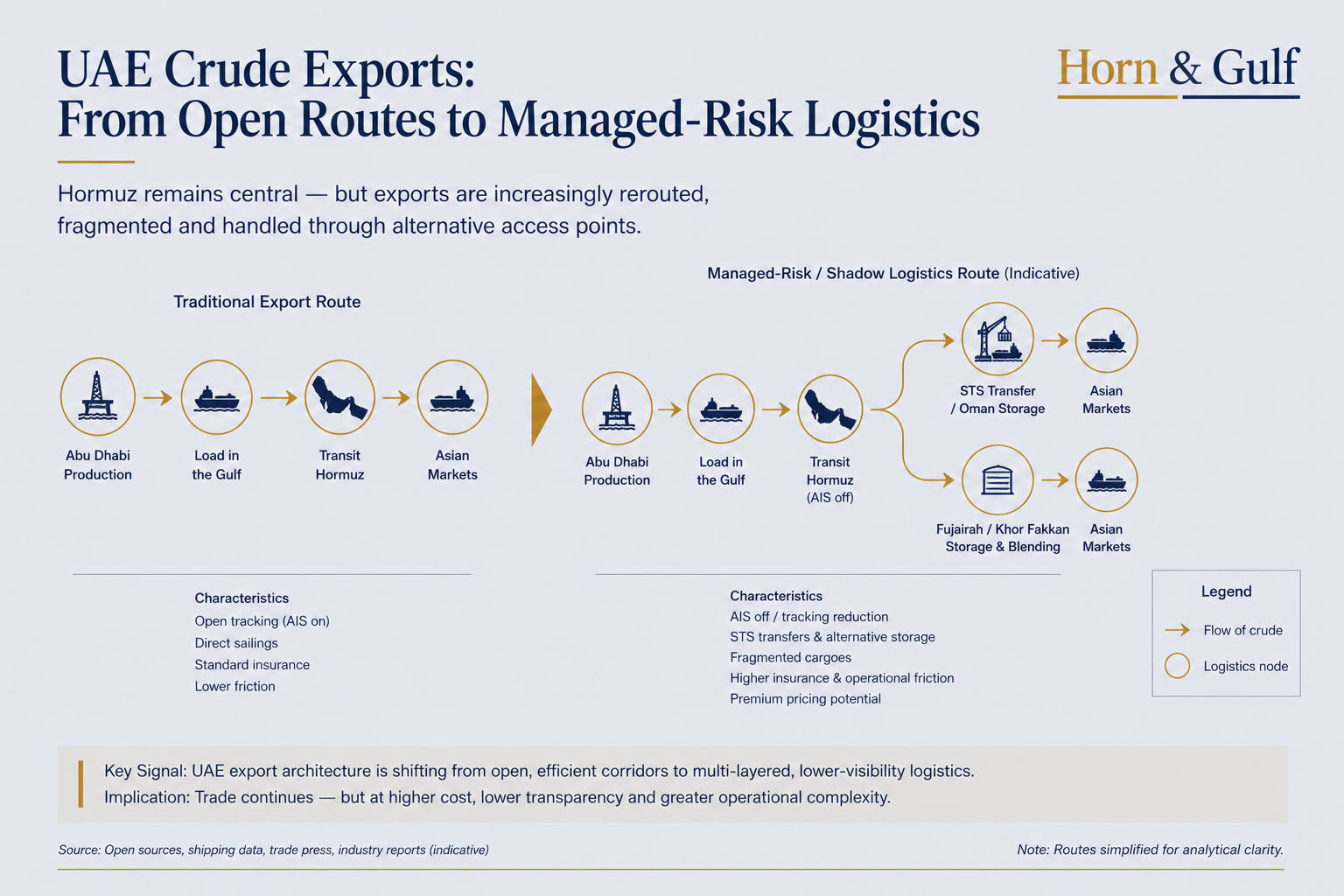

The most important part of the recent reporting surrounding ADNOC’s crude exports was not the volume itself. Gulf producers move millions of barrels every day. The real signal was the operational method behind the movement.

In April, at least six million barrels of Upper Zakum and Das crude were reportedly exported using tankers that switched off AIS tracking systems while transiting the Strait of Hormuz. Some cargoes were allegedly routed through ship-to-ship transfers, Oman-linked storage points and Fujairah-connected logistics channels before reaching Asian buyers.

Several details remain difficult to independently verify, and portions of the operational chain depend on shipping and trading sources familiar with the movements. But the broader pattern matters even with incomplete visibility.

The Gulf’s energy system is beginning to operate under conditions normally associated with sanctions evasion, wartime shipping or covert maritime trade.

That does not mean the UAE is collapsing into crisis. Quite the opposite. It means the region’s most operationally capable states are adapting to a new risk environment where continuity matters more than transparency.

Hormuz is shifting from a trade route into a permissions regime

Traditional maritime analysis treats Hormuz as a chokepoint: narrow geography, high throughput, military exposure. That framework is now insufficient.

Hormuz is increasingly functioning as a permissions regime. Cargoes may still move, but movement depends on layered tolerances: insurance acceptance, naval posture, tanker discretion, satellite visibility, political signaling and buyer willingness to absorb reputational or legal ambiguity.

This changes the economics of Gulf energy exports. Oil is no longer priced solely through supply and demand. It is increasingly priced through survivability of movement.

Reports from trading circles suggest that at least one fragmented Upper Zakum cargo traded at an unusually elevated premium during the recent period of maritime stress. Whether isolated or not, the pricing logic itself is revealing. Buyers were not merely purchasing crude quality. They were purchasing successful delivery through a stressed maritime environment.

That distinction matters. The premium is no longer attached only to the barrel. It is attached to the corridor.

The UAE’s advantage is flexibility — not immunity

Much of the international discussion around Gulf energy security still frames the UAE as comparatively insulated because of Fujairah and its eastern-coast infrastructure.

This is only partially true. The UAE does possess one of the region’s most sophisticated redundancy architectures. Fujairah, Khor Fakkan, pipeline infrastructure, storage integration and Oman-linked logistics provide operational depth that many regional producers lack.

But the recent shipping patterns simultaneously expose the limits of that flexibility.

A substantial share of Abu Dhabi’s crude system still originates inside the Gulf. Upper Zakum and Das production remain geographically tied to the very maritime system now under pressure. Even with eastern bypass infrastructure, portions of the export chain continue to depend on Hormuz-linked passage.

This is the paradox now emerging across the Gulf. State capacity and structural vulnerability are appearing simultaneously. The UAE is not trapped. But it is also not fully detached from Gulf exposure.

Fujairah is no longer just a port

The underpriced dimension in this story is infrastructural rather than military. Fujairah is gradually evolving from a commercial energy terminal into a strategic continuity platform for the wider Gulf system.

That distinction is important because strategic infrastructure behaves differently from ordinary logistics infrastructure.

Ports like Fujairah increasingly perform four functions at once:

- energy export continuity

- insurance stabilization

- cargo redistribution

- geopolitical redundancy

In practical terms, this means the Dubai–Abu Dhabi–Fujairah corridor is becoming more than an economic axis. It is becoming a resilience architecture.

Dubai contributes financial intermediation, maritime services and trade management. Abu Dhabi anchors production and sovereign capacity. Fujairah provides exposure to the Indian Ocean beyond the immediate Gulf bottleneck.

This integrated system may prove more important over the next decade than individual oil price fluctuations themselves.

The hidden shift is happening inside insurance and logistics markets

The deeper transformation is likely occurring away from headlines. Shipping companies, insurers, commodity traders and sovereign logistics planners are already recalculating exposure models for Gulf transit.

This is how geopolitical repricing usually begins. Not through dramatic closure events, but through gradual normalization of extraordinary operating behavior.

AIS-dark tanker movement, fragmented cargo routing, STS transfers and alternative discharge chains are signals that normal commercial assumptions are weakening.

Once these practices become routine, the regional maritime system quietly changes character. Trade continues. But it becomes slower, more expensive, more layered and increasingly dependent on state-backed coordination.

The Gulf’s strongest actors are no longer optimizing only for efficiency. They are optimizing for continuity under friction.

The long-term meaning extends beyond energy

Short term, the recent shipping activity shows the UAE can still maintain partial export continuity despite elevated maritime risk.

Medium term, it suggests the Gulf is transitioning from open commercial logistics into managed-risk logistics. Long term, it reveals something more structural: the future balance of power in the Gulf may depend less on raw production capacity and more on the ability to sustain movement during systemic stress.

That changes how ports, pipelines, corridors and maritime insurance should be understood. Infrastructure is no longer neutral. It is geopolitical leverage.

And Hormuz is no longer merely a strategic chokepoint on a map. It is becoming a control layer inside the global energy system — one where access, discretion and resilience increasingly matter as much as the oil itself.