Gulf economic predictability is facing renewed scrutiny as regional escalation increasingly affects aviation, logistics and investor confidence alongside energy markets. Initial reports linked to the latest Iran-related tensions in Kuwait and Bahrain suggest the pressure is extending beyond military signaling into the region’s commercial operating environment.

The broader concern is not only oil flows through Hormuz, but whether the Gulf can preserve the perception of operational continuity during geopolitical stress.

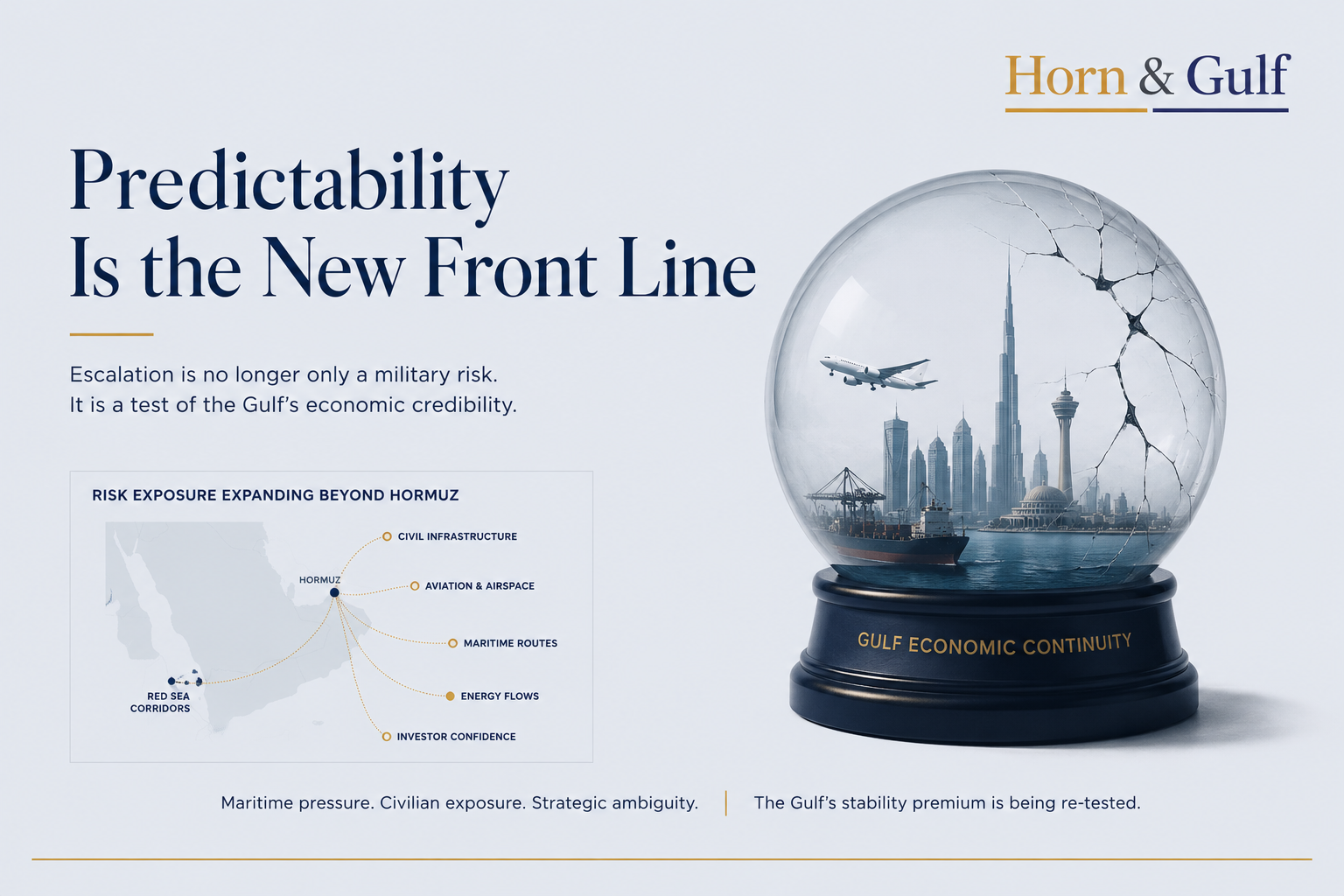

The latest escalation surrounding Iran is no longer viewed only through oil markets, military bases or naval activity near the Strait of Hormuz. Increasingly, attention is shifting toward a more sensitive question for Gulf economies: can the region preserve its reputation for commercial continuity during geopolitical stress?

Initial reports of escalation-linked incidents affecting Kuwait, alongside missile-related defensive activity in Bahrain, pushed regional attention closer to civilian-linked infrastructure, aviation systems and investor confidence. Some operational details remain disputed or incomplete. Several claims also still require independent verification.

Even so, the broader concern is already visible.

For Gulf economies, predictability is not simply a financial advantage. It is part of the operating environment on which logistics, aviation, trade and investment systems depend.

Ports, airports, energy infrastructure, financial districts and shipping corridors all rely on a shared assumption. Even during regional tension, the Gulf remains operational, insurable and commercially connected.

That assumption is facing renewed scrutiny.

Why the Current Escalation Feels Different

According to initial regional and international reporting, drone and missile activity linked to the wider Iran-related escalation affected areas connected to Kuwait International Airport operations. Reports also indicated injuries and infrastructure disruption.

Bahrain reportedly activated defensive systems after missile-related threats emerged in the context of rising Iran-US tensions and the presence of the US Fifth Fleet in the kingdom.

At the same time, international reporting suggested that Washington was evaluating or conducting retaliatory measures linked to maritime and regional escalation dynamics near Iran’s Qeshm Island.

Parts of the operational picture remain difficult to verify independently in real time. However, the broader strategic signal does not depend only on confirmed damage assessments.

Civilian-linked Gulf infrastructure is becoming increasingly exposed to the escalation environment. That shifts the crisis from a largely military confrontation into something more immediate for airlines, insurers, investors and regional governments.

The Risk Calculation Is Expanding

For decades, Gulf risk centered on the security of oil flows through Hormuz. During earlier crises, markets focused mainly on tanker traffic, crude exports and supply disruption.

The current environment appears broader.

Aviation routing, shipping insurance, supply-chain timing, port operations and investor perceptions are now entering the regional risk calculation alongside energy markets.

A disruption near an airport carries a different economic meaning from a maritime confrontation. It affects the Gulf’s identity as a region capable of sustaining commerce and connectivity even during geopolitical instability.

This does not mean Gulf commercial systems are breaking down. Energy exports continue. Major airports remain operational. Financial systems remain stable.

The region has also managed repeated geopolitical shocks over several decades.

Still, the risk environment is widening.

The question is no longer only whether oil can continue moving through Hormuz. Increasingly, the question is whether the Gulf can preserve the same perception of operational predictability while escalation thresholds become more fluid.

Hormuz Is Influencing More Than Energy Markets

Hormuz remains one of the world’s most important maritime corridors. Its importance to global energy markets has not changed.

At the same time, the latest escalation shows how the strait increasingly shapes broader commercial decisions.

Recent reporting suggests that some shipping and insurance actors are reassessing transit risk exposure around Hormuz-linked uncertainty. Governments and energy firms are also examining redundancy options, including bypass infrastructure, Red Sea-linked logistics and land-corridor alternatives.

These developments should not be overstated. Alternative routes remain expensive, capacity-limited and operationally uneven.

Red Sea and land-based alternatives cannot fully replace Hormuz. Nor can they eliminate the Gulf’s structural exposure to geography.

Yet repeated crises can gradually reshape what governments and companies consider commercially reasonable in terms of backup infrastructure and continuity planning.

Investments that once appeared excessive may increasingly look like strategic insurance.

US Strategic Ambiguity Adds Pressure

Recent comments by US President Donald Trump added another dimension to regional calculations.

Trump described shifting positions as part of his decision-making style. He also emphasized the value of keeping adversaries uncertain.

In military terms, unpredictability can complicate adversarial planning and preserve flexibility.

For Gulf states, however, the implications are more complicated.

The region’s security architecture remains deeply connected to the American security umbrella. At the same time, Gulf economic systems depend heavily on predictability, especially in logistics, aviation, investment and energy markets.

As a result, regional governments now appear to be managing two overlapping challenges at once:

- escalation risk linked to Iran;

- uncertainty surrounding how quickly US escalation thresholds may shift during crisis periods.

This does not signal a weakening of Gulf-US strategic relationships. Those ties remain central to regional security architecture.

Still, it helps explain why regional states continue investing in air-defense coordination, infrastructure resilience, diplomatic flexibility and continuity planning.

The objective is not only deterrence. It is also stability management under uncertain conditions.

The Red Sea and Horn of Africa Gain Relevance

The Red Sea and Horn of Africa are not replacing Hormuz as the primary center of regional tension. However, they are becoming more relevant to Gulf continuity planning.

Saudi Arabia, the UAE and other regional actors have spent years investing in logistics infrastructure, port access and strategic relationships across the Red Sea basin.

Djibouti, Somaliland, Eritrea, Sudan and Yemen all occupy increasingly important positions when maritime continuity and alternative routing become strategic concerns.

Caution remains necessary.

The current environment does not yet confirm the emergence of a completely new regional corridor order. Some rerouting activity may prove temporary if tensions ease. Many alternatives also remain commercially and operationally constrained.

Still, the logic of redundancy is becoming harder for governments and commercial actors to ignore.

Between Temporary Stress and Structural Adjustment

There are at least two plausible ways to interpret the current moment.

One interpretation is that the Gulf is entering a longer period of geopolitical adjustment. In this environment, insurance costs, aviation routing, infrastructure resilience and continuity planning become more central to economic strategy.

A more restrained interpretation also remains credible.

The Gulf has experienced repeated escalation cycles before. Markets often react sharply during uncertainty and later stabilize. Regional governments and commercial systems have historically demonstrated considerable institutional resilience.

Both interpretations remain plausible.

The region is not facing a collapse of commercial credibility. But this is also no longer routine geopolitical turbulence. Repeated pressure on civilian-linked systems can gradually shape how governments, insurers and markets assess long-term regional risk.

The strongest conclusion for now is not that a structural transformation has already occurred. Rather, the foundations for longer-term adjustment are becoming more visible.

Indicators to Watch

Several indicators will help determine whether the current environment remains temporary or develops into a more durable strategic adjustment:

- maritime insurance premiums linked to Hormuz transit;

- Gulf airspace advisories and commercial flight rerouting;

- vessel traffic patterns near Hormuz and Fujairah;

- GCC coordination on integrated air defense;

- Saudi and UAE investment in bypass infrastructure;

- Red Sea and land-corridor freight activity;

- oil and refined fuel price divergence;

- changes in US military posture across Bahrain, Qatar and Kuwait.

What Remains Unclear

Several important uncertainties remain unresolved.

The precise operational scale of the latest incidents remains partly unclear. The sustainability of further escalation is also difficult to assess. It remains uncertain whether current market reactions reflect temporary stress or the beginning of a longer-term shift in commercial risk calculations.

Gulf logistics and infrastructure systems may ultimately prove more resilient than current market anxiety suggests. Some strategic adjustments currently under discussion may also remain limited or temporary rather than transformational.

At this stage, the cumulative effect of repeated uncertainty may matter more than any single incident.

Conclusion

The latest Gulf escalation matters not only because of its effect on oil markets, but also because of its effect on confidence.

The Gulf’s modern economic model depends heavily on the perception that the region can remain commercially functional, operationally connected and strategically stable during periods of geopolitical tension.

That perception has not collapsed.

However, maritime uncertainty, civilian infrastructure exposure, evolving regional escalation dynamics and less predictable crisis signaling between major actors are testing it more directly.

For now, the Gulf remains operational.

The more important question is whether the long-term cost of maintaining that predictability is beginning to rise.