Hormuz bypass capacity has become a central strategic issue for Gulf energy and logistics planners. As regional tensions reshape maritime risk calculations, Gulf states are expanding pipelines, ports and inland trade corridors to reduce dependence on the Strait of Hormuz though available alternatives remain limited relative to the scale of existing flows.

The shift is not simply about rerouting oil exports. It reflects a broader regional effort to build continuity and operational resilience across interconnected maritime and logistics systems.

For decades, the Gulf’s strategic logic rested on a simple assumption: energy flows through the Strait of Hormuz because there is no meaningful alternative. That assumption is now being tested under a more complex regional security environment.

The visible signal is not merely rising maritime tension. It is the gradual emergence of a broader continuity architecture stretching from Fujairah to Yanbu, from Khor Fakkan to inland trucking corridors and future rail systems. What is unfolding across the Gulf is no longer simply a temporary shipping adjustment. It reflects a wider effort to reduce excessive dependence on a single maritime chokepoint.

The strategic concern around Hormuz has also evolved beyond the binary scenario of full closure. Regional policymakers, shipping operators and energy markets increasingly appear focused on a more prolonged environment of uncertainty, where shipping disruptions, insurance volatility and selective operational pressure may periodically affect maritime flows.

That distinction matters.

The Gulf Is Expanding Its Continuity Infrastructure

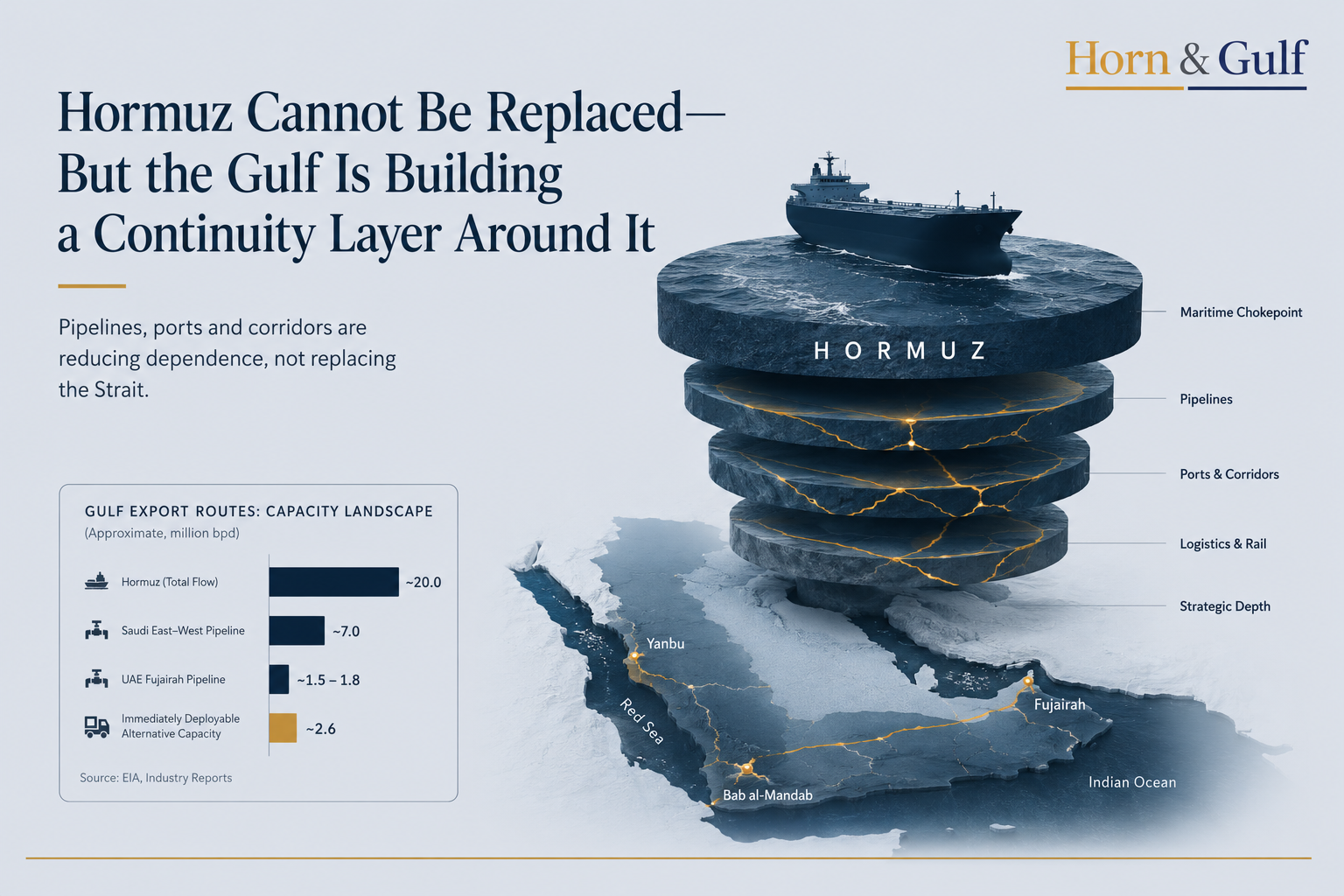

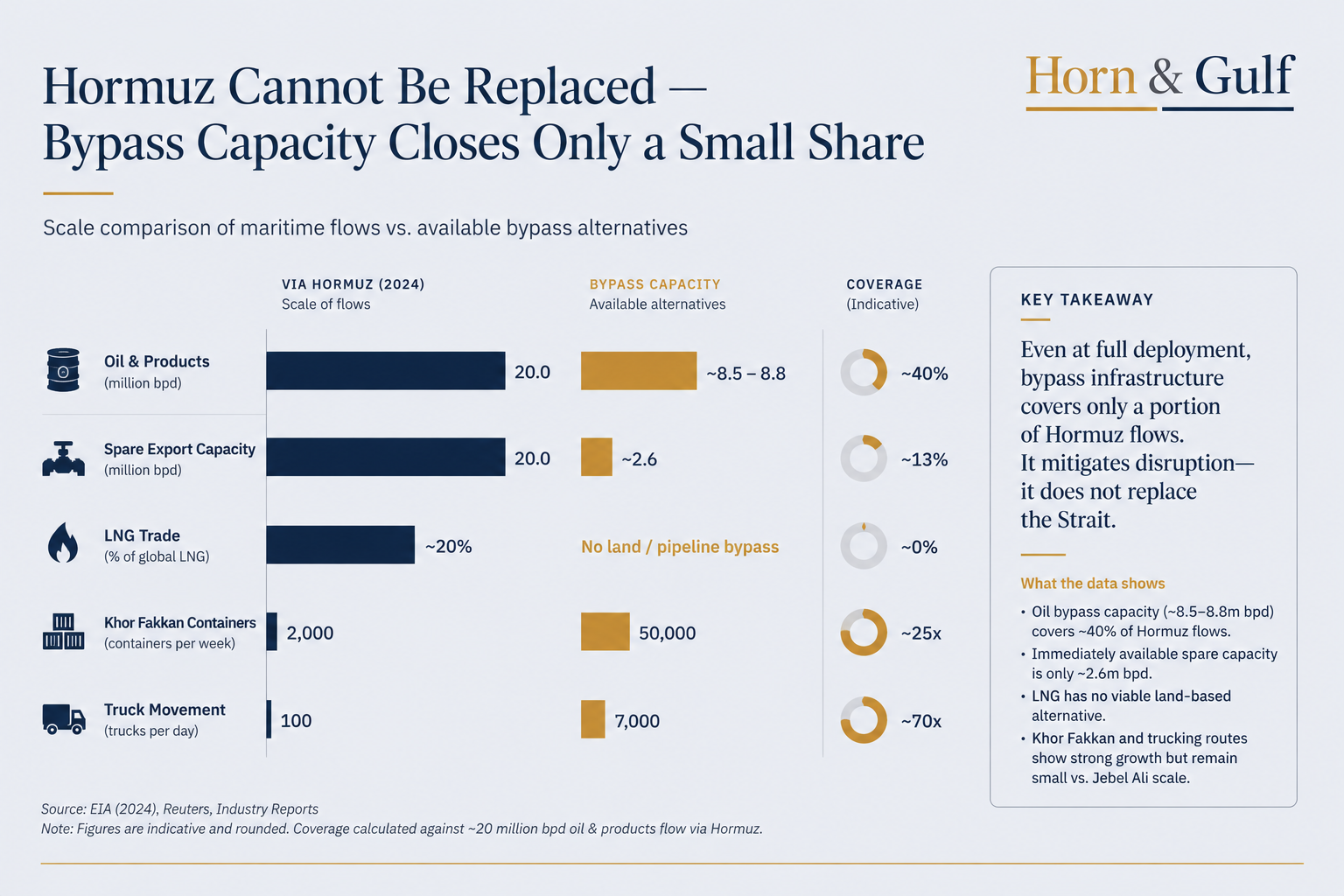

According to the U.S. Energy Information Administration (EIA), roughly 20 million barrels per day of crude oil and petroleum products transited through Hormuz in 2024 — close to one fifth of global petroleum liquids consumption. The Strait also carries a major share of global LNG trade, particularly from Qatar, making it one of the world’s most strategically important maritime corridors.

Yet the infrastructure available to partially bypass Hormuz remains limited relative to the scale of overall traffic.

Saudi Arabia’s East–West Pipeline, connecting the Eastern Province to Yanbu on the Red Sea coast, remains one of the region’s most important alternative export routes. Operational capacity is widely estimated at roughly 7 million barrels per day. In parallel, the UAE’s Abu Dhabi Crude Oil Pipeline to Fujairah is estimated to transport approximately 1.5–1.8 million barrels per day outside the Strait.

Together, these systems are strategically significant. However, immediately deployable spare capacity across regional bypass infrastructure appears considerably smaller than headline figures suggest.

EIA estimates indicate that available alternative export capacity under crisis conditions may amount to roughly 2.6 million barrels per day. While meaningful, that figure also illustrates the scale of Hormuz itself.

This remains one of the most important structural realities often overlooked in discussions about “bypassing” the Strait.

The Gulf cannot fully reroute its maritime economy onto land-based systems. What it can do is preserve partial continuity under periods of elevated stress.

From Maritime Route to Multi-Layered Logistics System

The most important shift may not be energy-related alone.

Recent logistics data from the UAE suggests accelerated movement toward eastern seaboard redistribution systems. Regional reporting indicates that Khor Fakkan has seen a significant rise in container throughput amid shipping adjustments, while trucking movements linked to rerouted cargo have also increased sharply. Exact figures vary across reports and should be treated cautiously, but the broader trend appears consistent: Gulf logistics systems are becoming more distributed.

Even at elevated throughput levels, Khor Fakkan remains significantly smaller than the broader Dubai logistics ecosystem. Jebel Ali continues to operate at a far larger scale and remains central to regional trade architecture.

But the strategic signal is not about replacing Jebel Ali. It is about building redundancy.

That redundancy increasingly includes:

- east coast ports outside Hormuz,

- dry ports,

- inland trucking corridors,

- future GCC rail integration,

- pipeline diversification,

- strategic warehousing,

- and insurance-linked routing flexibility.

In practical terms, the Gulf appears to be evolving from a highly centralized maritime export structure into a broader continuity-management system designed to operate more flexibly during periods of regional disruption.

The Chokepoint Has Not Disappeared It Has Expanded

A common analytical mistake is to frame bypass infrastructure as a complete solution to Hormuz-related risk. In reality, alternative systems often redistribute vulnerability rather than eliminate it entirely.

Saudi exports rerouted through Yanbu, for example, ultimately depend on Red Sea stability. That creates a second strategic layer through Bab al-Mandab, where recent years have demonstrated how drone threats, missile incidents and broader regional instability can affect shipping confidence and maritime insurance conditions.

This creates a wider strategic arc connecting:

- Hormuz,

- Fujairah,

- Bab al-Mandab,

- the Red Sea,

- the Horn of Africa,

- and Eastern Mediterranean shipping and insurance systems.

Under this structure, Gulf security is no longer solely about protecting tankers moving through a single waterway. It increasingly involves managing interconnected logistics and maritime systems across multiple operational theaters simultaneously.

The Gulf’s strategic geography is therefore expanding westward. And with it, so does the importance of Red Sea stability for long-term Gulf trade continuity.

Insurance, Capital and the Repricing of Continuity

The deeper economic story extends beyond the movement of ships themselves.

Insurance markets, sovereign investors, shipping firms and logistics operators are increasingly assessing not only physical disruption risk, but also continuity risk. The question is no longer simply whether cargo can move, but under which insurance, security and operational frameworks it can continue moving efficiently during periods of uncertainty.

This is where the Gulf’s infrastructure response becomes strategically significant.

The UAE’s continued investment in Fujairah, Saudi Arabia’s reinforcement of Red Sea export capacity and broader GCC discussions surrounding rail connectivity are not simply infrastructure projects. They also reflect efforts to strengthen strategic optionality across regional trade and export systems.

That optionality carries important economic implications:

- lower exposure to single-route disruption,

- greater operational flexibility,

- stronger continuity capacity,

- and more resilient positioning within global logistics networks.

This may also help explain why investment continues flowing into Gulf ports, logistics infrastructure, warehousing and trade-finance ecosystems despite recurring regional tensions.

Increasingly, markets appear to recognize that Gulf trade systems are being adapted not only for periods of stability, but also for periods of prolonged geopolitical uncertainty.

The Underestimated Constraint

There remains, however, an important limitation to the broader continuity architecture. Pipelines can partially reroute oil exports. Ports can redistribute some container flows. Truck corridors can absorb emergency pressure.

But LNG remains structurally more exposed.

Qatar’s LNG exports continue to depend heavily on Hormuz transit, and there is currently no comparable overland infrastructure capable of replacing that maritime dependence at scale. Any prolonged disruption affecting the Strait would therefore likely carry implications not only for oil markets, but also for Asian energy security, European LNG balancing and global shipping insurance pricing.

That means Hormuz retains significant systemic importance even within a more diversified Gulf logistics environment. The Strait may become less singular over time — but not less strategic.

The Gulf Is Preparing for a More Complex Operating Environment

The broader significance of these developments extends beyond the current cycle of regional tensions.

For decades, Gulf economic strategy emphasized efficiency: faster shipping, centralized export corridors and highly optimized maritime flows.

The emerging model appears different. It places greater emphasis on resilience. Redundancy. Continuity. And operational flexibility under uncertain regional conditions.

This reflects a wider geopolitical transition now visible across the Red Sea and Indian Ocean systems. Maritime chokepoints are increasingly viewed not simply as stable arteries of globalization, but as strategic control layers exposed to geopolitical pressure, non-state disruptions, sanctions-related risks and hybrid security challenges.

Under those conditions, infrastructure itself becomes part of strategic risk management. The Gulf’s response appears increasingly shaped by that reality.

Not by replacing Hormuz entirely. But by reducing excessive dependence on any single route within a more fragmented geopolitical environment.